Yahoo Finance

Yahoo Finance Some Colour Life Services Group (HKG:1778) Shareholders Are Down 12%

Colour Life Services Group Co., Limited (HKG:1778) shareholders will doubtless be very grateful to see the share price up 37% in the last quarter. But in truth the last year hasn't been good for the share price. In fact the stock is down 12% in the last year, well below the market return.

See our latest analysis for Colour Life Services Group

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

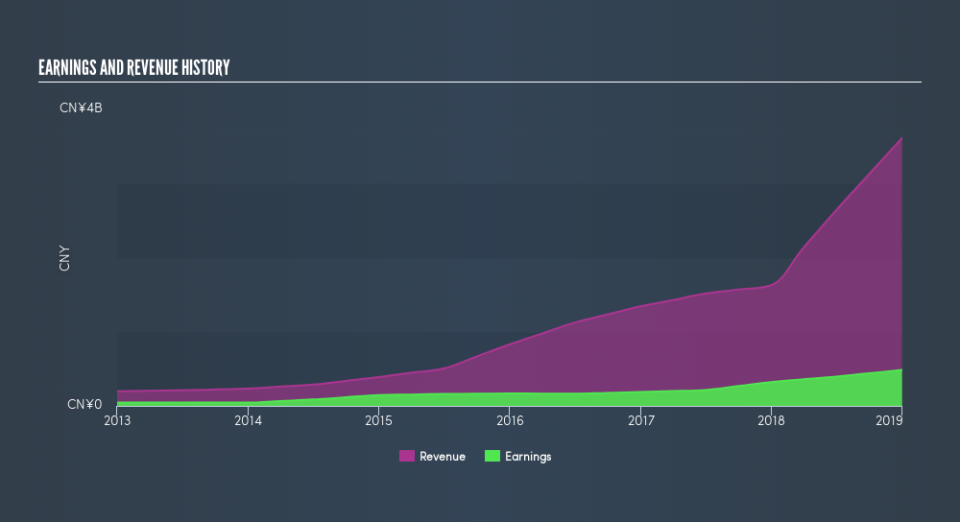

During the unfortunate twelve months during which the Colour Life Services Group share price fell, it actually saw its earnings per share (EPS) improve by 18%. Of course, the situation might betray previous over-optimism about growth. The divergence between the EPS and the share price is quite notable, during the year. So it's well worth checking out some other metrics, too.

Colour Life Services Group managed to grow revenue over the last year, which is usually a real positive. Since the fundamental metrics don't readily explain the share price drop, there might be an opportunity if the market has overreacted.

The chart below shows how revenue and earnings have changed with time, (if you click on the chart you can see the actual values).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. So it makes a lot of sense to check out what analysts think Colour Life Services Group will earn in the future (free profit forecasts)

What about the Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Colour Life Services Group's total shareholder return (TSR) and its share price return. Arguably the TSR is a more complete return calculation because it accounts for the value of dividends (as if they were reinvested), along with the hypothetical value of any discounted capital that have been offered to shareholders. Dividends have been really beneficial for Colour Life Services Group shareholders, and that cash payout explains why its total shareholder loss of 10.0%, over the last year, isn't as bad as the share price return.

A Different Perspective

The last twelve months weren't great for Colour Life Services Group shares, which performed worse than the market, costing holders 10.0%, including dividends. Meanwhile, the broader market slid about 1.6%, likely weighing on the stock. Investors are up over three years, booking 0.7% per year, much better than the more recent returns. Sometimes when a good quality long term winner has a weak period, it's turns out to be an opportunity, but you really need to be sure that the quality is there. Importantly, we haven't analysed Colour Life Services Group's dividend history. This free visual report on its dividends is a must-read if you're thinking of buying.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on HK exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.