Yahoo Finance

Yahoo Finance 25 Retirement Rules to Live By

Source: Getty Images

1 of

Follow these guidelines for a stress-free retirement

Many, if not most, of us are looking forward to retirement. We may also be looking forward to living with fewer rules, such as how we need to dress for work, when we can take our lunch breaks, how long our vacations can be, and so on.

Don't expect a rule-free life, though, because even retirement has some important ones. Here's a look at 25 retirement rules that can help us plan more effectively for our futures and enjoy retirements that feature lots of financial security and not so much stress.

Previous

Next

Source: Getty Images

2 of

Retirement Rule No. 1: Deal with retirement now -- no matter how old you are

If you're 53 years old right now, you probably know that you need to be thinking about retirement, socking away money, and so on. If you're 28, though, retirement is probably not on your radar screen, as it's so far away. Similarly, if you're 67 and about to retire, you may not be thinking too hard about how you could optimize your retirement because it may seem a little too late to make much of a difference.

No matter how old you are, you could be short-changing your future significantly by not giving some thought to retirement -- and taking some actions. If you're 28, you have a whopping 37 years until you reach the common retirement age of 65. Socking away just $5,000 annually for 30 years will leave you with more than $1 million if it grows at an average annual rate of 8% -- and more than $1.8 million if it averages 10% growth.

Previous

Next

Source: Getty Images

3 of

Retirement Rule No. 2: Have a plan

The most important thing to do for your retirement is to have a good plan and to execute it well. Your plan might change over time, especially if you're still young, but starting out with one will help you save effectively. Grab a pad and pen and perhaps a calculator. Are your savings on track? How big does your nest egg need to be, and will it reach that size on schedule? How will you accumulate as much as you need to? What will your income streams be -- Social Security? Pension income? Dividend income? An annuity?

This simple online calculator can help with your planning. It's meant to calculate interest, but you can swap in your expected investment growth rate for the interest rate, and then try out different savings levels. For example, if you start with $0, sock away $7,500 per year, and expect it to grow by 8% annually, on average, over 25 years, you'll end up with about $592,000. Try different scenarios that are realistic for you.

ALSO READ: 3 Steps to a Smart Retirement Income Plan

Previous

Next

Source: Getty Images

4 of

Retirement Rule No. 3: Aim to make your money last

A critical retirement rule is that your savings and your income streams should last as long as you do. It's great if you retire at 65 with a million dollars, but you don't want to blow through it all by age 75.

So how much of your nest egg can you safely withdraw each year? A general rule of thumb is that withdrawing 4% of it in your first year of retirement and then adjusting the annual withdrawal for inflation after that is very likely to make your money last about 30 years. But the 4% rule isn't a guarantee and its usefulness depends on a variety of factors, such as market performance. Instead of following the rule closely, use it as a rough guide. You might, for example, withdraw more in years when the market surges and less when it swoons -- or use a 3.5% withdrawal rate instead of 4% in order to be more conservative.

Previous

Next

Source: Getty Images

5 of

Retirement Rule No. 4: Use the 4% rule to help estimate your required savings amount

That 4% rule is useful not only for estimating how much you can shave off your savings each year in retirement -- if you flip it around, it can help you determine how much money you'll need in retirement.

Here's how you might use it: Imagine that you're aiming for annual income of $60,000 in retirement, and you expect $25,000 to come from Social Security benefits. That leaves you needing to generate $35,000 on your own. How big a nest egg will generate that income? Well, dust off the 4% rule. Inverse the 4% and you'll get 25 (100 divided by 4% is 25). Multiply $35,000 by 25 and you'll arrive at $875,000, the nest egg you'll need if you want to apply the 4% rule. If you plan to use a more conservative 3.5% withdrawal, multiply the $35,000 by 28.6, and you'll arrive at a goal of $1 million.

ALSO READ: Have You Heard of the 4% Rule? Most Americans Haven't

Previous

Next

Source: Getty Images

6 of

Retirement Rule No. 5: Don't forget healthcare

Be sure to factor healthcare costs into your plans, because they're likely to be rather massive. A 65-year-old couple retiring today will spend, on average, a total of $275,000 out of pocket on health care, according to Fidelity Investments. That's an average, of course -- meaning you might spend less, or more. Spend a little time learning about Medicare and make smart decisions about it and you may be able to save more and spend less on health care. (One tip: Don't be late to enroll, as that can leave you paying higher premiums for the rest of your life. Most folks need to enroll within a few months of turning 65.

