Yahoo Finance

Yahoo Finance Here's Why You Should Retain Surmodics (SRDX) Stock for Now

Surmodics, Inc. SRDX is well poised for growth in the coming quarters, courtesy of its solid prospects in the thrombectomy business over the past few months. The optimism, led by a solid first-quarter fiscal 2023 performance and the company’s consistent efforts to boost research and development (R&D), is expected to contribute further. Yet, concerns related to dependence on third parties and data security threats persist.

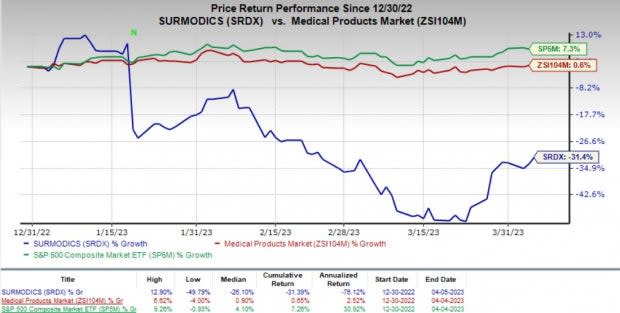

So far this year, this Zacks Rank #3 (Hold) stock has lost 31.4% against the industry’s 0.6% gain. The S&P 500 Composite fell 7.3% in the same time frame.

The renowned medical device and in-vitro diagnostics technology provider has a market capitalization of $320.8 million. Surmodics projects 46.6% growth for fiscal 2024 and expects to maintain its strong performance. Its earnings surpassed estimates in each of the trailing four quarters, the average surprise being 24.4%.

Image Source: Zacks Investment Research

Let’s delve deeper.

Consistent Efforts to Boost R&D: Surmodics’ solid efforts to improve its R&D stature have been a key growth driver, which raises our optimism. The company’s whole product solutions pipeline and sirolimus-based below-the-knee drug-coated balloon program deserve mention. Surmodics has been making progress using its internally developed .014 balloon platform.

In January, the company announced that the differentiated capabilities of its crystalline drug release platform for sirolimus-coated balloons were discussed in connection with the 12-month data from its SWING trial at the International Symposium on Endovascular Therapy.

Bright Thrombectomy Prospects: Surmodics’ plan to leverage its proprietary Pounce thrombectomy platform technology for developing products raises our optimism. On its first-quarter fiscal 2023 earnings call in February, the company confirmed that it had recently begun conducting limited market evaluations to gain experience across a wide variety of cases and clinical conditions, and study the feedback from various physicians. Per management, real-world feedback will help SRDX with future design improvements that’ll benefit physicians as well as patients. It will also optimize the company’s commercial viability.

Strong Q1 Results: Surmodics’ better-than-expected earnings in first-quarter fiscal 2023 buoy optimism about the stock. The company registered robust revenues from its Medical Device segment, product sales, as well as royalties and license fees. In October 2022, Surmodics announced its entry into a new, five-year credit agreement with MidCap Financial. This move is quite encouraging.

Downsides

Reliance on Third Parties: A key element of Surmodics’ business strategy is to enter into licensing arrangements with medical device companies and other organizations that manufacture products using its technologies. Revenues derived from such arrangements depend upon SRDX’s or its licensees’ ability to successfully develop, obtain regulatory approval, market and sell products using its technologies. The company’s or its licensees’ failure to meet these requirements could have an adverse effect on Surmodics’ business.

Data Security Threats: SRDX collects and stores sensitive data, including its proprietary business information, on its networks. Proper maintenance of this data is critical to the company’s operations and business strategy. Despite Surmodics’ security measures, its information technology and infrastructure may be vulnerable to attacks by hackers. This could be due to employee error or other technical disruptions.

Surmodics, Inc. Price

Surmodics, Inc. price | Surmodics, Inc. Quote

Estimate Trend

Surmodics is witnessing a positive estimate revision trend for fiscal 2023. In the past 90 days, the loss per share estimate for the company has narrowed from $2.37 per share to $1.93.

The Zacks Consensus Estimate for the company’s second-quarter fiscal 2023 revenues is pegged at $25.9 million, indicating a 0.4% decline from the year-ago quarter’s tally.

Our estimate for second-quarter 2023 revenues is $26 million, indicating a 0.2% decline from the year-ago period.

Stocks to Consider

Some better-ranked stocks in the broader medical space are Becton, Dickinson and Company BDX, Henry Schein HSIC and The Cooper Companies COO.

Becton, Dickinson and Company, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth of 7.8%. The company’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 6.47%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

So far this year, BDX’s shares have declined 2.4% against the industry’s 5.6% growth.

Henry Schein, sporting a Zacks Rank #1 at present, has an estimated long-term growth of 18.3%. Its earnings surpassed estimates in three of the trailing four quarters and met the same once, the average surprise being 2.97%.

So far this year, the company’s shares have gained 3.3% compared with the industry’s 5.6% growth.

The Cooper Companies, carrying a Zacks Rank #2 at present, has an estimated long-term growth of 11%. COO’s earnings missed estimates in each of the trailing four quarters, the average negative surprise being 1.82%.

So far this year, the company’s shares have gained 11.9% compared with the industry’s 5.6% growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Becton, Dickinson and Company (BDX) : Free Stock Analysis Report

Henry Schein, Inc. (HSIC) : Free Stock Analysis Report

Surmodics, Inc. (SRDX) : Free Stock Analysis Report

The Cooper Companies, Inc. (COO) : Free Stock Analysis Report