Yahoo Finance

Yahoo Finance Church & Dwight (CHD) Cuts Guidance Despite Q2 Earnings Beat

Church & Dwight Co., Inc. CHD reported second-quarter 2022 results, wherein the top line increased year over year, gaining from robust consumer demand. The bottom line remained flat as pricing was countered by cost inflation. Management curtailed its sales and earnings per share (EPS) growth guidance.

Quarter in Detail

Church & Dwight posted earnings of 76 cents per share, which beat the Zacks Consensus Estimate of 71 cents and remained in line with the adjusted EPS of the prior-year period. The bottom line included currency headwinds of 1 cent in the second quarter of 2022.

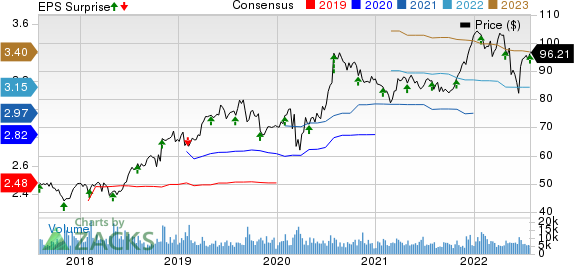

Church & Dwight Co., Inc. Price, Consensus and EPS Surprise

Church & Dwight Co., Inc. price-consensus-eps-surprise-chart | Church & Dwight Co., Inc. Quote

Net sales of $1,325.1 million moved up 4.2% year over year while missing the Zacks Consensus Estimate of $1,340 million. Results were backed by the solid consumption of the company’s brands due to strong demand. The company saw consumption gains in 11 out of 17 domestic categories.

Organic sales rose 3.4%, backed by the pricing gain of 6.3%, partially countered by a 2.9% dip in volumes. Also, contributions from buyouts aided performance, with both Zicam and Therabreath delivering a double-digit consumption increase. CHD concluded the integration of the Therabreath buyout.

The gross margin shrunk 220 basis points (bps) to 41.2% due to the adverse impacts of increased raw material, manufacturing and distribution costs, partly offset by better pricing, productivity and an improved mix.

Marketing expenses declined by $14.1 million year over year to $102.9 million. As a percentage of sales, the figure shrunk 140 bps to 7.8%. SG&A expenses, as a percentage of sales, fell 10 bps to 13.6% compared with adjusted SG&A expenses in the year-ago period.

Segmental Details

Consumer Domestic: Net sales in the segment increased 4.7% to $1,004.7 million due to higher household product sales. Organic sales improved 2.4%, driven by a higher price and product mix, somewhat negated by reduced volumes. Strength in ARM & HAMMER Liquid Detergent, ARM & HAMMER Cat Litter, BATISTE dry shampoo, OXICLEAN Versatile Stain Remover and ZICAM zinc supplements was countered by weakness in FLAWLESS and WATERPIK Shower Heads and the reduced consumption of vitamins.

Consumer International: Net sales in the segment rose 1.6% to $230.5 million, including currency woes of 5.6%. Organic sales were up 6.5%, with a higher price and product mix and volumes. The organic sales growth was mainly fueled by BATISTE in Europe, VMS and BATISTE in Canada along with an improvement in the GMG business.

Specialty Products: Sales in the segment advanced 6.3% to $89.9 million. Organic sales also jumped 6.3% on favorable pricing in the dairy and Specialty Chemicals businesses.

Other Updates

Church & Dwight ended the quarter with cash and cash equivalents of $639.7 million and total debt of $2.8 billion. In the first six months of 2022, cash from operating activities was $310.4 million. Capital expenditure amounted to $38.8 million in the same period.

For 2022, the company anticipates cash flow from operations of $900 million and capital expenditure of $180 million. Earlier, these metrics were anticipated at $920 million and $200 million, respectively.