Previous

Next

Source: Getty Images

7 of

Retirement Rule No. 6: Don't forget inflation

We all know that prices for all kinds of things tend to go up over time, but we also often ignore that when planning our future spending. Inflation has historically averaged about 3% annually. That may seem small, but it adds up over time. For example, if you're trying to come up with an estimate of how much money you'll need in retirement and you're including travel costs, remember that a plane ticket that costs $500 today could cost $1,000 or more in 25 years. That's inflation at work.

Fortunately, Social Security benefits are increased over time to keep up (to some degree) with inflation. And if you're depending on dividend income, dividends tend to be increased over time, so that can help you keep up with inflation, too. If you get an annuity, you can choose to have those payouts indexed for inflation, as well.

Previous

Next

Source: Getty Images

8 of

Retirement Rule No. 7: Have a margin of error

It's smart to have a margin of error when you buy stocks, aiming to buy them for less than they're worth. It's also smart to have a margin of error in your retirement planning. Be conservative as you plan, thinking about worst-case scenarios.

For example, you may be figuring on a 20-year or 25-year retirement, perhaps from age 65 to 85 or 90, but lots of Americans are living well beyond that, many even reaching 100 and beyond. Be sure to consider the possibility that your retirement might last for 35 years or more -- especially if you retire early. That's a long time.

Previous

Next

Source: Getty Images

9 of

Retirement Rule No. 8: Get out of debt before retiring

It's also a good rule of thumb to pay off all your debt before retiring -- at least any credit card debt or other high-interest debt. It can be hard to pay off such debt when you're living on a reduced income, and having loan repayments to make can hurt your ability to make other necessary payments.

If you can swing it, aim to enter retirement mortgage-free, too, so that you don't have to make any mortgage payments and will only have to deal with your home's insurance, taxes, and maintenance.

ALSO READ: How Badly Will Debt Wreck Your Retirement?

Previous

Next

Source: Getty Images

10 of

Retirement Rule No. 9: Don't write off the stock market

Many people think of stocks as investments for younger folks and bonds as suited for older folks. It can indeed be sensible to think about shifting some assets from stocks to bonds or to more stable securities such as CDs as you approach and enter retirement. But even as you enter retirement, you don't have to be entirely out of the stock market.

Remember that if you have 20 or more years of retirement ahead of you, you won't be needing a big chunk of your money for at least 10 years, and it might remain in stocks, where it's likely to grow the fastest. You can aim to protect your capital by favoring stable, established blue chip stocks instead of would-be high-fliers. Dividend-paying stocks can be especially welcome for the income they generate.

Previous

Next

Source: Getty Images

11 of

Retirement Rule No. 10: Use retirement savings accounts

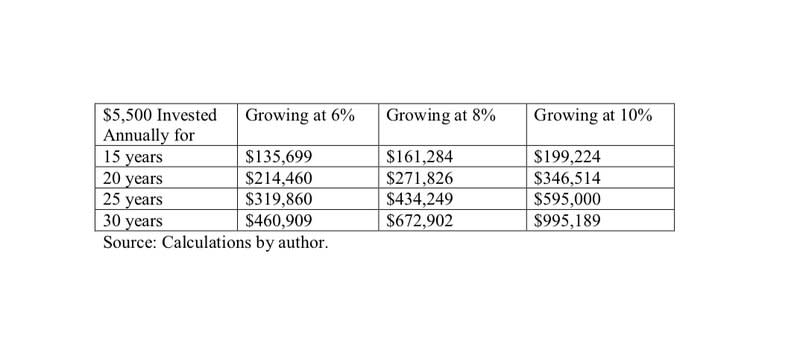

Make good use of the tax-advantaged retirement savings accounts available to you, such as IRAs and 401(k)s. The more you do so, the more money you'll have in retirement. There are two main kinds of IRAs -- the Roth IRA and the traditional IRA and for both in 2018, the contribution limit is $5,500 for most people and $6,500 for those 50 and older. (Limits are occasionally increased, to keep up with inflation.) That might not seem like a lot of money, but it's quite powerful if it can grow for many years. The table below shows how much money you can accumulate with annual $5,500 contributions at different average annual rates of growth:

Meanwhile, you might amass even greater sums via a 401(k), as it has much more generous contribution limits. For 2018, the limit is $18,500 for most people and $24,500 for those 50 or older. Give particular consideration to Roth IRAs and Roth 401(k)s (which are increasingly available), as they get funded with post-tax dollars and then let you withdraw money in retirement tax-free!

