Yahoo Finance

Yahoo Finance 3 Top Dividend Stocks to Buy Right Now

Everyone has their investing preferences, and people have studied the efficacy of various investing methods over the years. Unsurprisingly, all of those types of investing -- growth, value, income, etc. -- share one common trait: Buying and holding over long time periods.

If you are looking to buy a few stocks with that long-term strategy in mind, we have three dividend stocks for you. Here's why our Fool.com contributors think TerraForm Power (NASDAQ: TERP), China Mobile (NYSE: CHL), and Texas Roadhouse (NASDAQ: TXRH) are ones you should consider right now.

Image source: Getty Images.

New management, new investment opportunity

Tyler Crowe (TerraForm Power): When TerraForm Power was a subsidiary of its former parent, the now-bankrupt SunEdison, it was unsurprising that investors decided to tuck tail and run. When SunEdison went under, asset manager Brookfield Asset Management (NYSE: BAM) acquired TerraForm. That change of management is monumental to the investment thesis for TerraForm and its future.

On the surface, TerraForm was a solid business idea. It owned and operated a portfolio of solar and wind power generating assets that all had long-term power purchase agreements in place for years. The problem it ran into with SunEdison was that the parent company would sell it assets at rates that were favorable to SunEdison, and it used a lot of debt and equity to finance those deals. That strategy eventually put both TerraForm and SunEdison in a financial bind that led to the latter's bankruptcy.

The reason that having Brookfield at the helm is such a monumental change is that Brookfield's business strategy for these kinds of businesses is the exact opposite of SunEdison's. Rather than focusing on growth at all costs and relying heavily on external sources of capital, Brookfield's objective is to grow individual share value by acquiring assets selling at a discount and funding some of its growth with free cash flow. It has used this approach with all of its various partnerships -- there are a lot of them -- and it has been a pretty successful approach thus far.

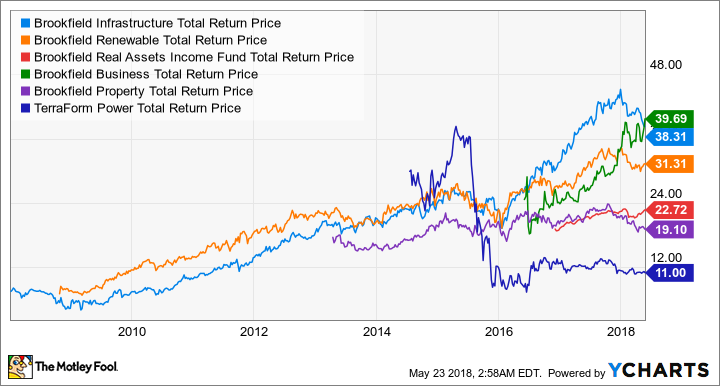

BIP Total Return Price data by YCharts.

Brookfield has to do a lot of cleaning up at TerraForm. It plans to wring out $25 million in operational costs and amortize close to $500 million in project-level debt. As Brookfield gets TerraForm in fighting shape, today's price looks like a great entry point.

China's top wireless carrier

Leo Sun (China Mobile): China Mobile, the largest wireless carrier in China, lost 16% of its market value over the past 12 months amid concerns about 5G expenses and ongoing trade tensions between the U.S. and China. However, the company remains one of the safest income plays in China.

China Mobile pays semiannual dividends that vary year to year based on its earnings growth, but its yield has generally stayed between 3% and 5% over the past five years. Its yield has consistently been higher than the dividends from its two main peers, China Unicom and China Telecom.

China Mobile, China Unicom, and China Telecom are all state-backed enterprises, and the Chinese government often rotates the management at the three telcos. That oversight provides a wide safety net and ensures that the three telcos collaborate on certain deals, like the sale of their towers to China Tower in late 2015.

China Mobile hit 899.7 million mobile subscribers in April, representing 4.6% growth from a year earlier. Within that total, its 4G customers jumped 16.7% to 669.3 million. Its wireline customer base also grew 44% to 127.1 million -- giving it a wider base for cross-selling bundled products.

Analysts expect China Mobile's sales and earnings to rise 3% and 1%, respectively, this year. That growth seems glacial, but its stock is also dirt cheap at 10 times this year's earnings. Investors looking for an overseas telco play with a low valuation and decent dividend should consider buying this stock.

Bucking the trend

Brian Feroldi (Texas Roadhouse): The last few years haven't been kind to most restaurant operators. Many chain restaurants have been expanding their store base so rapidly over the last decade that some industry watchers believe that the country is "over-restauranted." With scores of chains reporting declining or flat comps, it's hard to disagree.

However, even in these difficult times, a handful of top-notch operators have continued to thrive. Texas Roadhouse has increased its comps for several years in a row thanks to its focus on value pricing and creating a fun atmosphere for its guests. Last quarter the company posted total same-store sales growth of 4.9% at its company-owned restaurants. That's a number that any other restaurant chain would kill for.

Texas Roadhouse is also doing a fantastic job at translating the top-line gains into bottom-line success. Net income and EPS jumped by 59% and 58%, respectively, last quarter. While that's partially attributable to a lower tax bill, management is also driving margin expansion by keep its costs in check.

Looking ahead, I think that Texas Roadhouse can continue to thrive as it steadily grabs market share and opens new stores. Analysts think that will lead to 18% growth in EPS over the next five years, which is quite strong for a stock that costs around 22 times next year's earnings estimates. Throwing in a 1.6% dividend yield that only consumes 42% of profits is icing on the cake.

More From The Motley Fool

Brian Feroldi has no position in any of the stocks mentioned. Leo Sun owns shares of China Mobile. Tyler Crowe owns shares of Brookfield Asset Management and TerraForm Power. The Motley Fool owns shares of and recommends Texas Roadhouse. The Motley Fool has a disclosure policy.