Yahoo Finance

Yahoo Finance Cleveland-Cliffs' Seasonal Slowdown Hit Earnings, but It Remains on Track

At first glance, Cleveland-Cliffs' (NYSE: CLF) most recent earnings report looks like a bit of a disappointment. After posting solidly profitable quarters that allowed management to reinstate its dividend and start a share buyback program, the slip into the loss column this most recent quarter might come as a surprise to some.

In reality, though, this is very much business as usual for the North American iron ore supplier, and management's estimates for the year remained pretty much undeterred by the slow quarter. So, let's take a look at why management is able to brush off this quarter's results so easily and what Cleveland-Cliffs has in store for the rest of 2019.

Image source: Getty Images.

By the numbers

Metric | Q1 2019 | Q4 2018 | Q1 2018 |

|---|---|---|---|

Revenue | $157.0 million | $696 million | $180.0 million |

Operating income | ($0.8 million) | $163.2 million | $30.3 million |

Net income | ($22.1 million) | $609.5 million | ($84.3 million) |

EPS (diluted) | ($0.08) | $1.98 | ($0.29) |

DATA SOURCE: CLEVELAND-CLIFFS EARNINGS RELEASE. EPS = EARNINGS PER SHARE.

The first quarter is always the seasonal low for the company as the locks it uses to ship iron ore to steelmakers are frozen and closed for much of the winter. For the quarter, the company only shipped about 1.55 million tons of ore. Most of that ore was transported via rail in the quarter, which is more expensive and leads to lower margins. Despite the low sales numbers in the quarter, management still expects to sell around 20 million tons of iron ore in 2019.

What was most encouraging about this most recent quarter was management's new projections for iron ore prices for the rest of the year. Based on the indicators it uses to price its contracts -- the Platts IODEX spot price, the price of hot rolled steel, and premium for high iron ore grade pellets in the Atlantic Basin -- it now projects per-ton prices to be in the $111 to $116 range. Management did note, though, that it believes prices will rise throughout the year because of mine closures in Brazil and the ripple effects that will have.

Despite the slow sales numbers for the quarter, management was not deterred from continuing to buy back shares. CFO Keith Koci noted that the company repurchased $125 million in stock during the quarter. Cleveland-Cliffs' board of directors also approved an additional $100 million in share repurchases and leaves management with authorization to repurchase up to $130 million in shares.

What management had to say

In the company's previous earnings release and conference call, management announced it was looking to restart operations at its idle Empire Taconite mine in Michigan to meet the needs of the North American iron ore market. On this quarter's call, though, CEO Lourenco Goncalves emphasized that the restart of this mine will only happen if certain conditions were met, and not simply because it is starting up a raw iron upgrading plant in the next couple of years.

Last quarter, I was asked if Cliffs had an ability to expand production to fill the shortfall. I brought up the possibility of an Empire mine restart, which would backfill these needs. However, we will not invest any capital at Empire unless we can secure a long-term take or pay guaranteed contract at the minimum price with the clients to lock in the IRR [internal rate of return] for the benefit of Cleveland-Cliffs.

Without this type of arrangement, we will not be bailing out any blast furnaces for their failure to think strategically about their long-term raw material needs. And the Empire Taconite reserves will remain on the ground. The HBI [hot briquetted iron] number one plant will be demanding that full allotment of pellets by the time certain contracts expired at the end of 2020. And if current operation rates hold, someone among the existing blast furnaces will be left to starving. The shifting market dynamics from blast furnace to EAF [electric arc furnace] is something we saw coming long ago. And that's why owning 100% of our HBI number one plant is so important to Cleveland-Cliffs. Thanks to our long-term strategic planning and flawless execution, regardless of who prevails in the battle of blast furnaces versus EAF, Cleveland-Cliffs is set up to win either way.

You can read a full transcript of Cleveland-Cliff's conference call here.

The comments about blast furnaces and electric-arc furnaces are fascinating because for years, Cleveland-Cliffs' entire business has been supplying blast furnaces. For years, Goncalves has said that he wants to start supplying electric arc furnaces, but to call out blast furnace operators for poor management is a bit surprising. Then again, Goncalves has never been one to mince words.

Still improving, and still cheap

For those investors who have been intrigued by Cleveland-Cliffs' incredibly cheap stock and its operating turnaround, this most recent quarter may have been a bit of a disappointment. Most of those results were seasonal, though, and the company remains on track to deliver on its sales, cash cost, and EBITDA projections for the year.

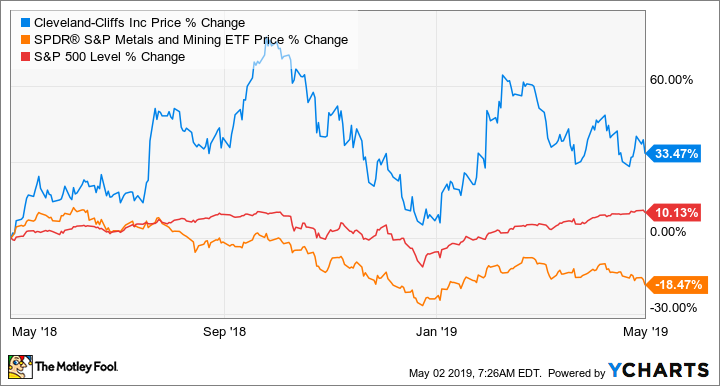

If the company can come remotely close to its EBITDA estimate for 2019 (more than $800 million), it would give the company an enterprise value to EBITDA ratio of 5.5 times. That's still an incredibly cheap stock despite its 33% gain over the past year. Considering the monumental turnaround management has executed here, and its current price, Cleveland-Cliffs continues to look like a great buy now.

More From The Motley Fool

Tyler Crowe owns shares of Cleveland-Cliffs. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.