Yahoo Finance

Yahoo Finance General Mills (GIS) Q4 Earnings Top Estimates, Dividend Raised

General Mills, Inc. GIS posted robust fourth-quarter fiscal 2022 results, wherein the top and bottom lines increased year over year and beat the Zacks Consensus Estimate. The company continued to benefit from its Accelerate strategy, as part of which it remains focused on its core business and portfolio-reshaping actions. Management announced or concluded seven transactions, including buyouts and divestitures, in fiscal 2022, aimed at driving growth in the long run.

While the company’s margins are battling considerable inflation and supply-chain hurdles, it is on track to counter these headwinds through saving and pricing actions.

GIS is progressing well with the Accelerate strategy, which aims to drive sustainable, profitable growth and robust shareholder returns. General Mills is on track with prioritizing core markets, global platforms and local brands along with reshaping its portfolio via strategic acquisitions and divestitures.

Quarterly Highlights

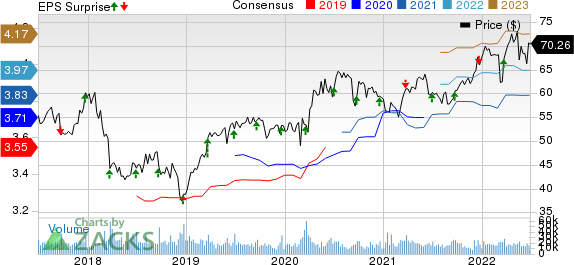

Adjusted earnings per share (EPS) of $1.12 rose 23% year over year on a constant-currency (cc) basis. The upside can be mainly attributed to the elevated adjusted operating profit and reduced average diluted shares outstanding. The bottom line surpassed the Zacks Consensus Estimate of $1.01 per share.

General Mills, Inc. Price, Consensus and EPS Surprise

General Mills, Inc. price-consensus-eps-surprise-chart | General Mills, Inc. Quote

Net sales of $4,891.2 million advanced 8% from the year-ago quarter’s figure. The metric included a 4-point net unfavorable impact of divestitures and acquisition activity and a 1-point adverse impact of currency movements. Organic net sales rose 13% due to the favorable organic net price realization and mix to the tune of 14 points as part of the company’s Strategic Revenue Management (“SRM”) actions undertaken to counter input cost woes. This was somewhat offset by a 2-point negative impact of the reduced organic pound volume. The top line surpassed the Zacks Consensus Estimate of $4,802 million.

The adjusted gross margin contracted 70 basis points (bps) to 33.8% due to a double-digit rise in input cost inflation, escalated other costs of goods sold and supply-chain woes. These were somewhat offset by the positive net price realization and mix as well as cost savings from Holistic Margin Management (“HMM”).

The adjusted operating profit margin expanded 200 bps to 18.3%.

Image Source: Zacks Investment Research

Segmental Performance

General Mills reported results in the following operating segments –

North America Retail: Revenues in the segment came in at $3,004.9 million, up 11% year over year. The uptick can be attributed to the positive net price realization and mix, which somewhat offset the reduced pound volume. Organic net sales grew 11% year over year. The segment’s operating profit increased 18% to $764 million.

International: Revenues in the segment came in at $749.7 million, down 21% year over year. Revenues reflected a 25-point adverse impact of the divestitures of the European yogurt and dough businesses as well as 2 points of unfavorable foreign currency translation. Organic net sales inched up 6% year over year. The segment’s operating profit surged 36% to $76 million.

Pet: Revenues came in at $610.3 million, up 37% year over year due to solid pound volume growth, and positive net price realization and mix. Net sales included 15 points of gains from the pet treats business buyout (concluded on Jul 6, 2021). Organic sales increased 22% year over year. The segment’s operating profit increased 10% to $113 million.

North America Foodservice: Revenues came in at $526.3 million, up 25% year over year due to the positive net price realization and mix, somewhat negated by the reduced pound volume. Organic sales rose 25% as well. The segment’s operating profit jumped 23% to $81 million.

Other Financial Aspects

General Mills ended the quarter with cash and cash equivalents of $569.4 million, long-term debt of $9,134.8 million and total shareholders’ equity of $10,788 million. GIS generated $3,316.1 million in net cash from operating activities in fiscal 2022. Capital investments amounted to $569 million.

