Yahoo Finance

Yahoo Finance Clorox (CLX) Q2 Earnings and Sales Beat, Stock Rises 4.2%

The Clorox Company CLX reported second-quarter fiscal 2023 results, wherein the top and bottom lines beat the Zacks Consensus Estimate and our estimate. Results benefited from solid demand for its products and brands, owing to continued brand relevance. Cost-saving efforts, strong execution and pricing actions further aided the company’s performance. Sales and earnings rose year over year. The company updated its view for fiscal 2023.

Adjusted earnings of 98 cents per share improved 48% year over year and beat the Zacks Consensus Estimate of 65 cents and our estimate of 61 cents. Earnings benefited from pricing gains and cost savings, negated by lower volume, higher selling and administrative expenses, and increased commodity costs.

Net sales of $1,715 million rose 1% from the year-ago quarter and surpassed the Zacks Consensus Estimate of $1,666 million and our estimate of $1,647.5 million. On an organic basis, sales improved 4%. The increase in sales was attributed to a favorable price mix, partly offset by lower volume.

The Clorox Company Price, Consensus and EPS Surprise

The Clorox Company price-consensus-eps-surprise-chart | The Clorox Company Quote

The gross margin expanded 320 bps year over year to 36.2% in the fiscal second quarter. Gains from pricing and cost-saving initiatives were offset by elevated manufacturing and logistic costs, higher commodity costs and an unfavorable mix.

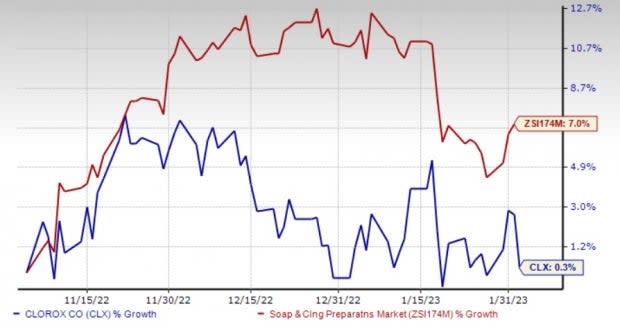

Driven by the robust second-quarter fiscal 2023 results and upbeat view, Clorox’s shares rose 4.2% in the after-hours trading session on Feb 2. Shares of the Zacks Rank #2 (Buy) company have gained 0.3% in the past three months compared with the industry’s 7% growth.

Image Source: Zacks Investment Research

Segmental Discussion

Sales of the Health and Wellness segment declined 2% to $635 million. The downside was led by a 19-point decline in volume, offset by a 17-point gain from a favorable price mix.

The Household segment’s sales improved 9% to $462 million. The increase in sales for the segment can be attributed to 6 points of pricing gains and 3 points of volume growth.

Sales in the Lifestyle segment rose 2% year over year to $332 million. The segment benefited from an 8-point gain from a favorable price mix, offset by a 6-point decline in volume.

In the International segment, sales of $286 million were down 3% year over year, driven by 8 points of volume decline and a 12-point impact from unfavorable currency, offset by a 17-point gain from a favorable price mix. Organic sales for the segment improved 9%.

Financials

Clorox ended second-quarter fiscal 2023 with cash and cash equivalents of $168 million, and long-term debt of $2,476 million. In the first half of fiscal 2023, the company generated $387 million of net cash from operations.

Fiscal 2023 Guidance

For fiscal 2023, the company envisions net sales between down 2% and up 1% year over year compared with the prior mentioned down 4% to up 2%. Organic sales are anticipated to be flat to up 3% versus down 3% to up 3% mentioned earlier. Currency headwinds are likely to impact sales by 2% in fiscal 2023.

The gross margin is expected to increase 200 bps in fiscal 2023, driven by the combined benefits of pricing actions, cost savings and supply-chain-optimization efforts, offset by continued cost inflation. The company expects selling and administrative expenses to be 15-16% of sales, including 1.5 points of impact from its strategic investments in digital capabilities and productivity enhancements.

The company anticipates advertising and sales promotion spending to be 10% of sales, driven by its commitment to investing in its brand portfolio. The effective tax rate is likely to be 24%.

The company expects adjusted earnings of $4.05-$4.30 per share for fiscal 2023 compared with the $3.85-$4.22 stated earlier. The guidance suggests a year-over-year decline of 1% to an increase of 5% versus a decline of 6% to an increase of 3% estimated earlier. The company’s earnings view excludes long-term investments in digital capabilities and productivity enhancements of 55 cents to provide greater visibility of the underlying operating performance. It also excludes the effects of the company’s streamlined operating model of 30 cents compared with the 20 cents stated earlier.

On a GAAP basis, earnings per share are anticipated to be $3.20-$3.45, suggesting a decline of 7-17% from the year-ago period’s reported number. Earlier, the company anticipated GAAP earnings of $3.10-$3.47, reflecting a decline of 7-17%.

Stocks to Consider

We highlighted some other top-ranked stocks from the broader Consumer Staples space, namely Procter & Gamble PG, Helen of Troy HELE and Inter Parfums IPAR.

Procter & Gamble currently flaunts a Zacks Rank #2. PG has a trailing four-quarter earnings surprise of 1.1%, on average. It has a long-term earnings growth rate of 6.1%. The company has gained 5.7% in the past three months.

You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Procter & Gamble’s current financial-year sales and earnings per share suggests growth of 0.4% and 0.5%, respectively, from the year-ago reported numbers. The consensus mark for PG’s earnings per share has moved up by a penny in the past 30 days.

Helen of Troy currently sports a Zacks Rank of 2. HELE has a trailing four-quarter earnings surprise of 13.4%, on average. It has a long-term earnings growth rate of 8%. The company has rallied 40.3% in the past three months.

The Zacks Consensus Estimate for Helen of Troy’s current financial-year sales and earnings suggests declines of 8% and 24.6%, respectively, from the prior-year reported numbers. The consensus mark for HELE’s earnings per share has moved up 1% in the past 30 days.

Inter Parfums currently has a Zacks Rank #2 and an expected long-term earnings growth rate of 15%. IPAR has a trailing four-quarter earnings surprise of 27.8%, on average. The company has rallied 46.6% in the past three months.

The Zacks Consensus Estimate for Inter Parfums’ current financial-year sales and earnings suggests growth of 23.6% and 29.5%, respectively, from the year-ago reported numbers. The consensus mark for IPAR’s earnings per share has moved up 4.7% in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Procter & Gamble Company (The) (PG) : Free Stock Analysis Report

The Clorox Company (CLX) : Free Stock Analysis Report

Helen of Troy Limited (HELE) : Free Stock Analysis Report

Inter Parfums, Inc. (IPAR) : Free Stock Analysis Report