Yahoo Finance

Yahoo Finance 2 Embarrassingly Low-Yield Dividend Stocks

Some of my best dividend stock ideas come from the Dividend Champions list, which is populated by companies like Franklin Electric Co. (NASDAQ: FELE) and Nordson Corp. (NASDAQ: NDSN) that have increased their dividends every year for 25 years or more. But being on this list isn't everything. Here's why I own Eaton Corp. (NYSE: ETN), but not either one of these two dividend stocks.

Great dividend records!

In many ways, Franklin Electric and Nordson are exactly the kind of companies I like to find. Franklin makes systems and components for moving liquids. Nordson makes adhesive dispensing equipment, fluid management products, and testing and inspection tools, among other things. They are perfectly fine, boring, industrial businesses of the type that I tend to favor. And they have great dividend payout records. Franklin has increased its payout each and every year for 26 consecutive years. Nordson's streak is even more incredible at 54 years. Clearly, both take rewarding shareholders seriously.

Image source: Getty Images

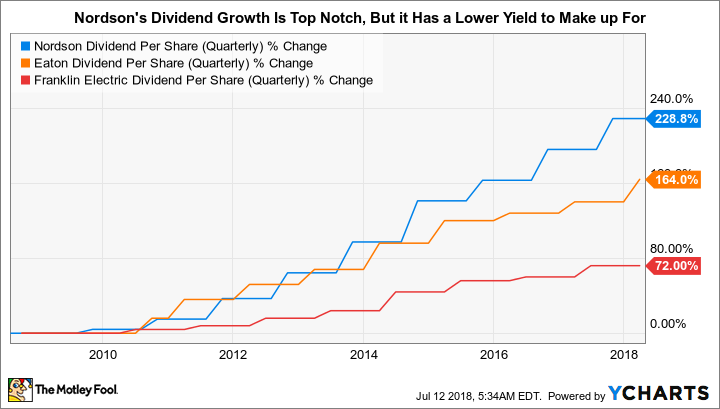

But annual increases are only part of the story. Another key attribute I look at is the rate of growth. Over the past decade, Franklin has increased its dividend at a compound annual rate of roughly 6% -- about twice the historical rate of inflation. Once again, Nordson's record is even better, with dividend growth over the past decade of around 12% a year -- an incredible four times the historical inflation rate.

The good news doesn't stop there. Neither company is overburdened with debt. Nordson is more leveraged, with long-term debt making up around 50% of the company's capital structure. That's a little high, but hardly outlandish, and certainly not enough to make me worry about the safety of the company's dividend. That's doubly true when you factor in the company's current ratio of 1.8, which shows it has plenty of resources to pay its near-term bills. Franklin, meanwhile, gets a gold star on the leverage front with long-term debt at just 15% of its capital structure, and a current ratio of 2.2.

Then there are these industrial companies' payout ratios. Franklin has generally paid out around 20% to 30% of its earnings annually over the past decade. Nordson's payout ratio has been in the 15% to 25% range over that time. A big part of this is to ensure financial flexibility in a cyclical industry, with protects the safety of the dividend over the long term. For example, the Great Recession caused their payout ratios to spike from 2007 to 2009, but their respective dividend streaks were never at risk because of the conservative payout ratios.

NDSN Dividend Per Share (Quarterly) data by YCharts

So far, both of these look like great dividend stocks -- until you check their yields. Franklin's is just 1%, and Nordson's is a mere 0.9%. Those trail well behind the 1.8% yield you could get from an S&P 500 Index fund like SPDR S&P 500 ETF. Even Nordson's 12% historical dividend growth rate isn't enough to make me consider it when I look at that paltry dividend yield.

This is why I own Eaton Corp.

While Franklin Electric are Nordson are both perfectly fine companies, as investments they just don't measure up to other alternatives in the industrial space.

For example, Eaton Corp., a stock I happen to own, currently yields roughly 3.4%. That company focuses on helping customers make efficient use of power, including in the electrical, hydraulic, aviation, and vehicle spaces. Despite a solid share price advance over the past few years, it still beats Franklin and Nordson in the yield department. A key reason for that is that Eaton has historically had a significantly higher payout ratio -- it has been in the 30% to 40% range in recent years, with occasional spikes above that.

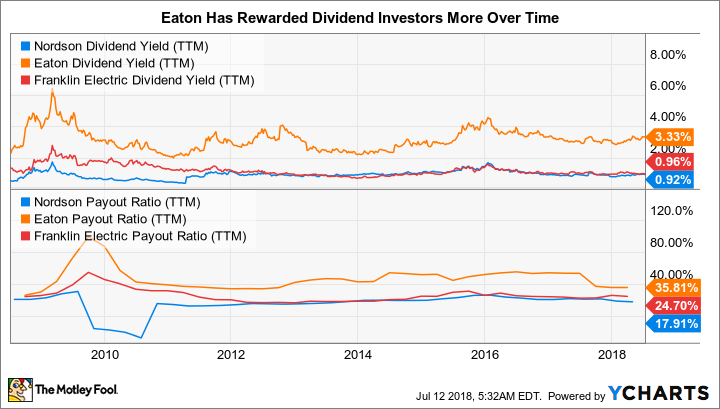

NDSN Dividend Yield (TTM) data by YCharts

Eaton's long-term debt is around 30% of its capital structure, and it has a current ratio of roughly 1.5 -- so its balance sheet is just as strong as those of Nordson and Franklin. Its annualized dividend growth over the past decade has been around 10%, so it stacks up well there, too. Where Eaton falls short is in the length of its dividend-hiking streak -- a mere nine years. But that's because the company paused its payout increases roughly a decade ago while it was integrating the largest acquisition it had ever made. I'm willing to forgive Eaton that "transgression," particularly given that the hiatus occurred when it was yielding around 5%.

I'll take the higher yield

All three of these companies are in the cyclical industrial sector, where strong balance sheets and reasonable payout ratios are especially good attributes to have. With their long streaks of annual dividend increases, they've all shown they have what it takes to survive and grow over time. However, Nordson and Franklin's dividend yields fall well short of being attractive. That doesn't make them bad companies, but it means income investors like myself just can't get excited about buying them. Which is one key reason why I gravitated to Eaton, and its far more impressive, market-beating yield. If you're a dividend investor considering opening a position in Nordson or Franklin Electric, I recommend you instead take a closer look at Eaton instead.

More From The Motley Fool

Reuben Gregg Brewer owns shares of Eaton. The Motley Fool owns shares of Nordson and has the following options: short January 2019 $285 calls on SPDR S&P; 500 and long January 2019 $255 puts on SPDR S&P; 500. The Motley Fool has a disclosure policy.