ALSO READ: IRA or 401(k): Which Is Better in 2018?

Previous

Next

Source: Getty Images

12 of

Retirement Rule No. 11: Know what to expect from Social Security

As part of your retirement planning, take the time to get an idea of how much money you can expect to receive from Social Security. A visit to the Social Security website at www.ssa.gov can help with that.

Retirement benefits for those with average earnings were designed to replace about 40% of pre-retirement earnings. The average Social Security retirement benefit was recently $1,375 per month, or about $16,500 per year. Those who had above-average earnings in their working years can expect a lower replacement rate, and vice versa. The maximum benefit for those retiring at their full retirement age was recently $2,687 per month -- or about $32,000 for the whole year.

It's good to know what to expect from Social Security in part so that we don't expect more from it than it's likely to deliver.

Previous

Next

Source: Getty Images

13 of

Retirement Rule No. 12: Understand how the Social Security benefit formula works

Your Social Security benefits are based on the income you earn in your 35 highest-earning working years (adjusted for inflation). If you've only worked 30 years, the formula will include five years' worth of zeroes, which will give you smaller benefit checks than if you'd worked for 35 years. If you work for more than 35 years, your lowest-earning years will be dropped, so working a little longer can be a way to boost your benefits. (Note that to qualify for benefits in the first place, you need to accumulate 40 work credits, which is typically achieved over 10 years of working.

Previous

Next

Source: Getty Images

14 of

Retirement Rule No. 13: Decide when to start collecting Social Security

When it comes to maximizing your Social Security income, one way to do so is to be strategic about when you start collecting benefits. You can start receiving benefits as early as age 62 and as late as age 70. For every year beyond your full retirement age that you delay starting to receive benefits, you'll increase their value by about 8% -- until age 70. So delaying from age 67 to 70 can leave you with checks about 24% fatter. Retire early, and your benefits may be up to about 30% smaller.

Note, though, that the system is designed so that total benefits received are about the same no matter when you start collecting, for those with average life spans. Checks that start arriving at age 62 will be considerably smaller, but you'll receive many more of them. Thus, it's not necessarily dumb to start collecting early -- and most retirees actually start collecting at age 62. Other ways to increase your Social Security benefits include working longer, earning more, and/or coordinating strategies with your spouse.

Previous

Next

Source: Getty Images

15 of

Retirement Rule No. 14: Coordinate your Social Security with your spouse

If you are or were married, read up on spousal strategies for Social Security. One good strategy for many married people is to start collecting the benefits of the spouse with the lower lifetime earnings record on time or early, while delaying starting to collect the benefits of the higher-earning spouse. That way, the couple does get some income earlier, and when the higher earner hits 70, they can collect extra-large checks. Also, should that higher-earning spouse die first, the spouse with the smaller earnings history can collect those bigger benefit checks.

Even divorcees can collect benefits based on their ex's earnings history -- if they were married for at least 10 years and have not remarried. Also, spouses can collect "spousal benefits" based on the other's earnings history, getting up to 50% of that spouse's benefits, while widows and widowers can choose to start receiving 100% of their late spouse's benefit instead of their own.

ALSO READ: 5 Surprising Facts About Social Security Spousal Benefits

Previous

Next

Source: Getty Images

16 of

Retirement Rule No. 15: Set up dividend income

Retirees need income streams to keep them afloat and one good way to generate income in retirement is via dividends. Sure, you could just sell off shares of stock from your stock portfolio over time -- but with dividend-paying stocks, you can collect income without having to sell any shares. A $300,000 portfolio, for example, that sports an overall average yield of 4% will generate about $12,000 per year -- a solid $1,000 per month. Dividend income isn't guaranteed, but if you spread your money across a bunch of healthy and growing companies, you'll likely receive regular -- and growing -- payments. Here are a few well-regarded stocks with significant dividend yields:

A dividend-focused exchange-traded fund (ETF) can be a fine option, offering instant diversification. The iShares Select Dividend ETF (NYSEMKT: DVY), for example, recently yielded about 3%. Preferred stock is another way to go. The iShares U.S. Preferred Stock ETF (NYSEMKT: PFF) recently yielded 5.6%.

