Yahoo Finance

Yahoo Finance The 1 Reason to Avoid 3M Company's Stock

The 16% year-to-date dip in the stock price of 3M Company (NYSE: MMM) is naturally going to attract value investors toward the Dividend Aristocrat. After all, the company now sports a near 2.7% dividend yield, and more than 60 years of dividend increases attest to its history of delivering for investors. However, I think the stock is still worth avoiding. Incoming CEO Mike Roman's presentation at the recent Electrical Products Group (EPG) conference did little to dispel fears concerning the company's pricing power -- a key part of its business model. Let's take a look at why, as well as what was discussed at the event.

Image source: Getty Images.

3M's business model

3M has long prided itself on its ability to use research and development (R&D) in order to create differentiated products. In plain English, this means 3M's solutions aren't commodity-type offerings and therefore tend to have some pricing power. So, 3M should be able to grow revenue through increasing price without suffering significant drop-offs in volume while maintaining strong margin.

Outgoing CEO Inge Thulin was always keen to remind investors of 3M's business model, and Roman's EPG presentation followed a similar theme.

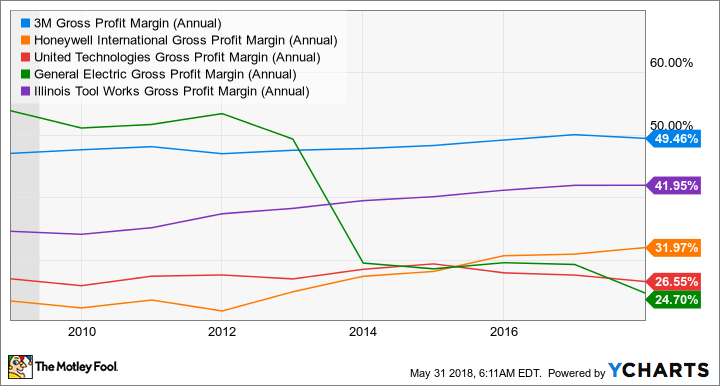

3M's margin performance

Indeed, 3M has demonstrated an ability to command margin, thanks to offering differentiated products. As you can see below, 3M's gross margin has been consistently superior to other leading industrial companies, including its best comparable multi-industrial peer, Illinois Tool Works.

MMM Gross Profit Margin (Annual) data by YCharts.

Signs of deterioration

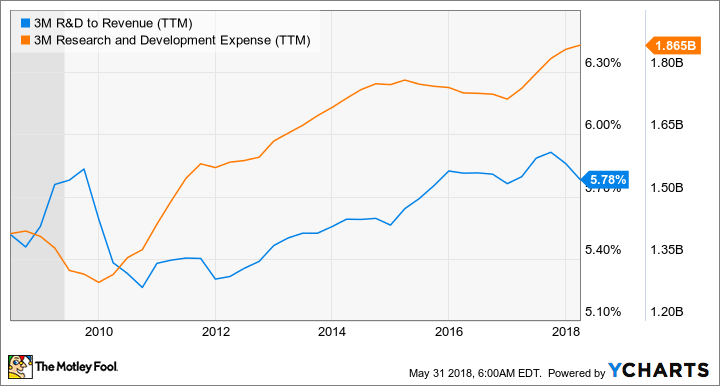

But here's the thing: There appear to be some cracks forming in 3M's business model. As you can see below, 3M has been increasing its R&D expenditures in the last decade on an absolute and relative basis.

MMM R&D; to Revenue (TTM) data by YCharts.

There's nothing wrong in this per se, but it needs to be backed up by demonstrable improvement in pricing power. Unfortunately, 3M appears to be losing ground on this issue.

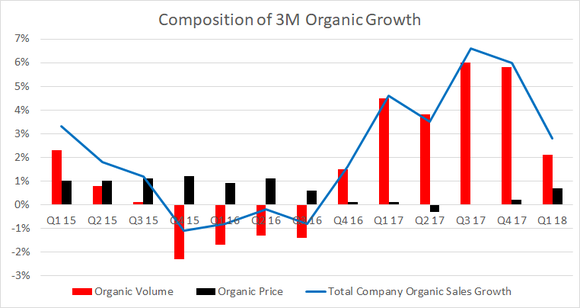

For example, the chart below shows two things that should concern investors. First, although total company sales growth was good in 2017, it was largely due to volume improvements -- 3M particularly benefited from a cyclical improvement in its electronics and energy segment in 2017, rather than any improvement in pricing.

Second, the chart seems to show an inverse relationship between pricing and volume. This is the sort of relationship you might expect from commodity-type products that don't possess much pricing power -- as prices rise, volume falls. In other words, this is precisely the kind of outcome that 3M is trying to avoid by investing in R&D.

Data source: 3M Company presentations. Chart by author.

Moreover, 3M's less cyclical segments (healthcare and consumer) are struggling to grow in line with management's mid-term guidance. The consumer segment has only grown in line with guidance in one of the last eight quarters, and the healthcare segment has only done this three times in the same period. The cracks are showing.

What management thinks about pricing

The issue of pricing came to the forefront at EPG, and Roman's response wasn't particularly convincing. In a nutshell, he said that in the first half of 2017, 3M was slow moving "into a higher growth marketplace," but in the second half, management adjusted and set the company up for stronger pricing. He cited the stronger pricing performance in the first quarter of 2018 as a sign of improvement.

Additionally, it's worth noting that on the first-quarter earnings call, CFO Nick Gangestad stated, "we expect price growth to remain strong, and that it will more than offset raw material inflation" for the remainder of the year.

Roman's argument and Gangestad's forecast are open to question for two main reasons. First, the first-quarter organic growth of 0.7% from pricing is not what you might expect from a company trying to take pricing in a growth environment. In fact, it's lower than any figure produced by 3M in 2015 -- recall that U.S. industrial production was in recession during 2015-2016.

Second, going back to 3M's second-quarter 2017 earnings call, Gangestad claimed 3M was making "selected price adjustments," but he expected "more normal price growth for 3M" in the second half of 2017. It didn't happen.

The reality is 3M didn't have anything like "normal" price growth in 2017. It could be argued that the strong volume growth in the second quarter was achieved because 3M didn't take aggressive enough action on pricing -- a sign that 3M doesn't have significant pricing power.

As you can see below, 3M stock has long commanded a premium compared to peers in its sector -- a large part of the reason why is its reputation for having products with pricing power.

MMM EV to EBITDA (Forward) data by YCharts.

Is 3M losing its touch?

Frankly, it's too early to tell just yet, but the warning signs are there. Management, for the second time in two years, is promising a better pricing environment in the second half of the year. However, I think cautious investors will want to hold off buying the stock in order to see if 3M will achieve this aim while also maintaining its --downwardly revised -- organic sales growth guidance of 3%-4% in 2018.

If 3M can't get back to demonstrating that it has pricing power -- a key part of its business model -- then investors have reason to question whether the stock continues to deserve its premium valuation rating compared to its sector.

More From The Motley Fool

Lee Samaha owns shares of Honeywell International. The Motley Fool recommends 3M. The Motley Fool has a disclosure policy.