Yahoo Finance

Yahoo Finance First Solar Lays Out Growth Plans Through 2020

First Solar (NASDAQ: FSLR) had its analyst day on Tuesday, and revealed its next-generation solar panel and guidance for 2018. Unlike years past, when the company has announced shifts in strategy or production plans at events like this, this time, the future course looks dialed in.

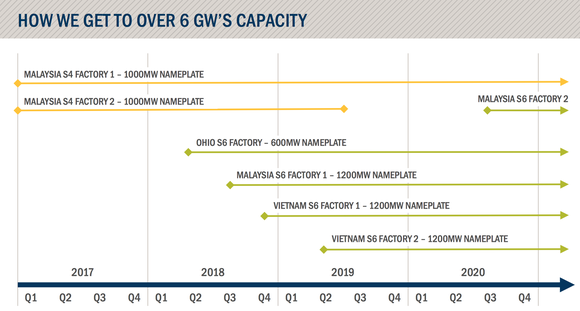

The one surprise was an expansion in Vietnam that will bring production capacity to 5.4 GW by the end of 2020. Here's a look at the big takeaways from the day.

Image source: First Solar.

Series 6 is here

First Solar debuted the first Series 6 solar panel, which was made at the Perrysburg, Ohio, manufacturing plant. The expected power rating is 420 to 445 watts, which gives the 2 meter by 1.2 meter solar panel at least a 17% efficiency rating.

The biggest change is the form factor -- the Series 6 is more than three times the size of the Series 4 panel being made today. This will lead to lower installation costs, and may make manufacturing easier as well.

I will point out that the announced efficiency for this first Series 6 -- which, like prior First Solar panels, use thin-film cadmium telluride technology -- isn't very impressive given that commodity versions of conventional silicon solar panels are already exceeding 17%. But we can also expect First Solar to steadily improve on that number, so investors should expect the company's products to be competitive long term.

First Solar is in growth mode

Planned capacity at the end of 2019 was expected to be around 4.0 GW, but First Solar's management has been hinting for months that they were working on bigger manufacturing expansions. The new forecast -- which includes significant production from sites in Vietnam -- puts capacity at 5.4 GW by the end of 2020, including about 1 GW of Series 4 panel manufacturing that will remain in operation, as you can see below.

Image source: First Solar.

A more focused company

First Solar has cut most of the non-module development out of its business model in the last few years. It's reducing system development to about 1 GW per year, and intends to sell most of those systems earlier in the development process; previously, it waited until a site was in commercial operation to make a sale.

It's also reducing development of trackers and other components down the value chain. This strategy differs from that of SunPower (NASDAQ: SPWR), which is vertically integrating inverters, racking, and system design into solar panel sales, even for the utility-scale market.

2018's guidance

One of the big takeaways from analyst day was First Solar's guidance for 2018. Revenue is expected to be in the $2.3 billion to $2.5 billion range, with gross margins of 22% to 23%. Operating cash flow is expected to be $100 million to $200 million, and after $650 million to $750 million in capital expenses, the company's net cash balance will fall to $1.6 billion to $1.8 billion.

It's notable that management said the result of the ongoing solar trade case, which could lead to President Trump adding tariffs to conventional solar panel imports, won't have much impact on First Solar in 2018, even though its thin-film panels would be exempt. Most of the year's production is already booked, and there will be little opportunity for it to take advantage of potential windfall pricing.

What it all means for investors

First Solar is executing on a strategy it laid out more than a year ago, which it hopes will drive profitability over the next half-decade. So far, its Series 6 panels are living up to expectations, and the capacity expansions being built will give the company greater scale.

The biggest risk First Solar faces comes from competing solar technology. Silicon-based solar panels are getting cheaper and more efficient, which could eat away at First Solar's advantages in the market. The technology side is what investors will want to watch to see if First Solar's strategy will succeed long-term.

More From The Motley Fool

6 Years Later, 6 Charts That Show How Far Apple, Inc. Has Come Since Steve Jobs' Passing

Why You're Smart to Buy Shopify Inc. (US) -- Despite Citron's Report

Travis Hoium owns shares of First Solar and SunPower. The Motley Fool recommends First Solar. The Motley Fool has a disclosure policy.