Yahoo Finance

Yahoo Finance Church & Dwight (CHD) Looks Troubled: Cost Inflation Key Worry

Several players in the consumer staple space are bearing the brunt of input cost inflation, and Church & Dwight Co., Inc. CHD is not immune to the same. The company’s second-quarter 2022 earnings results reflected continued cost-related headwinds, which prompted management to lower its earnings per share (EPS) growth guidance for 2022. CHD is also expecting a slowdown in certain brand sales and curtailed its sales view for the year.

The Zacks Consensus Estimate for 2022 EPS has declined from $3.16 to $3.02 in the past 30 days. The consensus mark for the third quarter has moved down from 87 cents to 68 cents per share.

Let’s take a closer look.

Church & Dwight Co., Inc. Price, Consensus and EPS Surprise

Church & Dwight Co., Inc. price-consensus-eps-surprise-chart | Church & Dwight Co., Inc. Quote

Cost Headwinds Persist

The company has been witnessing a shrinking gross margin for the past few quarters. During the second quarter of 2022, Church & Dwight’s gross margin shrunk 220 basis points (bps) to 41.2% due to the adverse impacts of increased raw material, manufacturing and distribution costs, partly offset by better pricing, productivity and an improved mix. On its second-quarter earnings call, Church & Dwight stated that it now expects to witness additional cost inflation of $135 million in 2022, $50 million higher than its earlier expectations. The incremental inflation is mainly associated with raw and packaging materials as well as the pass-through of similar costs from third-party manufacturers.

Though the company is undertaking pricing and productivity efforts to counter inflation, inflation is likely to come at a greater rate than pricing and productivity in 2022. For 2022, as well as the third quarter, the gross margin is likely to be down from the respective year-ago period levels. Apart from this, marketing dollar spend is likely to considerably increase in the second half of 2022 compared with the first half.

Image Source: Zacks Investment Research

Other Hurdles & Lowered Guidance

Due to its exposure to international markets, CHD remains vulnerable to currency fluctuations. This is because the strengthening of the U.S. dollar may require the company to either raise prices or contract profit margins at locations outside the United States. Currency headwinds are expected to hurt the 2022 EPS by nearly 1%.

For 2022, management now expects year-over-year sales growth of 4-5% compared with the earlier view of 5-8%. Organic sales are likely to rise 3-4% now compared with the earlier view of 3-6%. Management now anticipates EPS to be flat year over year in 2022 with the adjusted EPS in 2021. Earlier, the metric was anticipated to grow at the lower end of the 4-8% range. The revised view reflects the impact of increased cost inflation and currency headwinds (of nearly 1%). The bottom line is expected to be driven by the operating income growth of 6% (compared with the 10% projected before), offset by a 320-bps rise in the effective tax rate. In the second half of 2022, the EPS is again expected to be flat with 2021.

For the third quarter of 2022, the company expects a roughly 2 to 4% increase in reported sales. Organic sales are estimated to rise nearly 1 to 3%. The organic sales view indicates a slowdown in discretionary brands like Waterpik and Flawless and a tough comparison for vitamins with the year-ago period’s Delta variant-led spike. EPS is projected at 65 cents in the third quarter, suggesting a 19% decline from the year-ago quarter’s adjusted figure, due to inflation, elevated expected SG&A expenses and promotional spend.

Wrapping Up

Church & Dwight has been benefiting from favorable consumer demand and gains from buyouts. Also, the company has been undertaking incremental pricing across its portfolio to counter rising costs. However, the abovementioned headwinds cannot be ignored in the near term and remain concerns for this Zacks Rank #4 (Sell) company.

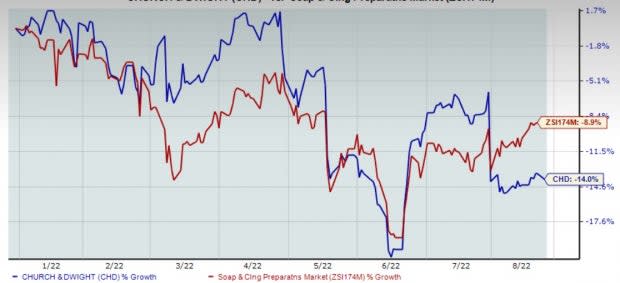

Shares of this New Jersey-based company have tumbled 14% in the year-to-date period compared with the industry’s decline of 8.9%.

Consumer Staple Stocks Worth a Look

Some better-ranked stocks are The Chef's Warehouse CHEF, Campbell Soup CPB and General Mills GIS.

The Chef's Warehouse, which engages in the distribution of specialty food products, sports a Zacks Rank #1 (Strong Buy). The Chef's Warehouse has a trailing four-quarter earnings surprise of 355.9%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for CHEF’s current financial-year bottom line suggests significant growth from the year-ago reported number.

Campbell Soup, which manufactures and markets food and beverage products, carries a Zacks Rank #2 (Buy). Campbell Soup has a trailing four-quarter earnings surprise of 10.8%, on average.

The Zacks Consensus Estimate for CPB’s current financial-year sales suggests growth of 0.8% from the year-ago reported number.

General Mills, which manufactures and markets branded consumer foods, currently carries a Zacks Rank #2. General Mills has a trailing four-quarter earnings surprise of 6.5%, on average.

The Zacks Consensus Estimate for GIS’ current financial-year sales suggests growth of nearly 2% from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

General Mills, Inc. (GIS) : Free Stock Analysis Report

Campbell Soup Company (CPB) : Free Stock Analysis Report

Church & Dwight Co., Inc. (CHD) : Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research