Yahoo Finance

Yahoo Finance 3 Stocks You Can Safely Own Until 2030

Over short periods of time, stock prices can be very volatile. And that short-term volatility is what makes stocks risky. But when you start stretching out your investing window beyond a year or two, and start measuring your ownership period in decades, the risk of permanent losses on your invested capital falls much lower. This is particularly the case when you own a diversified mix of stocks across multiple industries and sources of potential risk.

Furthermore, the long-term not only reduces your chances of permanent losses, but it also improves your chances of making substantial gains. This is the aspect of long-term, buy-and-hold investing that really pays off: Wealth creation. The best place to start? Owning great companies that can do well across a variety of economic conditions, have minimal risk of being disrupted by competition, and are run by excellent management with the chops to do well by both the business and its investors.

Image source: Getty Images.

We've compiled three excellent examples: Berkshire Hathaway Inc. Class B (NYSE: BRK-B), Electronic Arts Inc. (NASDAQ: EA), and Brookfield Infrastructure Partners L.P. (NYSE: BIP). Below, three real-world investors explain why these stocks are worth owning for at least the next dozen years.

Betting beyond Buffett

John Bromels (Berkshire Hathaway): Think Warren Buffett can make it to 100? The 87-year-old "Oracle of Omaha" just might pull it off. But even if Buffett doesn't make it to 2030, an investment in his diversified Berkshire Hathaway is almost certain to be thriving in 2030... and beyond.

Since 1965, Berkshire has pulled in annualized returns of about 20%, roughly double the overall market's returns of just under 10%. More impressive, Berkshire seldom invests in technology, thanks to Buffett's insistence that he only invest in businesses he can understand -- and more importantly, value -- meaning the portfolio's success is due more to savvy business analysis than lucking out on hot new tech.

But at some point, it's going to have to be "out with the old and in with the new" for Berkshire, since even Buffett can't live forever. Luckily, the company seems to be proceeding with succession in mind, recently appointing longtime Buffett disciples Ajit Jain and Gregory Abel as vice chairmen. Buffett himself praised both men, saying: "They both have Berkshire in their blood. They love the company. They know their operations like the back of their hand. So it's very good for Berkshire. And it's even better for me."

BRK.B stock price graph. Data source: YCharts.

It's also good for investors, who have seen the value of their Berkshire Hathaway shares increase 68% over the past five years. For many companies, I'd be concerned if they indicated it would be "business as usual" over the next decade, but for Berkshire, I'll gladly take more of the same.

Gamers for life

Daniel Miller (Electronic Arts): Much can change in 10 years, especially when it comes to business, but one trend that only seems to be gaining traction is gaming, and that makes Electronic Arts a stock you can safely own until 2030. During EA's May 17, 2018 investor day presentation, the company noted that 10 years ago the gaming player base was 200 million. That figure exploded to 1.5 billion five years ago and is currently pegged at 2.6 billion. EA's stock price has soared along with the growing player base and is up 547% over the past five years.

The good news is that the player base is not only expected to keep growing, but the gaming industry is evolving in favor of large publishers such as EA. Top gaming titles are driving a greater market share and fewer companies are producing those titles. EA has a list of incredibly popular franchises -- such as Star Wars Battlefront, NBA Live, Madden, SimCity, and many others -- that should continue to drive the company's results over the next decade.

EA stock price graph. Data source: YCharts.

Further, the gaming industry is becoming more digital and mobile, which should continue to drive margins and profitability higher. As the transition to digital occurs, EA has upside with its long-standing franchises because its loyal player base continues to come back for more expansions, sequels, microtransactions, and other downloadable content. EA also has a major catalyst as esports gains traction worldwide. The company will have to find ways to monetize competitive gaming, but if it can do that it will be another growth driver over the next 10 years.

As the gaming player base continues to grow, and more profitable digital downloads increase, EA is in a good position to capitalize on its list of popular game franchises and titles -- that makes it a stock you can safely hold until 2030.

Timeless assets we can't go without

Jason Hall (Brookfield Infrastructure Partners): If a company provides a necessary, in-demand good or service, and management allocates resources in a responsible way, that company should be able to remain relevant -- and profitable -- forever. And with lower risk of being disrupted than almost any other company out there, I think Brookfield Infrastructure Partners is the rare type of business that fits this mold.

Its core business is owning and operating critically important infrastructure assets in five areas: Telecommunications; water; energy; freight; and transportation. These assets are not only daily necessities for modern life, but many of Brookfield Infrastructure's operations are regionally regulated monopolies with incredibly high barriers to entry. The resulting business generates steady, predictable cash flow in every economic environment with limited risk of competitive disruption.

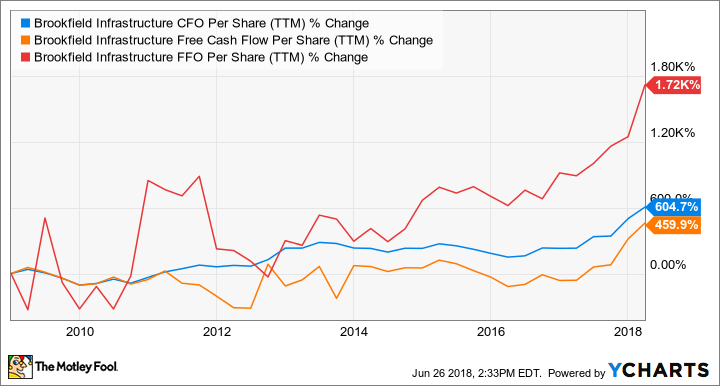

Furthermore, management has proven very skilled at capital allocation, whether putting cash to work via acquisitions or investments in organic expansion, or selling assets at a huge profit after having acquired them at a bargain price. This can be seen in how its cash flow and FFO -- funds from operations -- have steadily increased in the decade since going public:

BIP CFO Per Share (TTM). Data source: YCharts.

And with the global population on track to grow by more than 1 billion by 2030, Brookfield Infrastructure should make for both a relatively secure, and quite profitable, investment over the next dozen years. With a dividend yield approaching 4.8% and a very long path of growth ahead, there's a case for owning Brookfield Infrastructure for the rest of your life.

More From The Motley Fool

Daniel Miller has no position in any of the stocks mentioned. Jason Hall owns shares of Brookfield Infrastructure Partners. John Bromels owns shares of Berkshire Hathaway (B shares). The Motley Fool owns shares of and recommends Berkshire Hathaway (B shares). The Motley Fool recommends Electronic Arts. The Motley Fool has a disclosure policy.