Yahoo Finance

Yahoo Finance 3 Dividend Stocks With Better Yields Than Procter & Gamble

Procter & Gamble (NYSE: PG) has been a dream holding for dividend-focused investors. The consumer-staples giant has increased its payout every year for 60 years in a row. That's a track record that few companies can match.

With a dividend yield of 3% today, P&G's shares certainly look tempting. But can investors do better? To find out, we asked a team of investors to share a stock with a higher yield that P&G that they think is worth owning today. Here's why they picked Altria Group (NYSE: MO), Las Vegas Sands (NYSE: LVS), and Crown Castle Internation (NYSE: CCI).

Image source: Getty Images.

The biggest tobacco company in America

Leo Sun (Altria): Altria, the maker of Marlboro cigarettes, is the biggest U.S. tobacco company. It pays a forward dividend yield of 3.7%, and it's raised that payout every year since it spun off its overseas business as Philip Morris International (NYSE: PM) in 2008.

Altria spent just 30% of its earnings on those payments over the past 12 months. That payout ratio is at a historical low, thanks to the sale of its stake in brewer SABMiller to Anheuser-Busch InBev (NYSE: BUD) last year. That merger gave Altria a nearly 10% stake in the new company and $5.3 billion in pre-tax cash, and it boosted its annual pre-tax earnings by $13.7 billion.

It also reduced Altria's trailing P/E to 9, but the stock still trades at 20 times next year's earnings. Analysts expect its revenue and earnings to respectively rise 1% and 9% this year.

It might seem risky to invest in Altria as U.S. smoking rates are declining. However, Altria constantly raises cigarette prices, cuts costs, and repurchases stock to protect its earnings and dividends. It's also expanded into other markets -- including cigars, snuff, wine, and e-cigarettes -- to offset the softness of its core cigarette business.

Altria's business isn't built to last forever. But it's likely to last for decades before it runs out of room to raise prices of shares to repurchase. Until that happens, it will remain a safe income play for conservative investors.

A dividend that isn't a gamble

Travis Hoium (Las Vegas Sands): The biggest gambling company in the world is Las Vegas Sands, and it has some of the best cash-generating assets in the industry. That cash flow is what drives a 4.1% dividend yield, which will grow as the company raises its dividend to $3 per share in 2018.

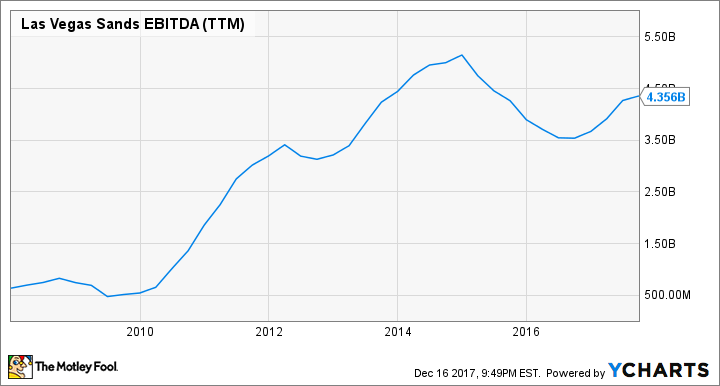

Most of the cash flow comes from Macau, where Las Vegas Sands is the industry leader. Adjusted property EBITDA was $652 million in the third quarter of 2017, or $2.6 billion on an annualized basis. On top of Macau, Marina Bay Sands in Singapore generated $442 million last quarter, or $1.8 billion on an annualized basis. Those two regions currently account for nearly 90% of adjusted EBITDA right now.

The wonderful thing about Las Vegas Sands' business is that most of the big expenses are up front when a resort and casino is built. After that, the property becomes a cash flow machine, which is why EBITDA, not net income, is used as a proxy for value creation. Las Vegas Sands currently has over $4 billion of EBITDA to draw from, and it doesn't have any major construction projects on the horizon, outside of maintaining its current properties.

LVS EBITDA (TTM) data by YCharts

Casino stocks aren't for every investor, but if you're looking for a high-yield dividend stock in the entertainment business, Las Vegas Sands is a top pick.

High yield and high growth

Brian Feroldi (Crown Castle International): The U.S. smartphone market is largely saturated, which has forced wireless carriers to step up their game to remain competitive. That's why all four major carriers now offer reasonably priced unlimited data plans. However, while this development has been great news for consumers, all that extra demand is putting a strain on the big boys' networks. In response, carriers are increasingly turning to tower owners such as Crown Castle International for help.

Crown Castle is a real estate investment trust that owns more than 40,000 cell towers spaced throughout the United States. The company rents out space on its towers to carriers who are looking to increase their capacity without having to make a big upfront investment. This creates a winning arrangement for all parties.

While the tower business has been kind to Crown Castle's investors over the long term, management is diversifying away from towers into the fiber-optic network business, too. The company currently has 32,000 miles of fiber in its empire, but that number is expected to nearly double soon, thanks to a pending $7.1 billion deal in the works.

Wall Street believes that between its tower and fiber-optics businesses, Crown Castle will drive long-term profit growth in the mid-teens for the foreseeable future. If true, then the company should easily be able to afford regular dividend bumps in the years ahead. That's a pretty compelling story for a stock that already yields a tempting 3.8%.

More From The Motley Fool

Brian Feroldi has no position in any of the stocks mentioned. Leo Sun owns shares of Las Vegas Sands. Travis Hoium owns shares of Procter & Gamble. The Motley Fool owns shares of and recommends Anheuser-Busch InBev NV and Crown Castle International. The Motley Fool has a disclosure policy.