The company paid out dividends worth $1.2 million and bought roughly 14 million shares for $877 million in fiscal 2022. Concurrently, management unveiled a dividend hike of 6%, taking it to 54 cents per share, which is payable on Aug 1, 2022 to shareholders of record as of Jul 8.

Other Developments

Cc sales from the joint ventures of Cereal Partners Worldwide remained flat year over year in the quarter. In Haagen-Dazs Japan, sales rose 6% at cc from the prior-year figure.

Fiscal 2023 Guidance

Management issued its guidance for fiscal 2023. The biggest factors impacting its show in the fiscal are likely to be consumers’ economic status, cost inflation and supply-chain bottlenecks. Management anticipates a double-digit rise in the cost of goods sold in the fiscal, to counter which it is on track with its HMM cost saving efforts and pricing initiatives as part of its SRM capacity. Volume elasticities are expected to rise but stay lower than historic levels, while supply-chain woes are likely to moderate in fiscal 2023.

Management has undertaken several portfolio-reshaping actions over the past year, which are anticipated to boost the top and bottom lines in the long run. However, the net effect of these actions is expected to lower adjusted operating profit growth and adjusted EPS growth by nearly 3% each in fiscal 2023. Net proceeds from divestitures are, however, likely to help General Mills support an accelerated share buyback plan in fiscal 2023, which, in turn, is likely to lead to a 2-3% decline in the average diluted share count.

For fiscal 2023, organic net sales are anticipated to grow roughly 4-5%. The net effect of divestitures, buyouts and currency movements is anticipated to lower the full-year net sales growth by roughly 3%.

The adjusted operating profit growth at cc is anticipated between a 2% decline and an increase of 1%. This includes a 3-point net adverse impact of divestitures and buyouts concluded in fiscal 2022.

Adjusted EPS growth at cc is envisioned to be flat to up 3%. This includes a 3-point net adverse impact of divestitures and buyouts concluded in fiscal 2022. Currency woes are likely to have a nearly 1% adverse impact on the adjusted operating profit and adjusted EPS.

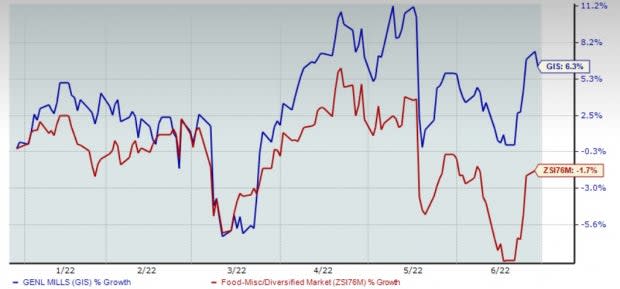

Shares of this Zacks Rank #3 (Hold) company have rallied 6.3% in the past six months against the industry’s 1.7% decline.

3 Solid Staple Stocks

Some better-ranked stocks are Sysco Corporation SYY, Pilgrim’s Pride PPC and Campbell Soup CPB.

Sysco, which engages in marketing and distributing various food and related products, sports a Zacks Rank #1 (Strong Buy). Sysco has a trailing four-quarter earnings surprise of 9.1%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for SYY’s current financial-year sales and EPS suggests growth of 32.6% and 124.3%, respectively, from the year-ago reported number.

Pilgrim’s Pride, which produces, processes, markets and distributes fresh, frozen and value-added chicken and pork products, carries a Zacks Rank #2 (Buy). Pilgrim’s Pride has a trailing four-quarter earnings surprise of 31.4%, on average.

The Zacks Consensus Estimate for PPC’s current financial-year EPS suggests growth of almost 43% from the year-ago reported number.

Campbell Soup, which manufactures and markets food and beverage products, currently carries a Zacks Rank #2. Campbell Soup has a trailing four-quarter earnings surprise of 10.8%, on average.

The Zacks Consensus Estimate for CPB’s current financial-year sales suggests growth of 0.5% from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

General Mills, Inc. (GIS) : Free Stock Analysis Report

Campbell Soup Company (CPB) : Free Stock Analysis Report

Sysco Corporation (SYY) : Free Stock Analysis Report

Pilgrim's Pride Corporation (PPC) : Free Stock Analysis Report

To read this article on Zacks.com click here.