Yahoo Finance

Yahoo Finance ASX Growth Companies With At Least 10% Insider Ownership

Despite a challenging day on the Australian market, with all sectors experiencing downturns influenced by factors such as low iron ore prices and international economic data, investors continue to seek stable opportunities in growth-oriented companies. High insider ownership can be a reassuring signal for potential stability and commitment from company leadership, particularly in turbulent times like these.

Top 10 Growth Companies With High Insider Ownership In Australia

Name | Insider Ownership | Earnings Growth |

Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

Cettire (ASX:CTT) | 28.7% | 29.9% |

Gratifii (ASX:GTI) | 15.6% | 112.4% |

Acrux (ASX:ACR) | 14.6% | 115.3% |

Doctor Care Anywhere Group (ASX:DOC) | 28.4% | 96.4% |

Plenti Group (ASX:PLT) | 12.8% | 106.4% |

Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

Change Financial (ASX:CCA) | 26.6% | 85.4% |

Botanix Pharmaceuticals (ASX:BOT) | 11.4% | 120.9% |

Liontown Resources (ASX:LTR) | 16.4% | 63.9% |

Underneath we present a selection of stocks filtered out by our screen.

Develop Global

Simply Wall St Growth Rating: ★★★★★☆

Overview: Develop Global Limited, along with its subsidiaries, focuses on the exploration and development of mineral resources in Australia, with a market capitalization of approximately A$538.69 million.

Operations: The company generates revenue primarily from mining services, totaling approximately A$109.75 million.

Insider Ownership: 17.7%

Develop Global Limited, recently added to the S&P/ASX 300 and Small Ordinaries Indexes, is poised for significant growth with revenue expected to increase by 54.2% per year, outpacing the Australian market's 5.3%. Although currently unprofitable, it is forecasted to achieve profitability within three years, a rate well above average market growth. However, potential investors should note concerns such as shareholder dilution over the past year and a short cash runway of less than one year.

Dive into the specifics of Develop Global here with our thorough growth forecast report.

Our valuation report here indicates Develop Global may be overvalued.

Ora Banda Mining

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ora Banda Mining Limited is an Australian company focused on the exploration, operation, and development of mineral properties, with a market capitalization of approximately A$640.52 million.

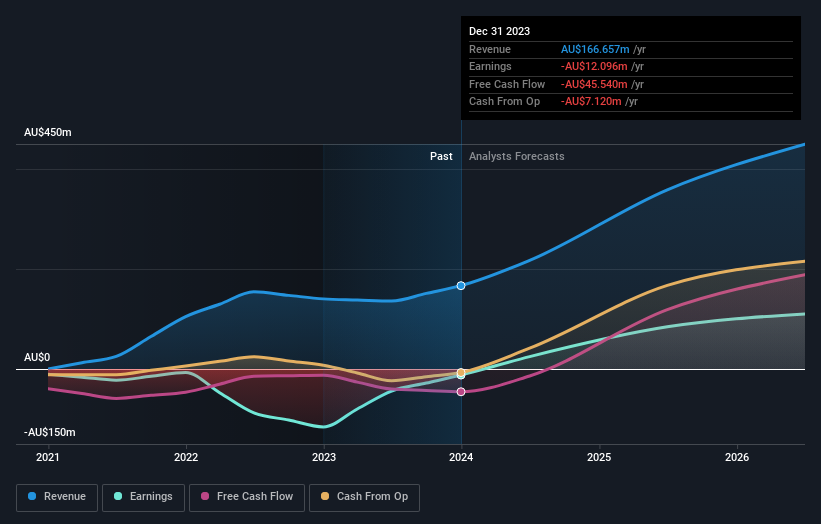

Operations: The company generates revenue primarily from gold mining, totaling A$166.66 million.

Insider Ownership: 10.2%

Ora Banda Mining, recently included in the S&P/ASX All Ordinaries Index, reported a significant turnaround with sales reaching A$96.35 million and net income of A$10.79 million for the half-year ended December 31, 2023, contrasting sharply with a loss the previous year. The company is trading at 89.7% below its estimated fair value and forecasts suggest an impressive revenue growth rate of 39.1% per year, outstripping the Australian market's average of 5.3%. However, shareholder dilution occurred over the past year despite no substantial insider trading activity reported in recent months.

Qualitas

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Qualitas operates as a real estate investment firm, engaging in direct investments across various real estate classes and geographies, acquisitions and restructuring of distressed debt, third-party capital raisings, and consulting services, with a market cap of approximately A$0.69 billion.

Operations: The company generates revenue through two primary segments: Direct Lending, which brought in A$27.58 million, and Funds Management, contributing A$19.32 million.

Insider Ownership: 27.1%

Qualitas Limited, highlighted at the ASX CEO Connect on June 7, 2024, shows a mixed financial forecast. While its revenue growth at 15.4% per year trails behind the desired 20% mark for high-growth entities, its earnings are expected to surge by a significant 25.1% annually over the next three years, outpacing the broader Australian market's average of 13.9%. However, challenges persist as its return on equity is projected to be modest at 10.6%, and its dividend coverage is weak with earnings not sufficiently covering a 3.3% yield.

Navigate through the intricacies of Qualitas with our comprehensive analyst estimates report here.

Upon reviewing our latest valuation report, Qualitas' share price might be too optimistic.

Where To Now?

Delve into our full catalog of 90 Fast Growing ASX Companies With High Insider Ownership here.

Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include ASX:DVP ASX:OBM and ASX:QAL

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com