Yahoo Finance

Yahoo Finance E-commerce Earnings: Time to Buy These 3 Stocks?

Earnings season is nearing its end, but there are still a few e-commerce companies reporting this week. Ebay EBAY, Etsy ETSY, and Overstock OSTK all report earnings on Wednesday February 22.

These three stocks aren’t exactly giants in the e-commerce space compared to Amazon AMZN, Costco COST, or Walmart WMT, but they are still potentially great stocks. E-commerce is obviously a rapidly growing segment of retail, now making up 22% of total global retail sales, up from 14% in 2019.

While eBay, Etsy, and Overstock are all e-commerce companies, each has its own unique business model. This gives each stock its own strengths and weaknesses. We will cover these differences and earnings expectations below to see if investors want to buy EBAY, ETSY, and OSTK stock before or after their upcoming financial releases.

eBay

eBay is an online marketplace, and auction platform that allows users to list, buy, sell, and pay for items through its web and mobile app.

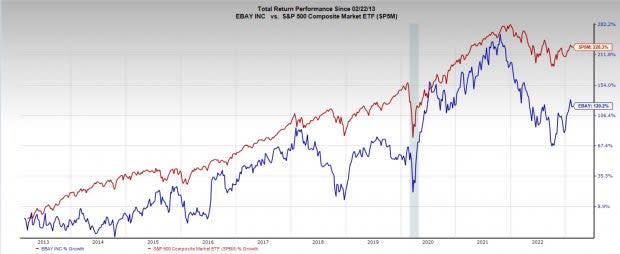

eBay stock experienced explosive growth in its early years but has since slowed to a more regular pace, underperforming the market over the past 10 years.

Additionally, in 2015 EBAY spun off PayPal PYPL. In an extremely unique corporate event, one company became two, and EBAY shareholders became equal shareholders in PYPL. After being pressured by Carl Icahn a year prior, EBAY management eventually went through with the split.

Image Source: Zacks Investment Research

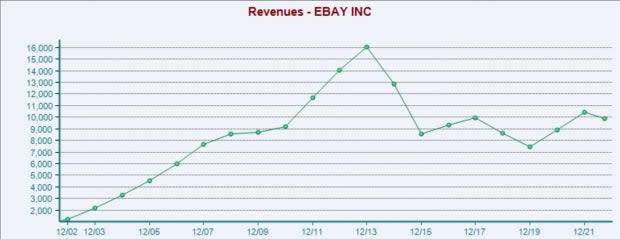

As a platform, eBay doesn’t sell any of its own products, and functions as a marketplace for third-party vendors. Etsy is like eBay in this way. While a strong business model, with 70% gross margins, sales for the online marketplace have stagnated for over a decade. Competition has increased, with new venues like Amazon, and Shopify SHOP as options for vendors.

Image Source: Zacks Investment Research

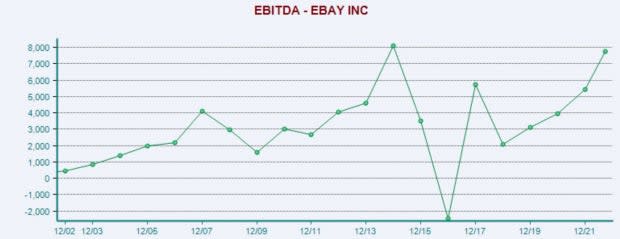

Although sales have been stagnant in recent years EBAY has been improving profitability, and looks like they will soon be making more profits than ever before.

Image Source: Zacks Investment Research

Because of lackluster growth, and declining popularity, EBAY currently sports a reasonable valuation. At 14x one-year forward earnings, EBAY stock is well below its 10-year median of 19x, and considerably below the E-commerce industry average of 35x. I think this makes EBAY a compelling valuation.

Image Source: Zacks Investment Research

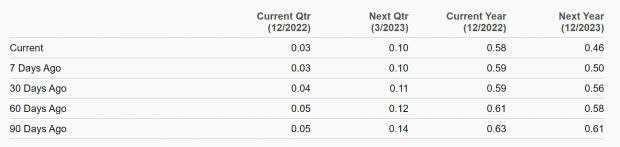

EBAY holds a Zacks Rank #3 (Holds), indicating a flat earnings revision trend. Current quarter sales estimates are projected to shrink -6% YoY to $2.5 billion. Earnings are expected to come in flat YoY at $1.05 per share, which is commendable considering the falling sales.

Etsy

Etsy is a two-sided online marketplace connecting buyers and sellers. ETSY has a ‘craft’ and ‘artisan’ focus to its products, with many sellers producing their products on a smaller scale. Founded in 2006 the company has more recently taken off, connecting 7.5 million active sellers and 96 million buyers, with 120 million items for sale.

ETSY has had extremely volatile returns since its IPO, dancing around the returns of the broad market in massive swings. ETSY sales growth speaks for itself though, as revenue has grown from $200 million to $2.5 billion in just the last 8 years.

Image Source: Zacks Investment Research

Even with the tremendous growth ETSY is experiencing, the valuation is still concerning. Etsy is trading at 46x next year’s earnings, more than double the industry average. From a price to sales perspective, it is quite rich as well. At 6x next year’s revenue, it is well above the industry average of 4x.

Image Source: Zacks Investment Research

ETSY has a Zacks Rank #3 (Hold), indicating flat earnings revisions trend. Current quarter estimates expect sales of $754 million, a 5.1% increase YoY. Earnings are expected to take a hit though, projecting a -26% decrease to $0.82 per share.

It is worth noting that during the previous earnings report ETSY surprised massively to the upside, posting earnings 57% above expectations. Zacks Earnings ESP is expecting another upside surprise of 7%.

Overstock

Overstock has a different business model than ETSY and EBAY, as it is the primary retailer on its e-commerce website. OSTK primarily sells home goods.

Because it is a retailer, rather than a platform, that means margins are significantly lower. Gross margins of ~23% for OSTK are considerably lower than EBAY and ETSY, which hover around 70%. Nonetheless, Overstock has consistently grown its revenues over the last 20 years from $250 million to $2.1 billion today. OSTK did take a -23% cut to its revenues between 2021 and 2022, returning growth back to pre-covid levels.

Image Source: Zacks Investment Research

OSTK holds a Zacks Rank #4 (Sell), indicating downward trending earnings revisions. Analysts are in a near unanimous decision in lowering OSTK earnings expectations across all timeframes.

Current quarter sales are expected to drop -24% YoY to $467 million, while earnings are projected to collapse -92% to $0.03 per share. During the last earnings report OSTK surprised to the upside by 8%, but based on Zacks Earnings ESP, this quarter is expected to see a -320% miss on earnings.

Image Source: Zacks Investment Research

OSTK is currently trading at 45x next year’s earnings, 50% higher than its two-year median of 30x, and well above the industry average of 33x. Considering OSTK’s relatively slower long-term growth, and extremely unstable near-term sales, this valuation seems rich.

Image Source: Zacks Investment Research

Bottom Line

E-commerce is a tremendous secular industry. This means that even though some of the largest companies in the world are leading the way, there is still room for some smaller e-commerce platforms and players to thrive. While valuations are all over the place ETSY, EBAY, and OSTK all have continued to grow sales in the face of intense competition.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

eBay Inc. (EBAY) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

Overstock.com, Inc. (OSTK) : Free Stock Analysis Report

Etsy, Inc. (ETSY) : Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL) : Free Stock Analysis Report