Yahoo Finance

Yahoo Finance 3 Stocks Poised for Huge Growth Over the Next Decade

Some of investors' best stories revolve around finding that one unheard-of stock that turned out to be a long-term wealth-generating powerhouse.

Finding stocks poised for huge growth isn't easy, however, or investors wouldn't put so much time and effort into uncovering the next game-changer. But three Fool.com contributors are intrigued by the potential of these stocks over the next decade, stocks which are certainly worth a deeper look: Control 4 (NASDAQ: CTRL), Axon Enterprise (NASDAQ: AAXN), and Charles Schwab (NYSE: SCHW).

Controlling long-term growth

Daniel Miller (Control4): If predicting which businesses would be thriving a decade from now were easy, we'd all be rich and retired by now.

While the future is uncertain, it seems likely that our future will be increasingly digitally connected. That's where Control4 comes in: It's a leading provider of networking systems for homes and businesses that offers a unified solution to control anything -- lighting, video, security, communications, music, and other smart-home devices. As the volume of connected devices increases in our homes and surrounding lives, Control4 seems well-positioned to thrive over the next decade.

The hype surrounding Control4 has been strong, but its valuation has finally come back down to planet Earth over the past couple of months. The decline could offer investors a great starting point, if they believe the company can offer compelling smart home solutions over the next decade. And there are a couple of factors that could help it do just that: acquisitions and brand awareness.

First, it's important to note these solutions from Control4 are for professionally installed systems; they typically control between 25 and 125 devices, and generally cost $1,000 to $50,000. This is a premium market aimed at households generating income over $150,000 annually, of which management believes the company has only penetrated roughly 1.5% -- so plenty of growth over the next decade remains.

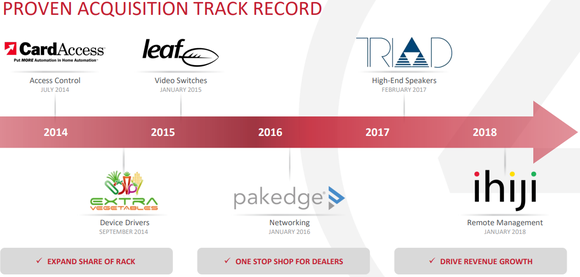

One reason to believe in Control4's future is its acquisition track record. Because smart devices and technologies are difficult to predict, a company like Control4 must be ready to scoop up innovative businesses, to keep itself positioned to take market share and grow. The recent graphic below shows its progress -- which it's made while keeping no debt on its balance sheet.

Image source: Control4 investor presentation, August 2018.

Control4 is also taking steps to grow its brand and product awareness. Many consumers don't yet comprehend the value of having everything connected, and may not for years to come. However, Control4 has recently opened a number of certified showrooms worldwide to essentially "wow" consumers and drive more effective leads and sales, while also improving its brand awareness. In fact, it had its second C4Yourself Day on Oct. 18, designed to show interior designers, builders, and architects how to work with consumers and professional installers of its products.

There could be many bumps in the road for Control4 over the next decade. But if it continues to impress consumers and installers with products, build its brand awareness, and scoop up innovating companies to bring into the mix, it could be poised for huge growth.

A long-tail bet on security

Jeremy Bowman (Axon Enterprises): It's not easy to predict the future. In business especially, change is constant, and in coming years some industries will inevitably go the way of camera film, VHS tapes, or the wagon wheel. However, one need that has persisted throughout human history and seems likely to continue is security. No technology can guarantee safety or disrupt the need for it. But one company that looks poised to grow on advances in security technology is Axon Enterprises.

Image source: Getty Images.

Axon is best known as the maker of Taser conductive electrical weapons, but the company does much more than that. It makes body cameras, fleet cameras, and Signal Sidearm sensors, which sit in the holster and detect when a gun is removed in order to start recording. It also runs Evidence.com, the largest cloud-based digital database of police evidence and other data, which pairs with the camera footage, allowing law enforcement agencies to easily manage and store data and evidence.

With ongoing calls for criminal-justice reform, body cameras are likely to proliferate and become the norm across agencies. Axon has scored several new contracts this year, including with Jacksonville County, Florida; Fort Worth, Texas; Charlotte, North Carolina; Boston; and other jurisdictions.

Axon has been delivering solid growth too. In its most recent quarter, revenue was up 16% to $104.8 million, but growth in its cloud segment and recurring revenue from software and sensors were much stronger, up 47% and 60% respectively. Gross margin surged 750 basis points to 62.6%, due in part to an improved mix in body-camera shipments, and adjusted earnings per share jumped from $0.05 to $0.20.

Axon is the market leader in this industry, and with growing demand for its products and services, the stock should thrive over the next decade and beyond.

A financial powerhouse

Jordan Wathen (Charles Schwab): You may know it as a brokerage, but Charles Schwab has a hidden gem in the form of a highly profitable banking operation that generates more than half its net revenue.

Charles Schwab is one of the most impressive asset gatherers around. The company uses its low-cost brokerage services to haul in brokerage and deposit assets on which it can earn fee and interest income. Customers move to Schwab for features like reimbursements of ATM fees around the world, and access to hundreds of ETFs they can trade for free.

These features help Schwab attract deposits despite its low deposit rates. In the most recent quarter, Schwab averaged $208.7 billion of deposit balances on which it paid a paltry annualized interest rate of 0.30%. It uses these deposits to invest in supersafe loans and securities, earning a healthy net interest margin of 2.33% despite the fact it takes almost no risk with its clients' cash.

Charles Schwab is well-positioned to benefit from a consolidating brokerage industry and plunging trading commissions, given that trading revenue was just 8% of net revenue in the first nine months of 2018. Unlike many of its peers, Schwab could survive, even thrive, in a world in which commissions on trades dropped to zero.

Over the next decade, I expect Charles Schwab to continue to haul in new accounts by the millions year after year. Its incredible pre-tax margin of 45% so far in 2018 could expand in the years ahead, as costs are spread across a larger asset base, and interest rates rise from multiyear lows.

More From The Motley Fool

Daniel Miller has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Axon Enterprise. The Motley Fool owns shares of Control4. The Motley Fool has a disclosure policy.