Yahoo Finance

Yahoo Finance Intel's Dividends Can Hold Up, But The Business Faces Uncertainty In The Future

First published on Simply Wall St News

Summary:

Intel's production expansion is projected to cost more than $120b, and will be partly supported by the U.S. Chips act.

The next few years are expected to be negative for earnings and cash flows as the company invests in fabs.

Intel can sustain dividend payments for some 4 years, but may have to finance them from debt if the business doesn't recover in the next few years.

Intel Corporation (NASDAQ:INTC) started an accelerated downtrend in August. The company lost 27% of its market value since then, and investors may be concerned about the near future. Looking at analysts forecasts, it seems that there may be some more pain ahead. We break down the fundamentals, future expectations, and see what that means for investors in our analysis.

The Fundamentals

Intel has a solid fundamental history, the company made $19b in net income for the last 12 months, with a profit margin of 26%. Its return on equity of 18.9% is close to the industry's 19.4%, but the returns on capital have declined from 20.2% three years ago to 8.9%. Intel also pays a sizeable 5.5% dividend yield for investors, or $1.46 per share.

Looking at the balance sheet, we can see that the company has a debt balance of $35.4b with a sizeable cash moat of $27b - marking an $8.4b net debt balance. We can see the health of Intel's balance sheet in the chart below:

See our latest analysis for Intel

The Future Business Direction

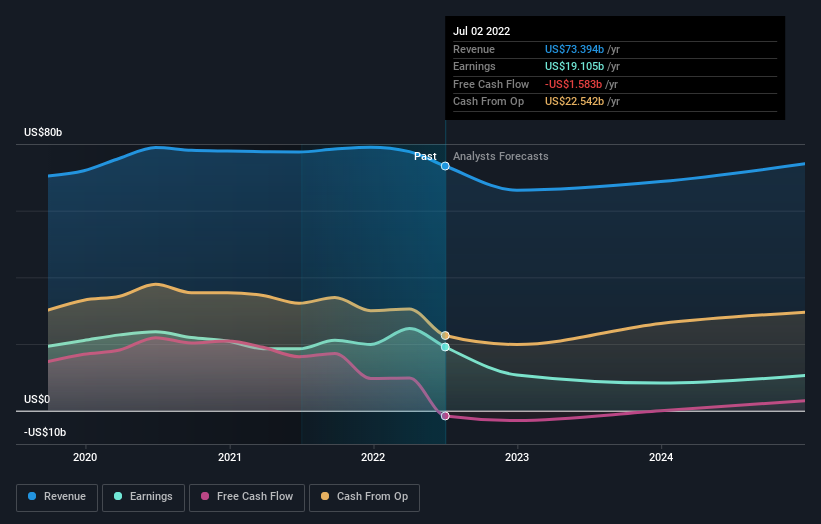

Intel's free cash flows have been slowly declining since 2021, finally ending up negative with a loss of $1.583b. This is somewhat due to the business decline and the fab investments that the company is making in order to allow other semiconductors companies to onshore their production to the U.S. by using Intel's new fabs.

Intel's Fabs are Returning to U.S. Shores

A fab is a semiconductor factory where most or all semiconductor components are produced. Traditionally, U.S. semiconductor companies only design the semiconductors in the states, which are then produced overseas.

After lagging in performance behind Apple (NASDAQ:AAPL), AMD (NASDAQ:AMD) and other semiconductor designers, Intel decided to pursue a manufacturing vertical. This is supported by the CHIPS act, which offers significant benefits to companies building semiconductor production facilities in the states. The act was partly passed as a way to decrease the reliance of the U.S. on external chip manufacturers, and allocates some $52.7b in federal subsidies.

The company is intending to spend more than $120b on expanding production capacities in the U.S. and Europe. This will pressure margins and cash flows, while investors will have to be patient to see if the investments will yield any real returns. Investors that are optimistic on the overall semiconductor future may lean to sticking with Intel as the company becomes a larger player in the field over time.

Analysts Estimate a Decline in Earnings for the Next Few Years

The 32 analysts covering Intel now estimate free cash flows coming up positive in 2024. Revenues and earnings are also expected to struggle, with an estimated $66.14b in 2022 revenues and $10.7b in earnings for the same period. This means that EPS are forecast to drop 44% to $2.60.

See our latest analysis for Intel

Considering that free cash flows are going to be negative for some time, the company may need to reach into its cash balance or raise more debt in order to pay the current dividend. Alternatively, Intel can reduce dividend payments if they think that their investor base would still stick with the company. The total annual dividend payment from Intel currently amounts to about $6b. This represents some 22% of the company's cash balance, which means that Intel can sustain current dividend payments for some 4 years. However, keep in mind that debt is becoming more expensive to refinance, and mature companies like Intel may want to deleverage somewhat, at least until they get their cash flows on a positive level.

What This Means For Investors

It is good that Intel can afford its current dividend for at least 4 more years, however this is not enough, as the company needs to finance the dividend from debt or cash instead of paying it out as a residual from free cash flows.

It seems likely that the company is in for a slump in the next year, but that can be a good or bad thing depending on investors' view on the future of the business. Will Intel find a profitable vertical with the onshoring of production, or will the net margin suffer as the company is reduced to producing cheap components? It seems that the next years will be uncertain for the business, and investors that make the right call now will be able to see higher returns or save themselves from further pain.

However, before you get too enthused, we've discovered 2 warning signs for Intel (1 is potentially serious!) that you should be aware of.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here