Yahoo Finance

Yahoo Finance Investors one-year losses grow to 87% as the stock sheds US$61m this past week

It's not a secret that every investor will make bad investments, from time to time. But serious investors should think long and hard about avoiding extreme losses. So we hope that those who held Velo3D, Inc. (NYSE:VLD) during the last year don't lose the lesson, in addition to the 87% hit to the value of their shares. A loss like this is a stark reminder that portfolio diversification is important. Velo3D may have better days ahead, of course; we've only looked at a one year period. The falls have accelerated recently, with the share price down 85% in the last three months. We really feel for shareholders in this scenario. It's a good reminder of the importance of diversification, and it's worth keeping in mind there's more to life than money, anyway.

After losing 20% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

Check out our latest analysis for Velo3D

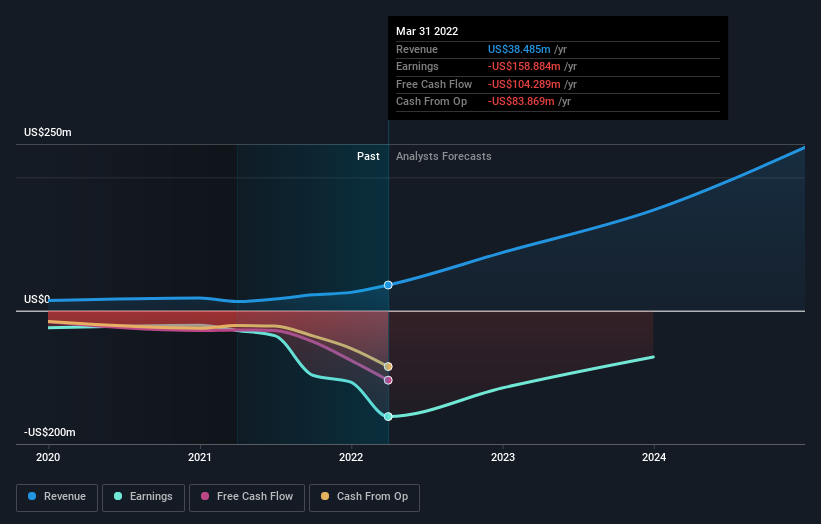

Velo3D isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

In the last twelve months, Velo3D increased its revenue by 180%. That's well above most other pre-profit companies. So the hefty 87% share price crash makes us think the company has somehow offended market participants. There's clearly something unusual going on here such as an acquisition that hasn't delivered expected profits. We'd recommend taking a very close look at the stock (and any available forecasts), before considering a purchase, because the share price is not correlated with the revenue growth, that's for sure. Of course, markets do over-react so share price drop may be too harsh.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

If you are thinking of buying or selling Velo3D stock, you should check out this FREE detailed report on its balance sheet.

A Different Perspective

Velo3D shareholders are down 87% for the year, even worse than the market loss of 20%. That's disappointing, but it's worth keeping in mind that the market-wide selling wouldn't have helped. With the stock down 85% over the last three months, the market doesn't seem to believe that the company has solved all its problems. Given the relatively short history of this stock, we'd remain pretty wary until we see some strong business performance. It's always interesting to track share price performance over the longer term. But to understand Velo3D better, we need to consider many other factors. Take risks, for example - Velo3D has 2 warning signs we think you should be aware of.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.