Yahoo Finance

Yahoo Finance Dover (DOV) Stock Surges 42% in a Year: More Room to Run?

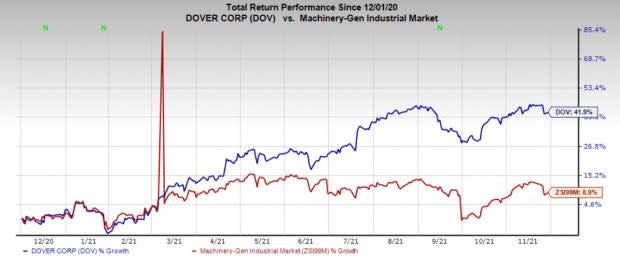

Dover Corporation’s DOV shares have gained 41.9% in the past year compared with the industry’s growth of 8.9%. Solid end-market demand across all segments, strong order trends and forecast-topping earnings over the trailing four quarters have contributed to this share-price appreciation. Benefits from cost-reduction actions, focus on investments and acquisitions as well as efforts to reduce debt levels will stoke growth.

Image Source: Zacks Investment Research

In the last month, Dover reported impressive third-quarter 2021 results, with earnings and sales beating the respective Zacks Consensus Estimates and improved year over year.

Let’s analyze the factors driving the stock.

Driving Factors

Dover has been gaining from robust order trends across the majority of its businesses for a while. It is witnessing solid sales growth in the Engineered Products, Pumps & Process Solutions and Refrigeration & Food Equipment segments. The company expects strong demand growth in compressor components, foodservice and textile printing business in the current year, as these markets continue to recover.

In the Engineered Products segment, demand for engineered products, vehicle service and industrial automation has been solid. Fueling Solutions continues to grow on a robust increase in systems and software, recovering underground demand and vehicle wash. The Imaging & Identification segment will benefit from strong demand for consumables and fast-moving consumer goods solutions. The Marking & coding business is expected to maintain its growth trajectory with services and serialization products. Digital textile printing is recovering from the pandemic-induced declines in the past year.

In the Pumps & Process Solutions business, demand for biopharma connectors and pumps will likely be healthy, aided by vaccine and non-COVID-related pharmaceutical tailwinds. The Refrigeration & Food Equipment, heat exchanger and Belvac business are poised to perform well in the current year, given the large backlog and strong order rates in the food retail business. Dover is investing in increasing capacity and new capabilities in these two businesses to capture growth.

Dover’s productivity and cost-control initiatives will continue to drive bottom-line growth. It executed restructuring programs to align costs and operations with current market conditions. The company is focused on investments in capacity expansions in high-growth businesses and productivity improvements across its portfolio. Dover has a long tradition of making successful acquisitions in diverse end markets. Its efforts to reduce debt levels, solid financial position, prudent capital structure, refinancing efforts and momentum in operational execution bode well.

Dover expects adjusted earnings per share to be between $7.45 and $7.50 for 2021, up from the prior projection of $7.30 and $7.40. The mid-point of the guidance indicates year-over-year growth of 37.8%.

Positive Growth Projection

The company’s earnings estimate for the current year is pegged at $7.52 at present, indicating year-over-year growth of 32.6%.

Zacks Rank & Stocks to Consider

Dover currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the Industrial Products sector are Encore Wire Corporation WIRE, SPX FLOW, Inc. FLOW and Casella Waste Systems, Inc. CWST. All these stocks flaunt a Zacks Rank #1 (Strong Buy), at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Encore Wire has an expected earnings growth rate of around 491% for the current year. The Zacks Consensus Estimate for current-year earnings has been revised 37% upward in the past 60 days.

Encore Wire’s shares have surged 171% in the past year. The company has a trailing four-quarters earnings surprise of 271%, on average.

SPX FLOW has a projected earnings growth rate of around 101.3% for 2021. The Zacks Consensus Estimate for current-year earnings has been revised upward by 5.3% in the past 60 days.

The company’s shares have appreciated 56.9% in a year. SPX FLOW has a trailing four-quarter earnings surprise of 40.4%, on average. FLOW has a long-term earnings growth of 35.2%.

Casella Waste has an estimated earnings growth rate of around 6% for the current year. In the past 60 days, the Zacks Consensus Estimate for current-year earnings has been revised upward by 11.4%.

The company’s shares have increased 44% in the past year. Casella Waste has a trailing four-quarter earnings surprise of 42.1%, on average. CWST has a long-term earnings growth of 14.2%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dover Corporation (DOV) : Free Stock Analysis Report

Casella Waste Systems, Inc. (CWST) : Free Stock Analysis Report

SPX FLOW, Inc. (FLOW) : Free Stock Analysis Report

Encore Wire Corporation (WIRE) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research