Yahoo Finance

Yahoo Finance 3 Growth Stocks for the Long Term

The stock market is the world's most powerful wealth-creation tool. But while many people envision day traders raking in massive profits, maintaining such a short-term mentality can be dangerous and unpredictable. Rather, we know that buying and holding great stocks over the long term is the best way to predictably generate wealth.

So, we asked three top Motley Fool contributors to each find a growth stock for the long term. Read on to learn why they like 2U (NASDAQ: TWOU), Sirius XM (NASDAQ: SIRI), and Eaton (NYSE: ETN).

IMAGE SOURCE: GETTY IMAGES.

Education is evolving

Steve Symington (2U Inc.): Shares of online education platform leader 2U have pulled back around 15% from their 52-week high set in May, but that doesn't mean the company's actual business is suffering. To the contrary, 2U handily beat expectations with its latest quarterly report in August, including a narrower-than-expected net loss with revenue soaring nearly 50% year over year.

To be clear, 2U isn't profitable just yet; it typically absorbs the bulk of the cost structure up front when it launches new domestic graduate programs (DGPs). In return, the company receives the majority of tuition revenue -- a move that should prove massively profitable down the road considering its contracts typically last between 10 and 15 years. And 2U has been incredibly busy on that front, announcing eight new graduate programs last quarter alone with the likes of Dayton, Tufts University, Pepperdine, Baylor, and Fordham. That effort helped it fully slot its originally planned 16 DGP launches for 2019 earlier this month (a number it increased to 17 shortly thereafter due to university demand). In 2020 and 2021, 2U plans to further accelerate its launch cadence to 21 and 25 graduate programs, respectively. That will mean more than doubling 2U's current base to over 100 graduate programs, but it will still leave plenty of room to grow into its longer-term stateside target of 250.

What's more, thanks to its acquisition of online short-course specialist GetSmarter last year, the company enjoys a significant opportunity for incremental growth both internationally and with non-degree alternatives. On the former, 2U is set to launch its first international graduate program (IGP), an MBA with University College London, in 2019. And the latter comprised just 17% of 2U's total sales in the second quarter.

For investors willing to take advantage of the recent pullback and watch 2U's story play out, the stock could still offer tremendous gains.

A growth stock with an impenetrable moat? Yes, please

Sean Williams (Sirius XM Holdings): When talking about growth stocks with a set-it-and-forget-it quality, I gravitate toward a company I once swore I'd never like: satellite radio operator Sirius XM Holdings. After a tumultuous two decades, this investor is hooked on the idea of its long-term success.

One of the greatest aspects of the Sirius XM model is that it's predominantly based on subscription revenue. Receivers go into a number of new cars sold today, with auto dealerships and (hopefully) consumers paying a monthly fee to hear practically commercial-free service. In its most recently reported operating results, Sirius XM recorded $1.14 billion in service revenue, or roughly 80% of its top-line figure.

The remainder was comprised of $209.3 million in music royalty fees and "other" revenue, $36.8 million in equipment revenue, and just $47.2 million in advertising revenue. This is important because terrestrial and online radio are highly cyclical and heavily reliant on ad revenue to drive results. During economic downturns, subscription revenue is far less likely to be hit than ad revenue. That puts Sirius XM in prime position to fare better than all of its competitors when the next recession strikes.

It's also easy to appreciate Sirius XM's cost structure. While its revenue share, royalties, and programming costs can vary from quarter to quarter depending on the artists, hosts, and content it aims to bring to its subscribers, its equipment costs are relatively fixed. No matter how many subscribers Sirius XM adds -- it just added 483,000 subscribers in Q2 to 28.2 million -- its equipment costs are pretty much the same. That suggests a model that could lead to higher margins over time.

Finally, as the only satellite operator in town, Sirius XM should be able to stay ahead of the inflationary curve by passing price increases along to its subscribers as needed.

With the self-pay monthly churn rate hitting an all-time low of 1.6% in the second quarter, it's pretty clear that Sirius XM has made smart moves to keep its members happy. My bet, and that of Wall Street, which expects a near-doubling in EPS between 2017 and 2021, is that it'll do the same for investors over the long run.

A long-term standout

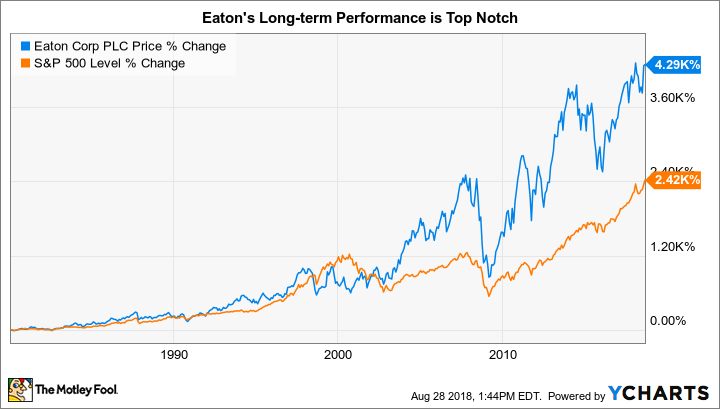

Reuben Gregg Brewer (Eaton Corporation plc): Industrial giant Eaton is a cyclical company that swings up and down with economic cycles. Pull back, though, and look at what the company has achieved over its history, including an over 4,300% stock price advance since 1980. And while the power management specialist happens to be firing on all cylinders today, it still looks relatively cheap.

The roughly 100-year-old company has a long history of shifting its business, often through acquisitions, to maximize shareholder value. Although it started out making truck axles, today, the company's business is broken into five major units serving a diversified collection of industries and a customer base that spans the globe.

Division | Q2 Sales | Q2 Operating Profit | Q2 Operating Margin |

|---|---|---|---|

Electrical products | $1.8 billion | $334 million | 18.5% |

Electrical systems and services | $1.5 billion | $227 million | 15% |

Vehicle | $899 million | $166 million | 18.5% |

Hydraulics | $723 million | $101 million | 14% |

Aerospace | $463 million | $90 million | 19.4% |

eMobility (NEW!) | $83 million | $14 million | 16.9% |

Data source: Eaton Corporation plc.

It continues to change with the times, recently adding eMobility, a sixth unit. It's tiny, producing just $83 million in quarterly sales, but management believes it could grow to a $4 billion business annually by 2030. All in, Eaton's got a balanced business mix focused on an increasingly important need (efficient power management) with a newly created catalyst (eMobility) to drive the top line.

Eaton isn't likely to excite you as much as a technology company, but it has proven that it has a corporate culture that knows how to adjust and grow a business over time. The eMobility segment, in which it is already winning contracts, is the latest example of that. What I like best, though, is that all of this comes at a reasonable price and with a pleasing 3.2% yield. That makes Eaton a good option for growth and income investors with a long-term bent.

More From The Motley Fool

Reuben Gregg Brewer owns shares of Eaton. Sean Williams has no position in any of the stocks mentioned. Steve Symington has no position in any of the stocks mentioned. The Motley Fool recommends 2U. The Motley Fool has a disclosure policy.