Yahoo Finance

Yahoo Finance Bio-Rad (BIO) Q1 Earnings Beat Estimates, Operating Margin Down

Bio-Rad Laboratories, Inc. BIO posted first-quarter 2023 adjusted earnings per share (EPS) of $3.34, which beat the Zacks Consensus Estimate by 3.1%. However, the bottom line declined 33.5% from the prior-year quarter.

The quarter’s adjustments eliminate the impacts of certain non-recurring items like the amortization of purchased intangibles, gains/losses from the change in the fair market value of equity securities and loan receivable, restructuring costs and others.

The GAAP EPS of the company was $2.32 per share in the first quarter against a GAAP loss of $112.5 in the year-ago quarter.

Revenues in Detail

Revenues of $676.8 million in the quarter beat the Zacks Consensus Estimate by 0.4%. However, revenues declined 3.3% from the year-ago quarter (down 0.3% at the constant exchange rate or CER). The company reported COVID-19-related revenues of $2.6 million, a significant decline from the $45 million reported a year ago.

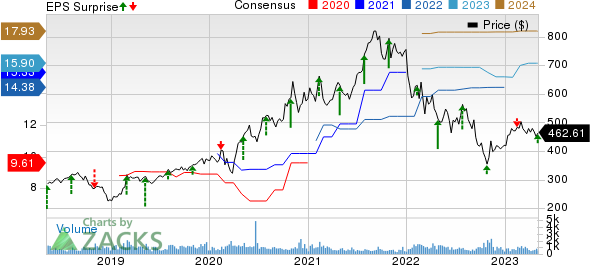

Bio-Rad Laboratories, Inc. Price, Consensus and EPS Surprise

Bio-Rad Laboratories, Inc. price-consensus-eps-surprise-chart | Bio-Rad Laboratories, Inc. Quote

Segmental Analysis

Sales in the Life Science segment in the first quarter totaled $323.6 million, down 6.8% year over year and 3.6% at CER. The sales decline was primarily due to lower COVID-19-related sales. Excluding pandemic-related sales, Life Science revenues increased 9.6%, primarily driven by Droplet Digital PCR, Western blotting, and qPCR products.

Net sales in the Clinical Diagnostics segment totaled $352.1 million, flat on a year-over-year basis and up 2.8% at CER. Apart from COVID-19-related sales, revenues increased 3.1% year over year, led by the robust demand for diagnostic instruments primarily within blood typing and diabetes.

Margins

In the quarter under review, Bio-Rad’s gross profit fell 10% to $362.4 million. The gross margin contracted 397 basis points (bps) to 53.6%. This can be attributed to lower pandemic-related sales, an unfavorable product mix and a higher cost of raw materials.

Operating expenses were $300.5 million in the first quarter, up 17.3% year over year. The operating profit totaled $62 million, reflecting a 57.7% decrease from the prior-year quarter. The operating margin in the first quarter contracted 1177 bps to 9.1%.

Financial Update

Bio-Rad exited the first quarter of 2023 with cash and cash equivalents (including short-term investments) of 1.85 billion compared with $1.80 billion at the end of 2022. Total debt (including current maturities) at the end of the first quarter was $1.20 billion, near the reported figure at the end of 2022.

The cumulative net cash flow from operating activities at the end of the first quarter of 2023 was $98.1 million compared with the year-ago figure of $50.5 million.

2023 Guidance

Bio-Rad updated its guidance for the full-year 2023.

The company anticipates currency-neutral revenue growth of approximately 4.5% (previously 6%-7%). Excluding pandemic-related sales, the company estimates currency-neutral 2023 revenue growth of 8.5% (earlier 10%-11%). The Zacks Consensus Estimate for revenues is pegged at $2.95 billion.

The adjusted operating margin projection for the full year is 17.5% (earlier 19.5%).

Our Take

Bio-Rad exited the first quarter of 2023 with an earnings beat, while revenues almost matched estimates. The demand for BIO’s newly launched ddPCR platform and QX600 continued to be strong in the first quarter. From its growing pipeline, Bio-Rad is set to introduce the ddPCR microsatellite instability kit towards the end of the quarter, expanding the company’s oncology assay menu for Droplet Digital PCR.

A significant decline in COVID-19-related sales impacted the year-over-year decrease in the quarter’s top line. Further, increased sanctions in Russia and headwinds related to early-stage biotech companies negatively affected BIO’s performance in the first quarter.

On the supply-chain front, Bio-Rad achieved a modest reduction of backlogs in the first quarter, short of its targeted reduction of approximately $30 million from the elevated 2022 backorders. BIO expects to clear the extended Life Science backlog by the end of the second quarter and the clinical backlog by the end of the year.

Meanwhile, a contraction in the adjusted operating margin also raises apprehension. BIO’s gross margin for the quarter was additionally impacted by the higher-than-anticipated percentage of instrument sales versus reagents and lower-than-forecasted revenues in the Life Science Group.

Zacks Rank & Key Picks

Bio-Rad currently carries a Zacks Rank #4 (Sell)

Some better-ranked stocks in the broader medical space that have announced quarterly results are Edwards Lifesciences Corporation EW, Intuitive Surgical, Inc. ISRG and Johnson & Johnson JNJ.

Edwards Lifesciences, carrying a Zacks Rank #2 (Buy), reported a first-quarter 2023 adjusted EPS of 62 cents, beating the Zacks Consensus Estimate by 1.6%. Revenues of $1.46 billion outpaced the consensus mark by 4.7%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Edwards Lifesciences has a long-term estimated growth rate of 6.8%. EW’s earnings surpassed estimates in two of the trailing four quarters, missed the same in one and broke even in the other, the average being 1.2%.

Intuitive Surgical, having a Zacks Rank #2, reported a first-quarter 2023 adjusted EPS of $1.23, which beat the Zacks Consensus Estimate by 3.4%. Revenues of $1.70 billion outpaced the consensus mark by 6.9%.

Intuitive Surgical has a long-term estimated growth rate of 13%. ISRG’s earnings surpassed estimates in two of the trailing four quarters and missed the same in the other two, the average being 1.9%.

Johnson & Johnson reported first-quarter 2023 adjusted earnings of $2.68 per share, beating the Zacks Consensus Estimate by 6.8%. Revenues of $24.75 billion surpassed the Zacks Consensus Estimate by 5%. It currently carries a Zacks Rank #2.

Johnson & Johnson has a long-term estimated growth rate of 5.5%. JNJ’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 3.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bio-Rad Laboratories, Inc. (BIO) : Free Stock Analysis Report

Johnson & Johnson (JNJ) : Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG) : Free Stock Analysis Report

Edwards Lifesciences Corporation (EW) : Free Stock Analysis Report