Yahoo Finance

Yahoo Finance Hate Checking Your Portfolio? Try These 2 Dividend Stocks

Managing a portfolio can be a full-time job if you aren't careful with the stocks you pick, and we don't always have that kind of time or dedication. If you hate checking your portfolio, you'll want to pick large, established, and downright boring companies. Dividend Aristocrat ExxonMobil Corporation (NYSE: XOM) and high-yield Enterprise Products Partners L.P. (NYSE: EPD) are great options if you've got things you'd like to do other than check your portfolio 24/7.

On sale today

The price of oil has started to stabilize above the $50 a barrel level. That's led to rebounds in the stock prices of many integrated oil companies, but not Exxon. This oil giant, with global operations that span the entire oil and natural gas value chain, has seen its shares fall around 8% so far in 2017. And, unlike many peers, its price to tangible book value is still hovering around 10-year lows. Relative to its own history, Exxon looks cheap today -- and gives you a generous 3.7% yield as well.

Slow and steady performers can help you build wealth, and avoid the hassle of constantly monitoring your portfolio. Image source: Getty Images

But there's a lot more to like here than just price. For example, Exxon's diversified portfolio is built to withstand tough times. Even during the worst of the recent oil downturn Exxon continued to post positive earnings while most peers were bleeding red ink. The company also raised its dividend each year, pushing its streak of annual dividend hikes to 35 years. Many peers had to pause their increases, or even cut their dividends.

And Exxon's balance sheet, even after adding billions of dollars in debt to support capital spending and dividends during the downturn, is still among the strongest in the industry. The energy giant has even started to pay down debt at this point: at the end of the third quarter, long-term debt accounted for around 12% of the capital structure, modest by almost any measure.

Company | Yield | Annual Dividend |

ExxonMobil Corporation | 3.7% | 35 |

Enterprise Products Partners L.P. | 6.9% | 20 |

Data source: ExxonMobil and Enterprise Products Partners

The price of Exxon will fluctuate with the price of oil and natural gas, but there's clearly no reason to worry about the company's rock-solid business -- quarterly or annual check-ups are all that's needed here.

Special delivery

The second company here is midstream oil and natural gas giant Enterprise Products Partners and its hefty 6.9% distribution yield. This middleman helps move oil and natural gas from where it's drilled to where it gets processed, and then on to end customers. The interesting thing about the business is that most of Enterprise's top line comes from fees, so the price of energy is less important than the demand.

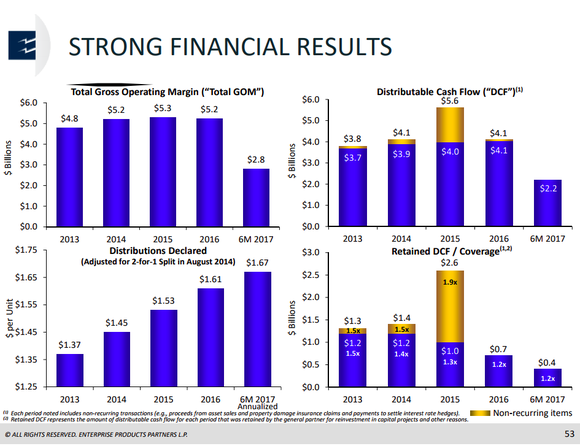

Enterprise, however, is no bit player -- it is one of the largest midstream companies in the United States. Its assets include pipelines, storage, terminals, processing facilities, and a fleet of ships. And unlike some peers that have resorted to cutting their distributions to support growth, Enterprise's streak of annual increases is two decades long. Notably, even during the worst of the energy downturn, the partnership's distribution coverage never dipped below a healthy 1.2 times. Distributable cash flow, meanwhile, rose each year between 2013 and 2016.

A snapshot of Enterprise's solid performance through the energy industry downturn. Image source: Enterprise Products Partners L.P.

Enterprise is planning on slowing its distribution growth over the next few years, but that's so that it will be in a better position to self-fund its growth projects. This move will reduce its cost of capital even further and, longer-term, should lead to more cash flowing through to unitholders in the form of distribution checks. And like Exxon you won't have to watch Enterprise like a hawk -- just a quick check-up every few months or even once a year should be enough.

Tortoises are wonderful

Slow and steady wins the race. Exxon and Enterprise are slow and steady industry leaders that dividend investors should own, or at least have on their watch lists. And the best part is that these tortoises are so boring and stable that you won't have to constantly monitor their businesses. Go have some fun, and let Exxon and Enterprise keep trucking along through good times and bad.

More From The Motley Fool

6 Years Later, 6 Charts That Show How Far Apple, Inc. Has Come Since Steve Jobs' Passing

Why You're Smart to Buy Shopify Inc. (US) -- Despite Citron's Report

Reuben Gregg Brewer owns shares of ExxonMobil. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.