Yahoo Finance

Yahoo Finance Did Business Growth Power Pacific Edge's (NZSE:PEB) Share Price Gain of 177%?

Pacific Edge Limited (NZSE:PEB) shareholders might be concerned after seeing the share price drop 13% in the last month. Despite this, the stock is a strong performer over the last year, no doubt about that. Like an eagle, the share price soared 177% in that time. So it is important to view the recent reduction in price through that lense. More important, going forward, is how the business itself is going.

View our latest analysis for Pacific Edge

Because Pacific Edge made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. When a company doesn't make profits, we'd generally expect to see good revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

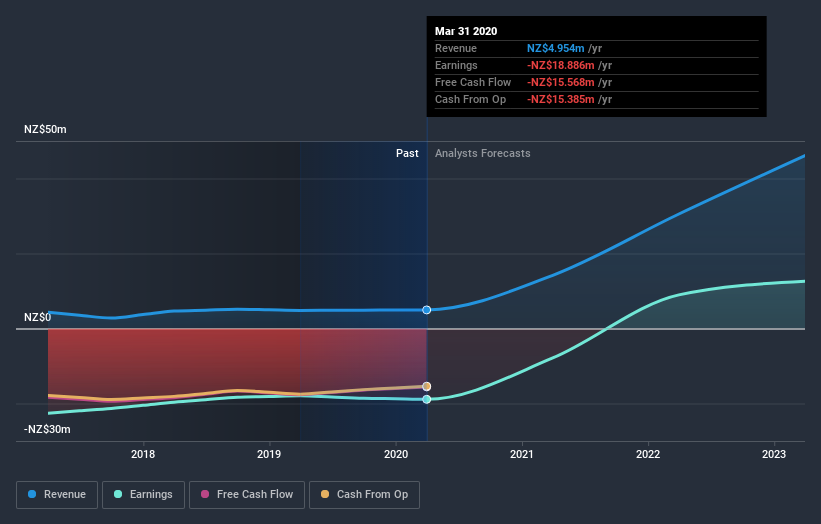

Over the last twelve months, Pacific Edge's revenue grew by 3.0%. That's not a very high growth rate considering it doesn't make profits. So we wouldn't have expected the share price to rise by 177%. The business will need a lot more growth to justify that increase. It's quite likely that the market is considering other factors, not just revenue growth.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

We like that insiders have been buying shares in the last twelve months. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. So it makes a lot of sense to check out what analysts think Pacific Edge will earn in the future (free profit forecasts).

What about the Total Shareholder Return (TSR)?

We've already covered Pacific Edge's share price action, but we should also mention its total shareholder return (TSR). The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Pacific Edge hasn't been paying dividends, but its TSR of 195% exceeds its share price return of 177%, implying it has either spun-off a business, or raised capital at a discount; thereby providing additional value to shareholders.

A Different Perspective

We're pleased to report that Pacific Edge shareholders have received a total shareholder return of 195% over one year. That's better than the annualised return of 8.7% over half a decade, implying that the company is doing better recently. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 4 warning signs for Pacific Edge that you should be aware of before investing here.

Pacific Edge is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on NZ exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.