Yahoo Finance

Yahoo Finance Here's Why it is Apt to Buy Ross Stores (ROST) at This Moment

Ross Stores Inc. ROST is an attractive bet for the long term, owing to its strong fundamentals and the off-price retail business model that allows it to deliver value bargains to customers. It has been benefiting from the execution of its store expansion plans over the years. It provided an upbeat view for the fourth quarter and fiscal 2022.

Ross Stores’ top and bottom lines beat the Zacks Consensus Estimate in third-quarter fiscal 2022. This marked the second straight quarter of a bottom-line beat. In third-quarter fiscal 2022, the company’s shoes category remained the key growth driver, with Florida and Texas being the top-performing regions. Results also gained from lower incentive costs and eased domestic freight expenses. Overall, gains at the core business demonstrated consumers' continued focus on value and the company’s ability to deliver value bargains to customers.

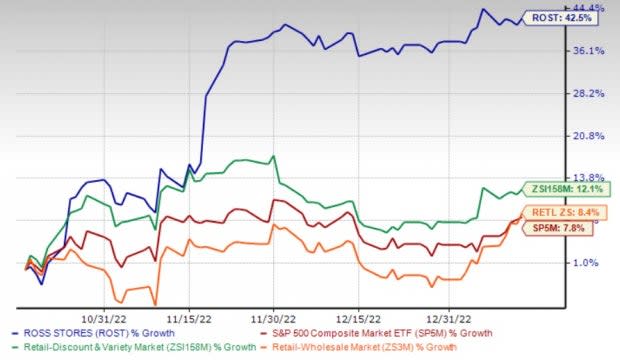

Backed by the robust fiscal third-quarter performance, the stock outperformed the industry and the Retail - Wholesale sector in the past three months. ROST has rallied 42.5% in the past three months compared with the industry and the sector’s growth of 12.1% and 8.4%, respectively. The stock also compares favorably with the S&P 500’s rise of 7.8% in the same period.

The Zacks Consensus Estimate for the Zacks Rank #2 (Buy) company’s fourth-quarter fiscal 2022 sales and earnings suggests growth of 2.2% and 18.3%, respectively, from the year-ago period’s reported numbers.

Image Source: Zacks Investment Research

Factors Driving Growth

Ross Stores is likely to benefit from the improved traffic trends in the retail industry. The company’s third-quarter fiscal 2022 results reflected gains from improved traffic trends from the first half and better inventory position despite year-over-year declines in the top and bottom lines.

As of the end of the fiscal third quarter, consolidated inventories increased 11.8% from the 2021 comparable period, reflecting a significant moderation from the first half of fiscal 2022. Average store inventory increased 4% in the quarter, down from the pre-pandemic levels.

The company also continues to witness SG&A leverage, which is aiding margins. Although Ross Stores was affected by the inflationary cost environment in third-quarter fiscal 2022, lower incentive costs acted as an upside. The decline in incentive costs resulted in lower SG&A expenses in the quarter. Notably, SG&A expenses declined 4.5% year over year. SG&A, as a percentage of sales, contracted 70 bps year over year to 15.2%. Lower incentive costs more than offset the deleveraging effects of declining comps.

Ross Stores has been consistent with the execution of its store expansion plans over the years. The company’s store expansion efforts are focused on continually increasing penetration in the existing, as well as new, markets. In third-quarter fiscal 2022, the company completed its store expansion target for fiscal 2022, with the opening of 28 Ross stores and 12 dd’s DISCOUNTS stores. For fiscal 2022, ROST opened 91 stores, comprising 71 Ross stores and 28 dd’s DISCOUNTS stores. The company earlier anticipated closing 10 older stores in fiscal 2022.

The company expects to end fiscal 2022 with 1,693 Ross stores and 322 dd’s DISCOUNTS stores, marking a net increase of 92 stores. As of Sep 30, 2022, Ross Stores operated 2,019 outlets, including 1,696 Ross stores across 40 states, the District of Columbia and Guam, and 323 dd’s DISCOUNTS stores in 21 states.

Given the large retail closures and bankruptcies over the past several years, Ross Stores earlier raised its long-term store expansion targets. The company expects “Ross Dress for Less” to expand to 2,900 stores compared with the previously mentioned 2,400 stores.

Additionally, it anticipates dd’s DISCOUNTS to expand to 700 stores versus the earlier stated 600 stores. This represents a 20% increase in potential store growth targets, bringing it to 3,600 stores. This indicates significant growth from the company’s store count of 1,923 stores at the end of fiscal 2021.

Given the third-quarter sales momentum and improved assortments for the holiday season, Ross Stores raised its guidance for fourth-quarter fiscal 2022. The company expects comps to be flat to down 2% in the fiscal fourth quarter, whereas it reported 9% comps growth in the prior-year quarter. Earnings per share are envisioned to be $1.13-$1.26 for the fiscal fourth quarter. The company reported earnings of $1.04 per share in the year-ago quarter.

The earnings view for the fiscal fourth quarter is based on sales of flat to up 3% and the operating margin of 9.7% to 10.5%. Notably, the company reported an operating margin of 9.8% in the year-ago quarter. The operating margin view indicates gains due to the easing of significant cost pressures from ocean freight and lower incentives in the prior-year quarter.

For fiscal 2022, the company envisions earnings per share of $4.21-$4.34. Notably, it reported $4.87 in fiscal 2021.

Other Stocks to Consider

Here are three other top-ranked stocks to consider — Build-A-Bear Workshop BBW, Capri Holdings CPRI and Tecnoglass TGLS.

Build-A-Bear, a multi-channel retailer of plush animals and related products, currently sports a Zacks Rank #1 (Strong Buy). Shares of BBW have rallied 67.7% in the past three months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Build-A-Bear’s fiscal 2022 sales and EPS suggests growth of 11.9% and 21.5%, respectively, from the year-ago period’s reported levels. It has a trailing four-quarter surprise of 14.8%, on average.

Capri Holdings, which operates membership warehouses, presently carries a Zacks Rank #2. The company has a trailing four-quarter earnings surprise of 20.99%, on average. Shares of CPRI have risen 48.4% in the past three months.

The Zacks Consensus Estimate for Capri Holdings’ sales and EPS for the current financial year suggests respective growth of 1% and 10.6% from the year-ago period’s reported figures. CPRI has an expected EPS growth rate of 11.8% for three to five years.

Tecnoglass, producer and seller of architectural systems for the commercial and residential construction industries, currently carries a Zacks Rank #2. Shares of TGLS have rallied 56.2% in the past three months.

The Zacks Consensus Estimate for Tecnoglass’ current financial-year revenues and EPS suggests growth of 43.4% and 82.2%, respectively, from the year-ago reported figures. TGLS has a trailing four-quarter negative earnings surprise of 26.9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ross Stores, Inc. (ROST) : Free Stock Analysis Report

BuildABear Workshop, Inc. (BBW) : Free Stock Analysis Report

Tecnoglass Inc. (TGLS) : Free Stock Analysis Report

Capri Holdings Limited (CPRI) : Free Stock Analysis Report