Yahoo Finance

Yahoo Finance Campbell Soup (CPB) Focuses on Saving Efforts Amid High Costs

Campbell Soup Company CPB has been benefiting from its focus on core priorities. The company’s Snacks business has been gaining traction due to the strength of its brands. However, like most other food companies, Campbell Soup is also battling input cost inflation, which is likely to persist. That said, this manufacturer and marketer of food and beverage products has been focused on its cost-saving plan.

Let’s delve deeper.

Focus on Core Priorities

Management recently outlined three important strategies to continue driving growth across the soup category. These priorities include reinforcing Campbell’s portfolio with solid brands, such as Campbell Soup's, Well Yes!, Pacific Foods, Chunky and Swanson and modernizing efforts, including new varieties and flavors and significant innovation. Management further cited that the sauces business is likely to grow to a $1-billion franchise through a 3% annual sales growth rate in the core business with brand and unit extensions. Campbell Soup’s Italian and Mexican sauce businesses gain momentum and are expected to continue expanding the market share. In addition, management targets plant-based growth with its unique plant-powered drink V8 and innovative offerings, such as V8 Plus Protein. The Pacific Foods brand is also performing impressively.

Image Source: Zacks Investment Research

Snacks Business & Brand Strength

Campbell Soup has been benefiting from the growth of its Snacks business. The segment formed 43.4% of CPB’s top line in the first quarter of fiscal 2022. Although net sales in the segment declined 1% year over year, it rose 4% from fiscal 2020. The company’s Snacks Power brands continue to fuel its performance, with in-market consumption growing 6% in the current fiscal and 13% on a two-year basis. Campbell Soup’s Snacks unit has been standing out for a while now. This business is likely to tap incremental sales, backed by a proven growth model, with strength in the power snacks brands and higher innovation. Management looks forward to enhancing its power brands’ distribution and channelizing its presence to grow revenues by $200 million.

The company remains encouraged by its brand strength. In fiscal 2021, 75% of the company’s brands increased or held shares compared with the year-ago period’s levels. Most of the company’s brands in the 13 core categories improved relatively compared with pre-pandemic levels. Also, in the first quarter, repeat rates on all eight power brands increased compared with fiscal 2020.

Inflation – a Worry

Campbell Soup has been struggling with cost inflation for a while. During the first quarter of fiscal 2022, the company’s adjusted gross margin contracted 200 basis points (bps) to 32.5%. The downside was caused by increased cost inflation, higher promotions and an unfavorable mix. Inflation, along with other factors, hurt the gross margin by 470 bps, mainly stemming from input cost inflation. The company, like other food players, is battling a high cost of ingredients, labor, packaging, warehousing and logistics. Adjusted EBIT plunged 15% to reach $389 million, mainly on account of lower sales volumes, reduced adjusted gross margin and elevated adjusted administrative expenses.

Management’s fiscal 2022 view includes accelerated inflation and a restricted labor market. In the second quarter of fiscal 2022, gross margin is expected to remain under pressure due to inflation across commodities and higher labor-related costs. Despite lapping easier comparisons in the second half of fiscal 2022, Campbell Soup expects inflation in high-single digits, which is anticipated to be more pronounced in the second half. Adjusted EBIT is forecast to be down 4.5-1.5% in fiscal 2022. For the fiscal, management expects net sales flat to down 2%, with organic sales between down 1% and up 1%. The sale of Plum baby food and snacks business is expected to affect fiscal 2022 sales by 1 percentage.

Will Saving Efforts Aid?

Campbell Soup is on track with a price rise in trade optimization, supply-chain productivity improvements as well as cost-saving initiatives. In the first quarter of fiscal 2022, CPB generated savings worth $15 million as part of its multi-year cost-saving program, which included synergies associated with the Snyder’s-Lance buyout. With this, the company generated total program-to-date savings of nearly $820 million. On its recent Investor Day, the company stated that it will increase its enterprise cost-saving program from $850 million to $1 billion by fiscal 2025 end.

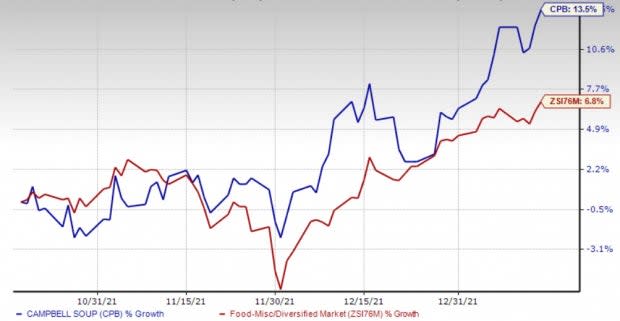

These upsides, along with Campbell Soup’s prudent investment and strategic efforts toward product innovation and brand building, bode well. Shares of this Zacks Rank #3 (Hold) company have rallied 13.5% in the past six months compared with the industry’s rise of 6.8%.

Hot Consumer Staple Bets

Some better-ranked stocks are United Natural Foods UNFI, Medifast, Inc. MED and The Estee Lauder Companies Inc. EL.

United Natural Foods, the leading distributor of natural, organic, and specialty food and non-food products in the United States and Canada, carries a Zacks Rank #1 (Strong Buy) at present. Shares of United Natural Foods have moved up 2.9% in the past six months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for United Natural Foods’ current financial-year sales and earnings per share (EPS) suggests growth of 4.8% and 7.7%, respectively, from the year-ago reported number. UNFI has a trailing four-quarter earnings surprise of 35.4%, on average.

Medifast, the manufacturer and distributor of weight loss, weight management, healthy living products, and other consumable health and nutritional products, currently carries a Zacks Rank #2 (Buy). Shares of Medifast have risen 3.8% in the past six months.

The Zacks Consensus Estimate for Medifast’s current financial-year sales and EPS suggests growth of about 63% and 49.3%, respectively, from the year-ago reported figure. MED has a trailing four-quarter earnings surprise of 17.3%, on average.

The Estee Lauder Companies, which manufactures, markets and sells skincare, makeup, fragrance and hair care products, carries a Zacks Rank #2 at present. Shares of The Estee Lauder Companies have moved up 1.2% in the past six months.

The Zacks Consensus Estimate for The Estee Lauder Companies’ current financial-year sales and EPS suggests growth of 15.5% and 15.2%, respectively, from the year-ago reported number. EL has a trailing four-quarter earnings surprise of 37%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Estee Lauder Companies Inc. (EL) : Free Stock Analysis Report

Campbell Soup Company (CPB) : Free Stock Analysis Report

United Natural Foods, Inc. (UNFI) : Free Stock Analysis Report

MEDIFAST INC (MED) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research