Previous

Next

Source: Getty Images

17 of

Retirement Rule No. 16: Consider delaying retiring

If you've crunched your numbers and they don't look good -- or if you simply wish your nest egg were bigger -- a great way to plump it up is by working a little longer. It's not the most appealing option to many, but it can be very effective. If you can work two or three more years than you originally planned to, your nest egg can grow while you put off starting to tap it, thereby shrinking the number of years it will need to sustain you. You might enjoy your employer-sponsored health insurance for a few more years, too, perhaps also while collecting a few more years' worth of matching funds in your 401(k).

Here's what a difference this can make in your investing: Imagine that you sock away $10,000 per year for 20 years and it grows by an annual average of 8%, growing to about $494,000. If you can keep going for another three years, still averaging 8%, you'll end up with more than $657,000! That's more than $160,000 extra just for delaying retiring for a few years.

Previous

Next

Source: Getty Images

18 of

Retirement Rule No. 17: Consider working a little in retirement

Another good option is to ease into full retirement instead of jumping in feet first. If you're willing and able to work a little in your first few years of retirement, you can generate some helpful income. Working just 12 hours per week at $10 per hour, for example, will generate about $500 per month.

You might be able to switch to part-time status with your current employer, or you could switch into something entirely new. You could be a cashier at a local retailer or deliver newspapers. You might do some freelance writing or editing or graphic design work. You can tutor kids in subjects you know well, or give adults or kids music or language lessons. You might do some consulting -- perhaps even for your former employer. You could babysit, walk dogs, or take on some handy-person jobs. These days the Internet offers even more options. You might make jewelry, soaps, or sweaters, and sell them online.

Previous

Next

Source: Getty Images

19 of

Retirement Rule No. 18: Consider relocating -- for financial or familial reasons

Another way to strengthen your financial health in retirement is to relocate. If you downsize and move to a smaller home -- or you move to a region with lower taxes or a lower cost of living -- you can end up spending less on taxes, insurance, home maintenance, utilities, landscaping, and so on. The median home value in California, for example, was recently about $385,500, but it was only $247,800 in Colorado and only $139,900 in South Carolina.

Financial concerns aside, you might relocate simply to be closer to your kids or other family members. This option is worth thinking about and exploring early. If you move while you're still somewhat active, you might be able to make new friends and settle in in your new location. Moving late may leave you feeling more isolated and can even mean a move directly into a nursing facility that you didn't get to choose.

Previous

Next

Source: Getty Images

20 of

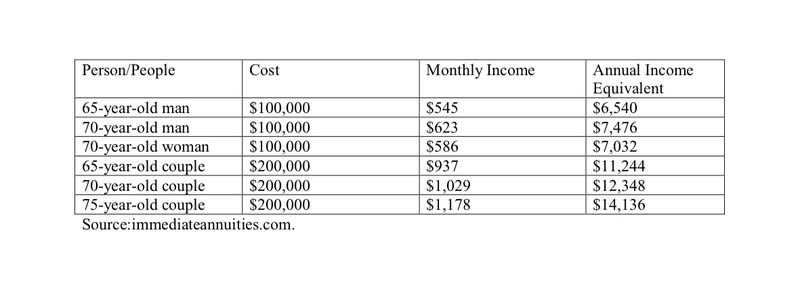

Retirement Rule No. 19: Consider immediate annuities for income

Since most of us don't have pension income to look forward to anymore, it's worth looking into buying your own dependable income stream, via a fixed immediate annuity. While some annuities, such as variable annuities and indexed annuities, can be quite problematic, often charging steep fees and sporting restrictive terms, fixed immediate annuities are well worth considering. They're much simpler instruments and they can start paying you immediately or on a deferred basis.

Below are examples of the kind of income that various people might be able to secure in the form of an immediate fixed annuity in the current economic environment. (You'll generally be offered higher payments in times of higher prevailing interest rates.)

