Yahoo Finance

Yahoo Finance Forget Penny Stocks: Your Money Is Better Off in These 3 Companies

Though penny stocks have the potential to skyrocket out of nowhere, they are often dangerous investments -- which is why they're valued in penny stock territory (usually $200 million or less in market cap, or under $5 per share). Institutional investors usually avoid penny stocks for their high risks, which is a clue that the retail investor probably should, too.

Rather than rolling the dice on a penny stock and hoping for the best, our Foolish investors believe your money would be better off in these three companies: robotic-assisted surgical system developer Intuitive Surgical (NASDAQ: ISRG), genome-editing drug developer Editas Medicine (NASDAQ: EDIT), and online travel booking behemoth Priceline Group (NASDAQ: PCLN).

Image source: Getty Images.

Arguably the best business model in healthcare

Sean Williams (Intuitive Surgical): Though the returns of penny stocks might seem alluring at times, they can be inherently risky. Rather than risking a dart throw, might I suggest you consider robotic-assisted surgical system developer Intuitive Surgical?

While the company's $400-plus share price might appear to be a hindrance to the average investor, it shouldn't, because this company is primed to get stronger as time passes.

Intuitive Surgical has three channels that generate revenue for the company. The first is the sale of its robotic-assisted surgical systems (da Vinci Surgical Systems), which tend to range between $0.5 million and $2.5 million. However, these are intricate systems, and their high cost to build often means the machines themselves are a low-margin product.

The other two revenue channels include the instruments associated with each surgical procedure, and services related to system maintenance. These latter two are high-margin sources of revenue, and their prominence as a percentage of the company's total sales will only grow over time as more da Vinci Surgical systems are installed. In other words, this is a fancy way of saying that Intuitive Surgical's margins are only going to improve over time, despite the entrance of competitors.

Speaking of competitors, Intuitive Surgical also has what might be an insurmountable lead over its peers in terms of installed systems. Since inception, the company has installed 4,149 machines, as of June 30, 2017. Comparatively, all of its peers combined hardly register as a blip next to this figure. It takes a long time to build rapport within the medical community, and the impetus to switch to a new robotic-assisted system simply isn't there for hospitals given the amount of money and time that goes into training surgeons to use these systems. In short, Intuitive has hooked its customers for a long time.

With the company dominating in gynecology and urology procedures, and angling to push into general thoracic and colorectal surgeries, a high single-digit or low double-digit growth rate should remain the norm. That's safety that penny stocks simply can't buy.

Image source: Getty Images.

A risky biotech -- but the rewards could be huge

Keith Speights (Editas Medicine): I shy away from penny stocks, because they're just too risky. However, I'm not afraid to take on some risk when I think the potential rewards could be worth it. And in the case of Editas Medicine, I think the risk-reward proposition looks pretty good.

Let's first talk about the risks. Editas doesn't even have a product in clinical testing yet. As a result, the company is losing lots of money and will likely do so for several years to come. Editas focuses primarily on a gene-editing technique called CRISPR-Cas9, which hasn't been tested in humans yet by any company and could run into problems along the way. There's no guarantee that Editas will ever successfully launch a product.

Now that I've scared you, let's talk about the biotech's potential. CRISPR-Cas9 really could change healthcare as we know it. The approach offers a way to quickly and easily edit genes that cause diseases. While there are several biotechs working on gene-editing therapies using CRISPR-Cas9, Editas has a key advantage: It holds the patents to use the approach in humans. What's more, a court has upheld its rights to those patents already.

Currently, Editas Medicine's market cap stands at around $1.4 billion. That's an enormous level for a company with no revenue to speak of. However, one success with CRISPR-Cas9 in treating a genetic disease could give Editas a market cap several times higher. It's risky, but it's also a risk that I personally feel comfortable taking.

Image source: Getty Images.

Worth every penny

Brian Feroldi (Priceline Group): I know all too well just how alluring penny stocks can be. I invested in them heavily almost exclusively when I first got started. My logic was that I could control hundreds of shares with just a small amount of money, which I thought was obviously better than buying just a few shares of "high-priced" stock.

Of course, I learned the hard way that penny stocks are priced low for a reason. All too often the companies behind the stock are pure garbage. I lost so much money early on that I was quickly cured of my myopic focus on price.

That's why I like to suggest that price-focused investors cure themselves once and for all by buying a stock that trades for well over $100 per share. My favorite business that fits this mold at the moment is Priceline Group.

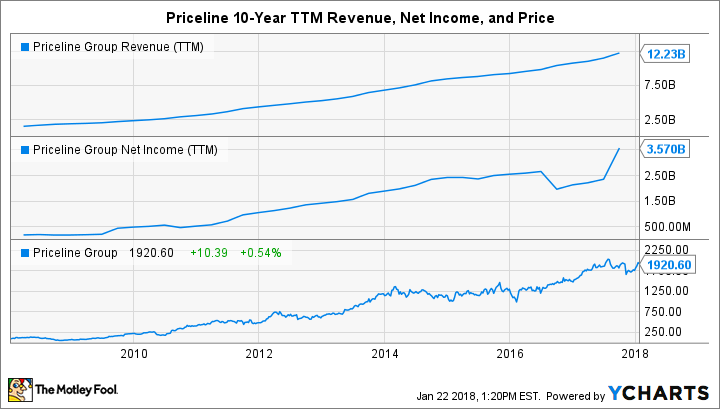

Priceline owns a range of high-quality travel portals that you may have used to book your last vacation. Websites like Kayak.com, Cheapflights.com, Rentalcars.com, Booking.com, and more all fall under Priceline Group's umbrella. This is a wonderful business because the company gets paid each time a user books a car, flight, or hotel through one of its sites. With more consumers using the internet to book their vacations each year, Priceline Group's revenue, net income, and stock price have soared over the last decade.

PCLN revenue (TTM) data by YCharts.

Despite its tremendous history, Wall Street still believes that this company will be able to crank out earnings growth of more than 15% annually over the next five years. That's quite fast for one that's currently trading around 23 times this year's earnings estimates.

Don't let the high share price scare you away. The numbers clearly suggest that Priceline Group is a fabulous business that's trading at a reasonable price. Take advantage of it by buying a few shares today.

More From The Motley Fool

Brian Feroldi owns shares of Intuitive Surgical and Priceline Group. Keith Speights owns shares of Editas Medicine. Sean Williams has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Intuitive Surgical and Priceline Group. The Motley Fool recommends Editas Medicine. The Motley Fool has a disclosure policy.