Yahoo Finance

Yahoo Finance 3 Reasons to Retain Merit Medical (MMSI) Stock in Your Portfolio

Merit Medical Systems, Inc. MMSI is well-poised for growth in the coming quarters, courtesy of its strong product portfolio. The optimism led by solid fourth-quarter 2022 performance and potential in its Cardiovascular unit are expected to contribute further. However, headwinds related to higher consolidation in the healthcare industry and stiff competition persist.

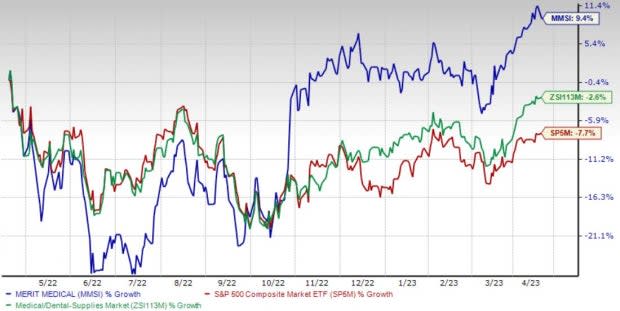

Over the past year, this Zacks Rank #3 (Hold) stock has gained 9.5% against a 2.5% decline of the industry and an 7.6% fall of the S&P 500.

This renowned medical devices provider has a market capitalization of $4.37 billion. The company projects 11% growth for the next five years and expects to maintain its strong performance. It has delivered an earnings surprise of 19.3% for the past four quarters, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strong Product Portfolio: Merit Medical has continued to gain significant momentum on the back of new products. The company is upbeat about the product pipeline, including radio and electrophysiology products, raising investors’ optimism. It has several electrophysiology products that are either on track for release or in several other stages of development.

In March, Merit Medical announced the expansion of its SwiftNINJA Steerable Microcatheter product line, which belongs to its delivery systems portfolio.

Potential in Cardiovascular Unit: Investors are optimistic about the unit’s robust potential. During the fourth quarter of 2022, Merit Medical witnessed a solid uptick in its Cardiovascular unit’s year-over-year revenues on a reported and at constant exchange rate, organic basis. Revenues in the unit’s majority of the product categories, Peripheral Intervention, Cardiac Intervention and original equipment manufacturer, were also robust during the fourth quarter.

Strong Q4 Results: Merit Medical’s robust fourth-quarter 2022 results buoy optimism. The company’s year-over-year uptick in the top and bottom lines was impressive. Robust performances in the United States and outside were impressive. Strong execution and improving customer demand trends pushed up the overall top line. The company stands to benefit from the execution of its global growth and profitability plan.

Downsides

Higher Consolidation in the Healthcare Industry: Healthcare costs have risen significantly over the past decade. Thus, to provide healthcare solutions at a cheaper rate and eradicate competition, large-cap MedTech behemoths have started consolidating with mid-cap and small-cap companies. This enables the availability of healthcare products at low prices in the market. Per management, such trends compel Merit Medical’s customers to ask for price concessions on its products, which acts against its ongoing business strategies. This may also exert a solid downward pressure on the prices of Merit Medical’s products and reduce the customer base.

Stiff Competition: Merit Medical operates in highly competitive markets, where it faces competition from many companies with greater resources. The company competes globally in several market areas, including radiology and interventional cardiology. Such resources and market presence may enable the competitors to market competing products more efficiently or at reduced prices to gain market share.

Estimate Trend

Merit Medical is witnessing a positive estimate revision trend for 2023. In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 1.1% north to $2.85.

The Zacks Consensus Estimate for the company’s first-quarter 2023 revenues is pegged at $280.8 million, suggesting a 1.9% rise from the year-ago quarter’s reported number.

This compares to our first-quarter 2023 revenue estimate of $279.6 million, suggesting a 1.5% improvement from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are IDEXX Laboratories, Inc. IDXX, Henry Schein, Inc. HSIC and Masimo Corporation MASI.

IDEXX Laboratories, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 18%. IDXX’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average beat being 3.6%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

IDEXX Laboratories has lost 3.9% compared with the industry’s 13% decline in the past year.

Henry Schein, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 8.1%. HSIC’s earnings surpassed estimates in three of the trailing four quarters and matched the same in the other, the average beat being 2.9%.

Henry Schein has lost 6.8% compared with the industry’s 2.5% decline over the past year.

Masimo, flaunting a Zacks Rank #1 at present, has an estimated growth rate of 3.5% for 2023. MASI’s earnings surpassed estimates in all the trailing four quarters, the average beat being 9%.

Masimo has gained 40.9% against the industry’s 13% decline over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Henry Schein, Inc. (HSIC) : Free Stock Analysis Report

Masimo Corporation (MASI) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

IDEXX Laboratories, Inc. (IDXX) : Free Stock Analysis Report