2022 View

Management expects 2022 to turn out as another solid year for Church & Dwight, even in the face of a volatile landscape. It expects the robust consumption of value detergents in the second half of 2022 to be negated by sluggishness in discretionary brands like Waterpik and Flawless and reduced vitamin category consumption growth. Given that 40% of the company’s portfolio consists of value products, it remains well-placed for a potential recessionary landscape. The company expects the recent advancement in fill rates to continue throughout the back half of 2022 for most of its brands. Also, CHD remains focused on product innovation for 2022, which remains a key growth driver for the company.

Management now expects year-over-year sales growth of 4-5% compared with the earlier view of 5-8%. Organic sales are likely to rise 3-4% now compared with the earlier view of 3-6%.

Church & Dwight now expects to witness additional cost inflation of $135 million in 2022, $50 million higher than its earlier expectations. The incremental inflation is mainly associated with raw and packaging materials as well as the pass through of similar costs from third-party manufacturers. That said, it is on track to offset inflation via price increases, laundry concentration and productivity efforts. The company unveiled a new round of mid-to-high-single-digit pricing in April 2022 on certain products, which went into effect in July. However, management expects to face inflation at a greater rate than pricing and productivity in 2022.

For 2022, the gross margin is likely to be down from the 2021 reported level due to inflation, which is anticipated to more than offset pricing and productivity benefits. Marketing expenditure is anticipated to be lower in 2022 due to the reduced expenditure in the first half of the year stemming from lower fill levels. In the second half of 2022, marketing dollar spend is, however, likely to considerably increase from the first half.

Management now anticipates EPS to be flat year over year in 2022 with the adjusted EPS in 2021. Earlier, the metric was anticipated to grow at the lower end of the 4-8% range. The revised view reflects the impact of increased cost inflation and currency headwinds (of nearly 1%).

The bottom line is expected to be driven by the operating income growth of 6% (compared with the 10% projected before), offset by a 320-bps rise in the effective tax rate. In the second half of 2022, the EPS is again expected to be flat with 2021.

Q3 & Q4 View

For the third quarter of 2022, the company expects a roughly 2 to 4% increase in reported sales. Organic sales are estimated to rise nearly 1 to 3%. The organic sales view indicates a slowdown in discretionary brands like Waterpik and Flawless and a tough comparison for vitamins with the year-ago period’s Delta variant-led spike. EPS is projected at 65 cents in the third quarter, suggesting a 19% decline from the year-ago quarter’s adjusted figure, due to inflation, elevated expected SG&A expenses and promotional spend. The gross margin is likely to contract year over year.

In the fourth quarter of 2022, management expects increased organic growth and considerable EPS advancement due to increased trade down to its value portfolio, a rebound of fill rates in personal care and promotional support closer to pre-pandemic levels.

In the past three months, shares of this Zacks Rank #3 (Hold) company have dropped 6.3% compared with the industry’s decline of 7.1%.

Solid Consumer Staple Stocks

Some better-ranked stocks are The Chef's Warehouse CHEF, Sysco Corporation SYY and Campbell Soup CPB.

The Chef's Warehouse, which engages in the distribution of specialty food products, sports a Zacks Rank #1 (Strong Buy). The Chef's Warehouse has a trailing four-quarter earnings surprise of 372.3%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for CHEF’s current financial-year EPS suggests significant growth from the year-ago reported number.

Sysco, which engages in the marketing and distribution of various food and related products, sports a Zacks Rank #1. Sysco has a trailing four-quarter earnings surprise of 9.1%, on average.

The Zacks Consensus Estimate for SYY’s current financial-year sales suggests growth of 13.2% from the year-ago reported number.

Campbell Soup, which manufactures and markets food and beverage products, currently carries a Zacks Rank #2 (Buy). Campbell Soup has a trailing four-quarter earnings surprise of 10.8%, on average.

The Zacks Consensus Estimate for CPB’s current financial-year sales suggests growth of 0.5% from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Campbell Soup Company (CPB) : Free Stock Analysis Report

Church & Dwight Co., Inc. (CHD) : Free Stock Analysis Report

Sysco Corporation (SYY) : Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research