Yahoo Finance

Yahoo Finance 3 Dividend Stocks That Are Minting Money

Dividend-paying stocks can be a gift that just keeps giving, minting money for shareholders who buy and hold. If you are trying to find some stocks with big yields, strong businesses, and plenty of opportunity for growth ahead, look no further than Eaton Corporation plc (NYSE: ETN), Duke Energy Corporation (NYSE: DUK), and Magellan Midstream Partners, L.P. (NYSE: MMP). Here's what you need to know about this trio of stocks and their dividends.

1. Power management

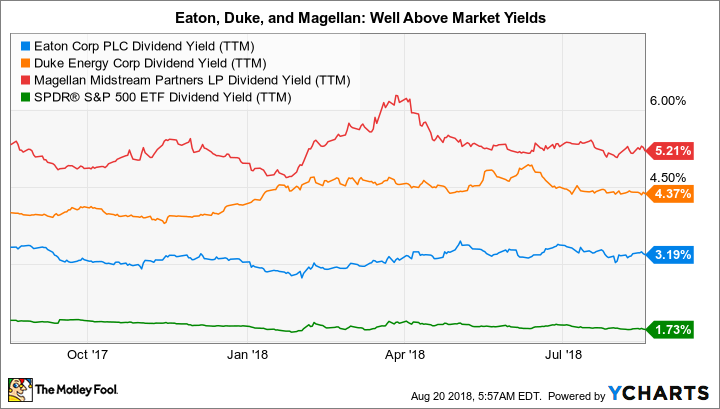

Eaton Corporation is a globally diversified industrial company focused on helping customers make the best use of energy. Its business is broken down into five main segments: electrical products (33% of second-quarter revenues), electrical systems and services (28%), vehicle (16%), hydraulics (13%), and aerospace (8%). It has increased its dividend annually for nine years after pausing increases following a large acquisition about a decade ago. The current yield is roughly 3.2%.

Image source: Getty Images.

The industrial giant has been performing quite well lately, with second-quarter earnings up 21% year over year and above the company's guidance. Organic growth, meanwhile, was up a strong 7%. The company upped the dividend a hefty 10% in the first quarter. Things are going well for Eaton right now.

But the company isn't done yet. For example, management believes that the bulk of the businesses it serves are in the early to mid stage of the economic cycle, suggesting there are several more years of growth ahead for Eaton. It also just introduced a new division called eMobility to serve the electric vehicle market. It's tiny today at around 1% of second-quarter sales (less than $100 million), but Eaton believes it could grow into a $4 billion revenue business by 2030 and is already winning contracts. With a big yield, a solid industry position, and growth opportunities ahead, Eaton is worth a deep dive for dividend investors.

2. A boring cornerstone

Duke Energy Corporation is one of the country's largest electric and natural gas utilities. The bulk of its business comes from its regulated electric utilities, which provide just under 90% of revenues. Natural gas contributes around 8%, with a renewable power merchant business pitching in the rest. Duke has increased its dividend annually for 14 consecutive years and currently yields around 4.5%.

The future for Duke is largely playing out in its spending on utility assets, which is set to total $37 billion between 2018 and 2022. The only way for regulated utilities to raise rates is to get approval from the government for rate hikes. The best way to do that is to spend money on upgrading its regulated assets. Duke expects its spending plans to drive earnings growth of 4% to 6% a year for the next several years, with dividend hikes of roughly the same amount.

ETN Dividend Per Share (Quarterly) data by YCharts.

The combination of a robust yield and slow and steady growth is enticing. But what makes Duke extra compelling is its ultra-low beta of 0.03. This is largely due to the fact that the shares haven't correlated well with the broader market, suggesting that it can provide you with income while also helping increase the diversification of your portfolio. That's a very nice combination of benefits, particularly if you are concerned about the market's lofty price levels.

3. Assets that can't be replaced

Magellan Midstream Partners is a limited partnership that owns the energy infrastructure that helps move oil and natural gas from where it is extracted to where it gets processed and to where it eventually gets used by end customers. These assets are largely fee-based, making Magellan a toll-taker business with assets that would be difficult, if not impossible, to replace. The current yield is 5.2%, and Magellan has increased its distribution for 18 consecutive years.

The quickest way for the partnership to expand its revenues is to build new midstream assets. On that front, Magellan is currently planning to spend around $2 billion on growth projects between 2018 and 2020. Run very conservatively, Magellan has customers lined up for most of the projects, or they are at facilities where demand has proven a need for expansion. This spending is expected to push distributions higher by 5% to 8% a year through 2020, with solid distribution coverage of 1.2 times throughout.

ETN Dividend Yield (TTM) data by YCharts.

Although the midstream sector has been a rough place to invest for a couple of years, Magellan is one of the best names in the space. And if you like to collect dividends, it is definitely worth the time to get to know this midstream partnership.

Collecting the checks

Eaton, Duke, and Magellan aren't very exciting stocks, but they do reliably send out large and growing dividend checks. If you are looking for investment opportunities that will mint money for your portfolio, each of them should be on your short list today. If you take a little time to get to know them, you might find that one or more fits nicely into your dividend portfolio.

More From The Motley Fool

Reuben Gregg Brewer owns shares of Eaton. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.