Yahoo Finance

Yahoo Finance China Mengniu Dairy And Other High Growth Stocks

High-growth stocks that are financially stable are attractive for many reasons. They provide a strong upside to your portfolio, with less likelihood of downside risks compared to less financially robust companies. I would suggest taking a look at my list of companies that compare favourably in all criteria, and consider whether they would add value to your current portfolio.

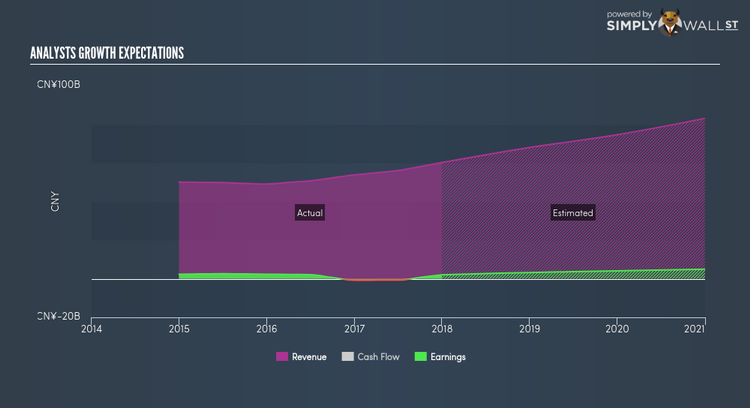

China Mengniu Dairy Company Limited (SEHK:2319)

China Mengniu Dairy Company Limited, an investment holding company, manufactures and distributes dairy products in the People’s Republic of China. Formed in 1999, and currently run by Minfang Lu, the company now has 41,141 employees and with the stock’s market cap sitting at HKD HK$115.46B, it comes under the large-cap stocks category.

2319’s projected future profit growth is a robust 26.73%, with an underlying 23.93% growth from its revenues expected over the upcoming years. An affirming signal is when net income increase is supported by top-line growth. Since net income isn’t artificially inflated by one-off initiatives such as cost-cutting, we know this profit growth is more likely to be sustainable. We see this bottom-line expansion directly benefiting shareholders, with expected positive return on equity of 16.13%. 2319’s bullish prospects on both the top and bottom lines make it an interesting stock to invest more time to understand how it can add value to your portfolio. Should you add 2319 to your portfolio? Have a browse through its key fundamentals here.

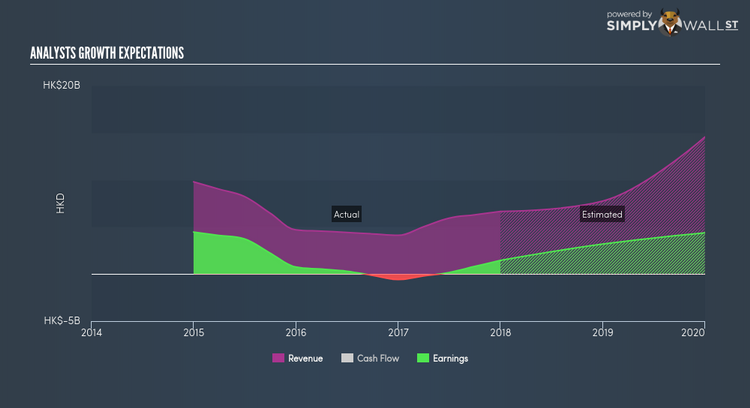

Shun Tak Holdings Limited (SEHK:242)

Shun Tak Holdings Limited, an investment holding company, engages in property, transportation, hospitality, and investment businesses in Hong Kong, Macau, and internationally. Founded in 1961, and headed by CEO Pansy Ho Chiu King, the company employs 3,390 people and with the stock’s market cap sitting at HKD HK$10.97B, it comes under the large-cap category.

242’s projected future profit growth is an exceptional 50.03%, with an underlying triple-digit growth from its revenues expected over the upcoming years. An affirming signal is when net income increase is supported by top-line growth. Since net income isn’t artificially inflated by one-off initiatives such as cost-cutting, we know this profit growth is more likely to be sustainable. This prospective profitability should trickle down to shareholders, with analysts expecting the company to generate a positive return on equity of 13.55%. 242’s bullish prospects on both the top and bottom lines make it an interesting stock to invest more time to understand how it can add value to your portfolio. Could this stock be your next pick? Take a look at its other fundamentals here.

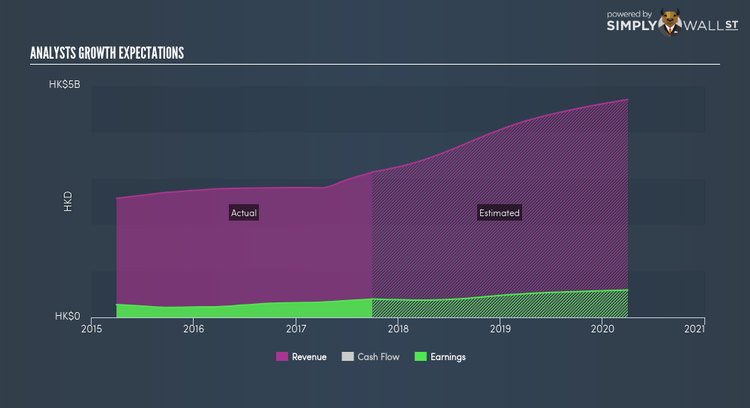

Nameson Holdings Limited (SEHK:1982)

Nameson Holdings Limited designs, manufactures, and sells knitwear products. Formed in 1990, and now run by Ting Chung Wong, the company now has 13,400 employees and with the market cap of HKD HK$3.44B, it falls under the mid-cap stocks category.

1982’s forecasted bottom line growth is an optimistic double-digit 22.35%, driven by the underlying double-digit sales growth of 42.56% over the next few years. It appears that 1982’s profitability may be sustainable as the fundamental push is top-line expansion rather than unmaintainable cost-cutting activities. This prospective profitability should trickle down to shareholders, with analysts expecting the company to generate a high double-digit return on equity of 22.20%. 1982’s impressive outlook on all aspects makes it a worthy company to spend more time to understand. Want to know more about 1982? I recommend researching its fundamentals here.

For more financially robust companies with high growth potential to enhance your portfolio, explore this interactive list of fast growing companies.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.