Yahoo Finance

Yahoo Finance 3 Dividend Stocks to Fund Your Retirement Nest Egg

Whether you're eyeing a retirement date 10 years away or 40 years in the future, dividend stocks can play a crucial role in helping you to build long-term wealth. That's because they offer two opportunities to benefit from the power of compound interest: share gains and dividend growth.

For instance, tech giant Apple currently pays a dividend of $2.92 per share each year for a yield of about 1.3%. But if you had purchased shares a decade ago, you'd be enjoying a 19% dividend yield -- on top of some remarkable stock returns.

Of course, there's more to it than simply owning dividend stocks. You have to own great businesses that also happen to pay a dividend that's sustainable and has room to grow. We recently asked three contributors at The Motley Fool for stocks that fit this mold, and they argued for Enterprise Products Partners (NYSE: EPD), Microsoft (NASDAQ: MSFT), and Verizon Communications (NYSE: VZ). Here's why.

Image source: Getty Images.

A yield over 6% with great growth opportunities

Maxx Chatsko (Enterprise Products Partners): The company isn't a household name, but the nearly $60 billion business is an integral component of America's growing energy dominance. It owns and operates marine fuel terminals, natural gas pipelines, processing facilities, and an increasingly vertical stack of natural gas liquids (NGLs) infrastructure from dedicated pipelines, storage facilities, and even export terminals.

A solid infrastructure footprint positions the business to exploit numerous opportunities created by cheap natural gas and NGLs, such as the under-discussed $200 billion in investments being made to build new petrochemical manufacturing facilities in the United States. Successfully doing so will generate billions in cash flow every year (and soon, every quarter) that can be reinvested into the business or returned to unitholders. If third-quarter 2018 operating results are any indication, successful execution isn't an obstacle. The problem may be that there are too many projects available to invest in.

Enterprise Products Partners delivered record results on 16 different operational and financial metrics during the third quarter of 2018, including $1.6 billion in operating income. Management raised full-year 2018 guidance yet again as a result of the surprisingly strong performance. In addition to business growth, income investors will be pleased to know that the company can cover its massive distribution -- $1.73 per share per year, or a yield of 6.4% -- with ease. The business is generating the equivalent of $2.85 per share in distributable cash flow.

Simply put, Enterprise Products Partners offers a rare combination of above-average growth and income that could help to bolster any retirement fund.

Image source: Getty Images.

A technology stock for the ages

Todd Campbell (Microsoft): One of my favorite core holdings for dividend portfolios, Microsoft has proven it can pivot to take advantage of changing technology trends, making it great to own in long-haul portfolios.

The company has successfully diversified its revenue away from personal computer software. It still pockets plenty of money from sales of its Windows operating system, but increasingly, its sales are coming from subscriptions to cloud-based software solutions and video gaming.

In its most recently reported quarter, its productivity and business processes segment sales increased 19% year over year to $9.8 billion due to Office 365 commercial, Dynamics 365, and LinkedIn revenue growing 36%, 51%, and 33%, respectively. Its intelligent-cloud division did even better, as increasing demand for its server and cloud computing solutions increased revenue 24% to $5.9 billion in that segment. And, not to be left out, Microsoft's gaming sales increased 44% in the past year.

Overall, Microsoft's quarterly revenue was $29.1 billion, up 19% from one year ago, and its earnings per share were $1.14, up 36% from last year. All that cash that's coming into Microsoft allowed it to return $3.5 billion in dividends to investors last quarter, and I think the odds are good that the dividend will grow in the future. Its cash dividend payout ratio, which shows how much of a company's cash flow is being paid to common-stock holders after subtracting capital expenditures and preferred dividends, is only about 40%. That suggests it has plenty of dividend-friendly financial wiggle room.

Image source: Getty Images.

Can you hear me now?

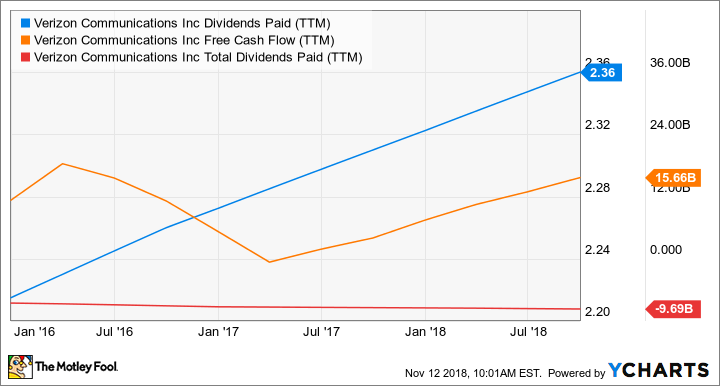

Travis Hoium (Verizon Communications): I think wireless giants like Verizon are some of the most overlooked stocks on the market right now, not just because of their dividends but because of their long-term growth potential. Verizon currently boasts a 4.3% dividend yield, and the dividend has been growing steadily for more than a decade.

VZ Dividends Paid (TTM) data by YCharts.

It may not seem like a saturated wireless industry would be a place to find much growth today, but 2018 will mark the initial launch of 5G networks in the U.S., which will change the industry forever. Not only will 5G take over cellphone connections, bringing broadband speed to mobile devices, but it will also allow Verizon to sell wireless services into the home. The first 5G products will be home routers that don't require a cable, phone, or fiber line to be run to the house; they just require a Verizon wireless router in range of a 5G network. That alone will allow Verizon to expand its potential market and offer bundles to existing wireless customers.

5G will also enable new technologies like self-driving cars, virtual- and augmented-reality networks, and connected cities. As one of the few wireless companies with the scale needed to build a 5G network, Verizon has an enviable position in the market and a dividend that I think has a lot of growth ahead for both revenue and your retirement nest egg.

More From The Motley Fool

Teresa Kersten, an employee of LinkedIn, a Microsoft subsidiary, is a member of The Motley Fool's board of directors. Maxx Chatsko has no position in any of the stocks mentioned. Todd Campbell owns shares of Apple and Microsoft. Travis Hoium owns shares of Apple and Verizon Communications. The Motley Fool owns shares of and recommends Apple. The Motley Fool owns shares of Microsoft and has the following options: long January 2020 $150 calls on Apple and short January 2020 $155 calls on Apple. The Motley Fool recommends Enterprise Products Partners and Verizon Communications. The Motley Fool has a disclosure policy.