Yahoo Finance

Yahoo Finance Celgene Deal Starting to Pay Off Big for Bristol-Myers

Investors and analysts who questioned the wisdom of Bristol-Myers Squibb Co.'s (NYSE:BMY) purchase of Celgene last year for $74 billion might want to reconsider their opinion about the largest health care takeover in history.

Among those who frowned at the deal was Wellington Management, which owned nearly 8% of Bristol's shares. The investment management company thought the arrangement was too risky, that Bristol understated the ability to make the combination work and that the company could benefit shareholders more by being selling itself, according to an article in Fierce Biotech. Wellington's view was seconded by Starboard Value, another Bristol stakeholder.

Meanwhile, Wall Street analysts also had their concerns, including Cantor Fitzgerald analyst Alethia Young, who Forbes reported as expressing surprise at the deal. The naysayers had their effect on Bristol shares, which dropped by 12% on the announcement.

Those objections and others seem to be in the process of being put to rest now that the benefits of the acquisition have started to come to fruition. FierceBiotech reported that in the first of a series of online meetings that started on June 25, Bristol boosted its forecast of annual sales from its late-stage pipeline from $15 billion to $20 billion, starting in the second half of the decade. Six of the eight drugs that are expected to generate the revenue were obtained along with Celgene.

Two of those drugs received the Food and Drug Administration's approval even before the merger closed. Another was given the green light by the agency in March, but the company has delayed bringing it to market because of the Covid-19 pandemic. As for the other four, Bristol is expecting approval of the treatments later this year.

Looking further down the line, Bristol has a rich pipeline of drugs in early-stage testing, including 19 cancer assets, 15 in hematology, nine in immunology and five each in cardiovascular disease and fibrosis.

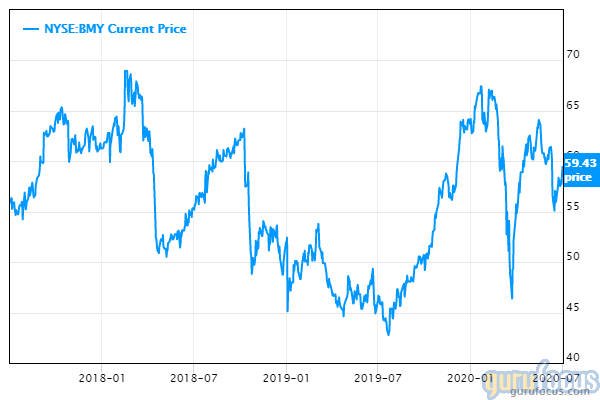

Company shareholoders hope they're rewarded for their patience. At $59.43, Bristol shares are 20% below where they were four years ago. The stock has fared well during the coronavirus crisis, climbing 28% from the first week in March. The $134 billion pharmaceutical giant pays a dividend of $1.80 per share, good for a yield of more than 3%, which is not too shabby in this era of miniscule interest rates.

In the first quarter, Bristol earnings and sales topped Zacks' consensus estimates. Earnings were $1.72, compared to Zacks' estimate of $1.48, and increased more than 56% from the same period a year earlier.

Revenue of $10.8 billion was well above the estimate of $9.9 billion and up more than 80% from a year earlier. Celgene products accounted for more than 70% of sales.

Bristol is trading under the 12-month low estimate of $62 offered by 11 analysts. The group pegs the high at $81 and the median at $73. The stock is rated a buy.

Disclosure: The author has a position in Bristol-Myers Squibb.

Read more here:

New Pharma ETF Focuses on Testing and Treatment for Infectious Diseases--but Not Covid-19

Invitae's Market Opportunity Grows to $45 Billion After Latest Acquisition

Acquiring Biomarin Would Speed Sanofi Transition to New Therapies

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.

This article first appeared on GuruFocus.