Yahoo Finance

Yahoo Finance Consumer Loans Industry Outlook: Growth Prospects Look Bright

The second quarter earnings season is in full swing and big names in the consumer loans industry have already come out with their results. The companies have reported impressive revenue and earnings growth along with manageable credit costs and solid loan growth.

Improving consumer confidence, lower unemployment rate and higher disposable income should drive the performance of consumer loan stocks. Near-term prospects look bright as a steadily improving domestic economy and robust economic data will continue increasing demand for student, auto and card loans. These factors should slightly increase the demand for mortgage loans too.

However, a rising rate environment, which supports net interest income growth for consumer loan providers, will likely somewhat lower the demand. That’s because, consumers will try to avoid taking loans at higher rates.

Nevertheless, easing credit standards that many of the consumer loan providers are implementing and higher disposable income should keep motivating borrowers. Also, with the change in credit rating process (implemented in July 2017), many consumers, who did not have the required credit score, are now able to gain access to credit card and auto loans due to higher FICO scores.

Also, digitization of operations, efforts to diversify revenue sources, restructuring efforts and strong asset quality (despite easing credit standards) will likely support profitability.

As such, the near-term prospects for the stocks in this industry look bright.

Industry Lags on Shareholder Returns

Looking at shareholder returns over the past two years, it appears that the border economic recovery wasn’t enough for enhancing investors’ confidence in the industry’s growth prospects. But policy changes and economic growth are encouraging enough for investors to bet on this space.

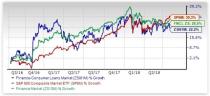

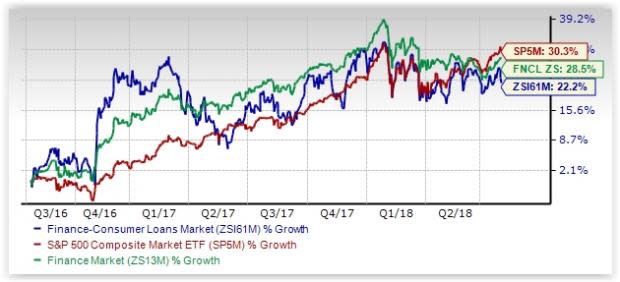

The Zacks Consumer Loans Industry, which is a part of the broader Zacks Finance Sector, has underperformed both the S&P 500 and its own sector over the past two years.

While the stocks in this industry have collectively gained 22.2%, the Zacks S&P 500 Composite and Zacks Finance Sector have rallied 30.3% and 28.5%, respectively.

Two-Year Price Performance

Consumer Loan Stocks Look Inexpensive

Thanks to the underperformance of the industry over the past two years, the inudstry's valuation picture looks reasonable. One might get a good sense of the industry’s relative valuation by looking at its price-to-tangible book ratio (P/TBV), which is the most appropriate multiple for valuing consumer loan providers because of large variations in their earnings results from one quarter to the next.

This ratio essentially measures a company’s current market value relative to what it would be worth if all assets were sold, debt was paid and intangible assets were written off.

The industry currently has a trailing 12-month P/TBV ratio of 1.38X, which is slightly above the one-year median level of 1.31X, over the past two years. When compared with the highest level of 1.47X over the past year, it is obvious that the group's valuation level was higher earlier.

The industry has traded at a discount to the broader market and that's the case at present as well, as the chart below shows.

Price-to-Tangible Book Ratio (TTM)

As finance stocks typically have a lower P/TBV ratio, comparing consumer loan stocks with the S&P 500 may not make sense to many investors. But a comparison of the group’s P/TBV ratio with that of its broader sector also ensures that the group is trading at a decent discount. The Zacks Finance Sector’s trailing 12-month P/TBV ratio of 2.87X and the one-year median level of 3.48X for the same period are above the Zacks Consumer Loan Industry’s respective ratios.

Price-to-Tangible Book Ratio (TTM)

Prospects Look Bright on Improving Earnings Outlook

Expectations of improving profitability with rising interest rates, a decent demand for loans and other strategic initiatives should help consumer loan stocks generate positive shareholder returns in the near future.

But what really matters to investors is whether this group has the potential to outperform the broader market in the quarters ahead. Investors may consider the current price levels as good entry points, as there are convincing reasons to predict a decent upside in the near term.

