Yahoo Finance

Yahoo Finance Best Discounted Cylical Stocks in June

Cyclical companies are those that offer goods and services that are luxuries, instead of absolute necessities, such as entertainment and gambling. Currently, Hallenstein Glasson Holdings and Kathmandu Holdings are cyclical companies I’ve identified as potentially undervalued, meaning their share price is below what these companies are actually worth. There’s a few ways you can value a cyclical company. The most popular methods include discounting the company’s cash flows it is expected to create in the future, or comparing its price to its peers or the value of its assets. Analysing the most recent financial data, I’ve created a list of companies that compare favourably in all criteria, making them potentially good investments.

Hallenstein Glasson Holdings Limited (NZSE:HLG)

Hallenstein Glasson Holdings Limited, together with its subsidiaries, retails men’s and women’s clothing in New Zealand and Australia. Hallenstein Glasson Holdings was established in 1873 and with the company’s market cap sitting at NZD NZ$259.37M, it falls under the small-cap stocks category.

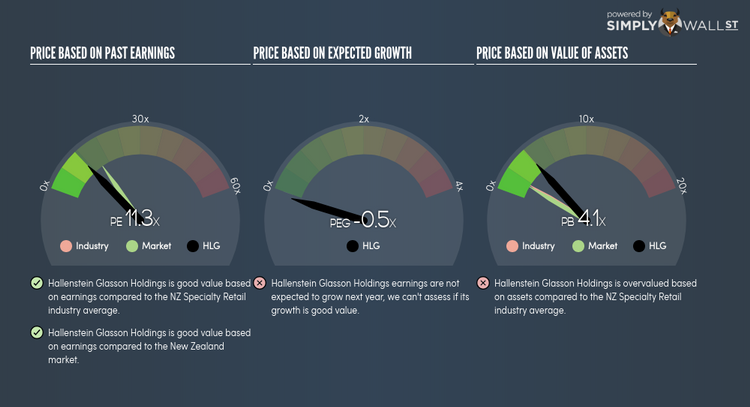

HLG’s shares are currently trading at -55% beneath its value of $9.74, at a price of NZ$4.40, according to my discounted cash flow model. This mismatch signals an opportunity to buy HLG shares at a discount. Furthermore, HLG’s PE ratio stands at around 11.3x relative to its Specialty Retail peer level of, 11.81x indicating that relative to its comparable set of companies, you can buy HLG for a cheaper price. HLG is also a financially healthy company, as near-term assets sufficiently cover liabilities in the near future as well as in the long run. HLG has zero debt on its books as well, meaning it has no long term debt obligations to worry about. Continue research on Hallenstein Glasson Holdings here.

Kathmandu Holdings Limited (NZSE:KMD)

Kathmandu Holdings Limited, together with its subsidiaries, designs, markets, and retails clothing and equipment for travel and adventure in New Zealand, Australia, and the United Kingdom. Established in 1987, and currently headed by CEO Xavier Simonet, the company provides employment to 1,273 people and has a market cap of NZD NZ$554.27M, putting it in the small-cap stocks category.

KMD’s shares are currently hovering at around -58% below its intrinsic value of $5.88, at a price of NZ$2.46, based on my discounted cash flow model. signalling an opportunity to buy the stock at a low price. Additionally, KMD’s PE ratio stands at around 12.32x against its its index peer level of, 15.12x indicating that relative to its comparable company group, you can buy KMD’s shares at a cheaper price. KMD is also in great financial shape, as current assets can cover liabilities in the near term and over the long run. Finally, its debt relative to equity is 6.14%, which has been declining for the past few years showing KMD’s capability to reduce its debt obligations year on year. Interested in Kathmandu Holdings? Find out more here.

The Warehouse Group Limited (NZSE:WHS)

The Warehouse Group Limited, together with its subsidiaries, engages in the retail of general merchandise and apparel in New Zealand. Started in 1982, and currently headed by CEO Nick Grayston, the company provides employment to 12,000 people and has a market cap of NZD NZ$699.33M, putting it in the small-cap group.

WHS’s stock is currently trading at -41% beneath its intrinsic value of $3.44, at the market price of NZ$2.03, based on my discounted cash flow model. This mismatch indicates a potential opportunity to buy low. Moreover, WHS’s PE ratio is trading at around 10.83x relative to its Multiline Retail peer level of, 15.9x meaning that relative to its peers, WHS’s stock can be bought at a cheaper price. WHS is also strong in terms of its financial health, with short-term assets covering liabilities in the near future as well as in the long run. It’s debt-to-equity ratio of 43.09% has been dropping over time, indicating WHS’s capability to reduce its debt obligations year on year. Continue research on Warehouse Group here.

For more financially sound, undervalued companies to add to your portfolio, explore this interactive list of undervalued stocks.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.