Annuities can provide peace of mind, too, relieving you of the responsibility of managing a big chunk of your money and sending you regular checks. They lessen worries about stock-market moves and the economy's current condition, too.

Previous

Next

Source: Getty Images

21 of

Retirement Rule No. 20: Consider deferred annuities to avoid running out of money

Even if you've socked away a lot of money for retirement, you may reasonably still fear that it won't be enough, and that you'll run out of money before you run out of breath. You can prevent that by buying a deferred annuity (sometimes called longevity insurance). It's a fixed annuity, but one that doesn't start paying immediately. Instead, the insurer agrees to start paying at a future point, such as when you turn a certain age. For example, a 70-year-old man might spend $50,000 for an annuity that will start paying him $1,600 per month for the rest of his life beginning at age 85. That can remove any worries about running out of money late in life.

ALSO READ: Immediate vs. Deferred Annuity: Which Is Best for You?

Previous

Next

Source: Getty Images

22 of

Retirement Rule No. 21: Consider a reverse mortgage

Next, you might consider a reverse mortgage. It's essentially a loan secured by your home. A lender will provide (often tax-free) income during your retirement, and the loan doesn't have to be paid back until you no longer live in your home -- perhaps because you moved into a nursing home or, sadly, died. It has some drawbacks, though, such as requiring your heirs to sell your home unless they can afford to pay off the loan, but if you're really pinched for funds and no one is counting on inheriting your home, it can be a solid solution.

If this possibility interests you, learn a lot more about it before taking any action.

Previous

Next

Source: Getty Images

23 of

Retirement Rule No. 22: Borrow against your life insurance if you need to

Borrowing against your life insurance is another way to generate retirement funds. If you have a life insurance policy that no one is depending on -- for example, if the children you meant to protect with it are now grown and independent -- you might consider borrowing against your policy. This can work if you've bought "permanent" insurance such as whole life or universal life, and not term life insurance, that generally only lasts as long as you're paying for it. You'll be reducing or wiping out the value of the policy with your withdrawal(s), but if no one really needs the ultimate payout, it can make sense. As an added bonus, the income is typically tax-free.

Previous

Next

Source: Getty Images

24 of

Retirement Rule No. 23: Prepare in non-financial ways

As you prepare for retirement, don't neglect preparing for the non-financial aspects of it, too. Many people find themselves bored, restless, or lonely in retirement -- often to their surprise. The routine of working is more important to some of us than we realize. Brace yourself for that and consider how you might deal with its loss. Think about how you'll spend your days and try to come up with volunteering activities to sign up for, places where you might enjoy a low-stress part-time job, or new hobbies or interests to pursue.

Know that you'll probably need help in retirement, too, so expect that and perhaps practice asking for help now and then.

ALSO READ: 3 Sources of Retiree Stress -- and How to Deal With Them

Previous

Next

Source: Getty Images

25 of

Retirement Rule No. 24: Stay active -- physically and socially

Plan to stay active and social in retirement. It's important to stay active for your physical health, as that can keep your bones and heart strong and can lead to a longer life or at least a life with fewer health issues.

Being social has been shown to pay big dividends, too, such as keeping you mentally and physically healthier and possibly even keeping dementia at bay. Aim to not be too sedentary in retirement, sitting all day with books and crossword puzzles. Studies have found that those who sit for long periods are at greater risk of having or developing obesity, diabetes, cancer, heart disease, and muscular-skeletal disorders. This is even true for people who get ample exercise outside work. According to the folks at juststand.org, "People who sit for more than 11 hours a day have a 40% increased risk of death in the next three years, compared with people who sit for four hours or less."

Previous

Next

Source: Getty Images

26 of

Retirement Rule No. 25: Seek professional help, if you need it

Planning for retirement is a big deal and a big job. It's not unreasonable to feel intimidated and out of your comfort zone. There's no shame in tapping the expertise of a financial professional if you're so inclined. (It can even make sense if you're not so inclined -- yes, financial pros will charge you, but you may end up saving much more than you pay them.) Don't just go with anyone, though. Ask around for references and perhaps choose a fee-only planner instead of a pro who may have conflicts of interest from commissions earned by selling you various products. You'll find some local pros at www.napfa.org.

Selena Maranjian has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Previous

Next