One reliable measure that can help investors understand the industry’s prospects for a solid price performance going forward is the industry's earnings outlook. Empirical research shows that earnings outlook for the industry, which is a reflection of the earnings revisions trend for the constituent companies, has a direct bearing on its stock market performance.

The Price & Consensus chart for the industry shows the market's evolving bottom-up earnings expectations for the industry and its aggregate stock market performance. The red line in the chart represents the Zacks measure of consensus earnings expectations for 2019, while the light blue line represents the same for 2018.

Price and Consensus: Zacks Consumer Loan Industry

This becomes even clearer by focusing on the aggregate bottom-up EPS revisions trend. The chart below shows the evolution of aggregate consensus expectations for 2018.

Please note that the $4.36 'EPS' estimate for the industry for 2018 is not the actual bottom-up dollar EPS estimate for every company in the Zacks Consumer Loan industry, but rather an illustrative aggregate number created by our proprietary analytics model. The key factor to keep in mind is not the dollar earnings of $4.36 per share for 2018, but how this dollar number has evolved recently.

Current Year EPS Estimate Revisions

As you can see here, the $4.36 EPS estimate for 2018 is up from $3.95 at the end of April and $3.86 at the end of the month prior to that and $3.84 this time last year. In other words, the sell-side analysts covering the companies in the Zacks Consumer Loan industry have been steadily raising their estimates.

Zacks Industry Rank Indicates Solid Prospects

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates continued outperformance in the near term.

The Zacks Major Regional Banks industry currently carries a Zacks Industry Rank #46, which places it at the top 18% of more than 250 Zacks industries. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

Our proprietary Heat Map shows that the industry’s rank has remained in the top half of the rank list over the past eight weeks.

Long-Term Growth Prospects Don’t Look Impressive

While the near-term prospects look bright, long-term (3-5 years) EPS growth estimates for the Zacks Consumer Loan industry don’t seem that impressive. The group’s mean estimate of long-term EPS growth rate has increased since the beginning of 2018 and has remained stable for quite some time at current level of 11.18%. This compares to 9.8% for the Zacks S&P 500 Composite.

Mean Estimate of Long-Term EPS Growth Rate

Since the beginning of 2016, revenues have been improving. Though revenues declined marginally in 2017, the current level compared much favorably with the same in 2015. This is mainly driven by rising interest rates and economic improvement. The adverse impact of higher interest rates on the bottom-line numbers is expected to gradually reduce.

Revenue

Bottom Line

Consumer loan stocks will likely continue benefiting from higher interest rates, favorable operating environment and improving economy in the near term. So, investing in this space could be rewarding.

One should particularly consider betting on the consumer loan stocks that depict an improving earnings outlook.

4 Consumer Loan Stocks to Bet on

Santander Consumer USA Holdings Inc. (SC): The stock of this Dallas, TX -based company has surged 51.4% over the past year. The Zacks Consensus Estimate for the current-year EPS has been revised 12.3% upward over the last 60 days. The stock currently sports Zacks Rank #1 (Strong Buy). (You can see the complete list of today’s Zacks #1 Rank stocks here.)

Price and Consensus: SC

Ally Financial Inc. (ALLY): The consensus EPS estimate for this Detroit, MI-based company has moved 1.7% higher for the current year, over the last 60 days. This Zacks Rank #2 (Buy) stock has rallied 20.4% over the past year.

Price and Consensus: ALLY

Capital One Financial Corporation (COF): The stock of McLean, VA -based company has gained 9.7% over the past year. The consensus EPS estimate for the current year has been revised 12% upward over the last 60 days. The stock carries a Zacks Rank 2.

Price and Consensus: COF

OneMain Holdings, Inc. (OMF): The consensus EPS estimate for this Evansville, IN-based company has moved upward marginally for the current year, over the last 60 days. This Zacks Rank #2 (Buy) stock has rallied 26.9% over the past year.

Price and Consensus: OMF

Wall Street’s Next Amazon

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Santander Consumer USA Holdings Inc. (SC) : Free Stock Analysis Report

OneMain Holdings, Inc. (OMF) : Free Stock Analysis Report

Capital One Financial Corporation (COF) : Free Stock Analysis Report

Ally Financial Inc. (ALLY) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research