Yahoo Finance

Yahoo Finance 3 Great Income Stocks That Could Double Their Dividends

Savvy investors looking for income know that high yields aren't the whole story. A company that consistently increases its dividend can be even better to own as share prices tend to follow that dividend higher. To help with the search for a great payday, check out shares of Texas Roadhouse (NASDAQ: TXRH), TJX Companies (NYSE: TJX), and Apple (NASDAQ: AAPL).

What restaurant recession?

The single greatest boost to restaurant cash flows, which are used to pay dividends, is comparable-store sales. That metric was negative for the average restaurant for nearly two years starting in 2016 and has only just begun to turn a corner. While that has put a cap on profit growth for many chains, that has not been the case for Texas Roadhouse.

Image source: Getty Images.

The chain has been winning in suburban America with a fun-loving atmosphere and big portions at a value price. As a result, comps have been positive all through the so-called "restaurant recession," making Roadhouse a best-in-class winner. The topper? During the first quarter of 2018, comparable-sales were up 4.9% and 3.9% at company-owned and franchised stores, respectively. A month into the second quarter, management said company-owned comps were up 8.5%.

While restaurants are dealing with wage increases and some food inflation, Roadhouse's huge bump in traffic and ticket sizes should more than offset that. What that boils down to is free cash flow that is growing at a fast pace, which should support further hikes to its dividend that currently yields 1.7%.

Data by YCharts.

What retail apocalypse?

Much like the restaurant industry, brick-and-mortar retail has been in decline the last few years. The convenience of shopping online and increased ease of comparing prices has been taking a big bite out of foot traffic for many chains, but TJX Companies has bucked the trend.

The off-price treasure-hunt shopping experience offered by the company's TJ Maxx, Marshalls, and HomeGoods brands has been resilient, complementing the modern shopper's digital preferences rather than battling against them like other traditional retailers have been doing. As a demonstration of that, to kick off 2018 TJX Companies' comparable-sales rose 3%, and company wide revenues were up 12%.

Over the last five years, TJX has more than doubled its dividends paid to shareholders. The current yield is at 1.9%. Paired with an expected $2.5 billion to $3 billion in share repurchases through the rest of the year, this is one attractive dividend payer with a lot of room to boost that payout.

Data by YCharts.

Something even better than a dividend

Speaking of share repurchases, that's a commonly overlooked metric in the income-seeking investment world. It isn't as visible as a cash payment showing up in your account, but a share repurchase program -- where a company uses cash to buy its own stock -- boosts earnings per share and acts like a type of tax-free return to shareholders.

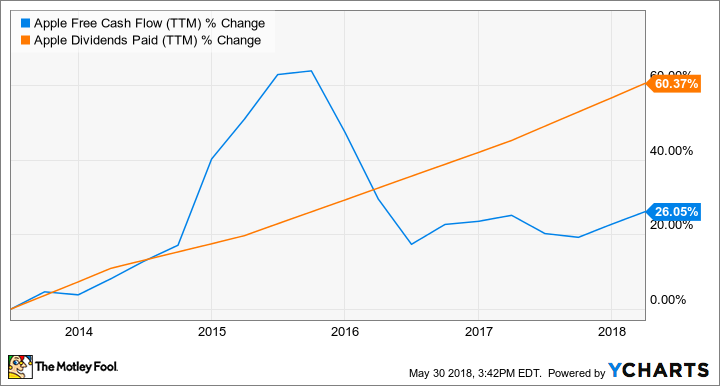

Tech giant Apple is hardly known for its dividend; the current yield sits at only 1.6%. The company uses a significant amount of free cash to develop new devices and grow its subscription services to complement its iPhone bread-and-butter, and revenues and earnings per share increased 16% and 30%, respectively, last quarter as a result.

Data by YCharts.

While the dividend may not look like much, Apple plans to use its iPhone cash cow to buy back a massive amount of its own stock in the coming year. Apple is authorized to spend $100 billion, which represents nearly 11% of its market cap as of this writing. Pair that with the dividend, which was simultaneously raised 16% with the new repurchase authorization, and income-oriented investors have a lot to like about Apple stock.

While there's no guarantee that these particular stocks will double their dividends, all three of them have something in common with companies that tend to do so: strong cash flow generation. Given their current payouts and positive outlook on boosting the bottom line, these look like great buys for investors who seek income from their portfolios.

More From The Motley Fool

Nicholas Rossolillo and his clients own shares of Apple and Texas Roadhouse. The Motley Fool owns shares of and recommends Apple and Texas Roadhouse. The Motley Fool has the following options: long January 2020 $150 calls on Apple and short January 2020 $155 calls on Apple. The Motley Fool has a disclosure policy.