Yahoo Finance

Yahoo Finance Is a Beat in Store for Simon Property (SPG) in Q1 Earnings?

Simon Property Group’s SPG first-quarter 2023 results are scheduled to be released on May 2, after the closing bell. The company’s quarterly results are likely to exhibit year-over-year growth in revenues and funds from operations (FFO) per share.

This Indianapolis, IN-based retail real estate investment trust (REIT) reported fourth-quarter 2022 comparable FFO per share of $3.15, exceeding the Zacks Consensus Estimate by a whisker. This performance was backed by a better-than-expected top line. Results reflected a healthy operating performance and growth in occupancy levels.

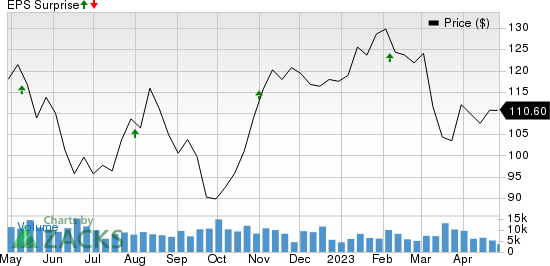

In the last four quarters, the company beat the Zacks Consensus Estimate on each occasion, the average surprise being 1.31%. This is depicted in the graph below:

Simon Property Group, Inc. Price and EPS Surprise

Simon Property Group, Inc. price-eps-surprise | Simon Property Group, Inc. Quote

Factors at Play

Per a report from CBRE Group CBRE, the United States retail real estate market remained resilient in first-quarter 2023, with the retail availability rate falling 50 basis points (bps) year over year to a new low of 4.8%.

The core retail sales climbed 50 bps to 7.7% from the prior quarter. The non-store retail sales of 9.8%, although falling 120 bps from the previous period, remained above core retail sales for the third consecutive quarter.

The EA asking rent for the first quarter was $22.97. Also, overall retail rent growth of 2% year over year remained above the 10-year average.

Retail space absorption was at 8.6 million square feet for first-quarter 2023, marking the 10th consecutive quarter of positive retail absorption per the CBRE Group report.

Simon Property’s portfolio of premium assets in the United States and abroad is anticipated to have benefited from the above-mentioned factors.

Amid growing consumers’ preference for in-person shopping experiences following the pandemic downtime, demand for SPG’s properties is likely to have remained healthy, aiding occupancy levels and leasing activity in the quarter.

The Zacks Consensus Estimate for first-quarter lease income is pegged at $1.24 billion, up from $1.21 billion reported in the year-ago quarter. The consensus mark for management fees and other revenues is $28.8 million, up 4.3% from the prior-year quarter’s reported figure. In addition, the consensus estimate for quarterly revenues is presently pegged at $1.34 billion, indicating an increase of 3.1% year over year.

Simon Property’s adoption of an omni-channel strategy and successful tie-ups with premium retailers are likely to have paid off well.

Moreover, its efforts to explore the mixed-use development option, which has gained immense popularity in recent years, is anticipated to have enabled it to tap the growth opportunities in areas where people prefer to live, work and play.

This March, Simon Property announced that it would collaborate with José Andrés Group to bring award-winning restaurants to several of the company’s premier properties. The move is likely to draw more shoppers to its shopping centers, making it a strategic fit.

Further, in the same month, SPG’s majority-owned operating partnership subsidiary, Simon Property Group, L.P., closed a new $5 billion multi-currency unsecured revolving credit facility, replacing the existing $4 billion senior unsecured revolving credit facility. This enhanced the company’s liquidity position and financial flexibility.

We expect the company’s robust balance sheet position to have supported its strategic expansions during the quarter to be reported.

However, the economic slowdown amid macroeconomic uncertainty and higher e-commerce adoption might have cast a pall on SPG’s performance in the to-be-reported quarter.

Also, rising interest rates might have raised expenses in the to-be-reported quarter.

The Zacks Consensus Estimate for FFO per share has been revised marginally downward over the past month to $2.80. Nonetheless, the figure indicates a slight increase from the year-ago quarter’s reported figure.

Earning Whispers

Our proven model predicts a surprise in terms of FFO per share for SPG this season. The combination of a positive Earnings ESP and a Zacks Rank #3 (Hold) or higher — increases the odds of a beat. That’s the case here.

Earnings ESP: Simon Property has an Earnings ESP of +1.23%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: SPG currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1(Strong Buy) Rank stocks here.

Other Stocks That Warrant a Look

Here are some other stocks that are worth considering from the retail REIT sector, as our model shows that these have the right combination of elements to deliver a surprise this reporting cycle:

Realty Income O is slated to report quarterly numbers on May 3. O has an Earnings ESP of +0.12% and carries a Zacks Rank of 3.

Federal Realty Investment Trust FRT is scheduled to report quarterly figures on May 4. FRT has an Earnings ESP of +0.57% and a Zacks Rank #3 currently.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Note: Anything related to earnings presented in this write-up represents FFO — a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Simon Property Group, Inc. (SPG) : Free Stock Analysis Report

Federal Realty Investment Trust (FRT) : Free Stock Analysis Report

Realty Income Corporation (O) : Free Stock Analysis Report

CBRE Group, Inc. (CBRE) : Free Stock Analysis Report