Yahoo Finance

Yahoo Finance Fed to start 2020 with heavy scrutiny on the meaning of 'liquidity'

Markets do not expect the Federal Reserve to move on interest rates in its first policy-setting meeting of 2020, which could shift attention to the central bank’s efforts to provide liquidity through an expanding balance sheet.

As of Monday afternoon, Fed funds futures traded on the Chicago Mercantile Exchange were pricing in an 87% chance of no change at the conclusion of the Federal Open Market Committee meeting this Wednesday afternoon.

JPMorgan Chase wrote Jan. 24 that the Wednesday meeting “should be one of the least eventful meetings in recent years.”

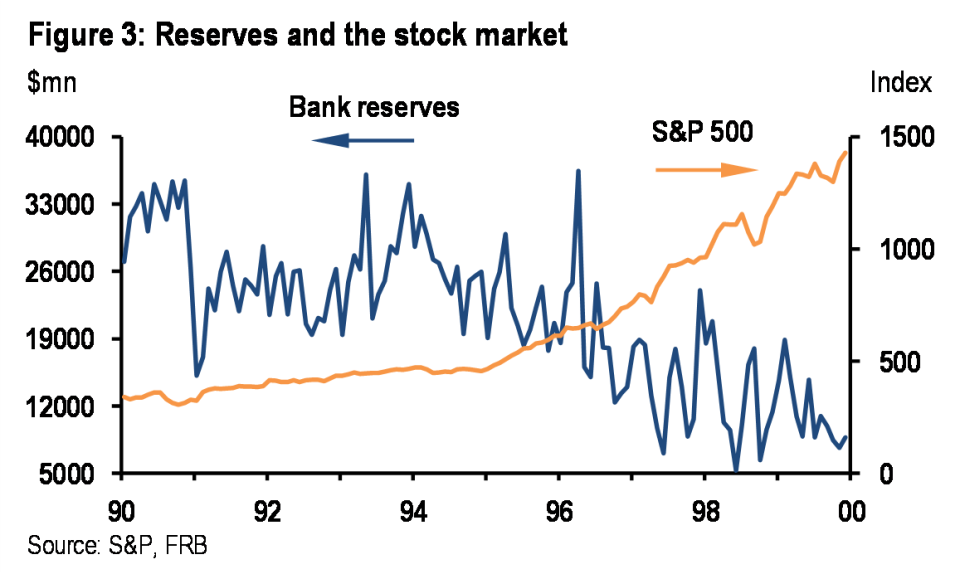

But the balance sheet, which has expanded by almost $400 billion over the last four months, may take center stage in Powell’s press conference as markets debate the impact of liquidity on risk assets.

While Fed Chairman Jerome Powell and other policymakers have reiterated that T-bill purchases and temporary repo operations are merely “technical” adjustments, the market may not be so convinced.

“Clearer communication is needed to allay concerns among investors that an end to building reserves will pull the rug out from under risk assets,” Morgan Stanley’s economics team wrote Jan. 24.

It’s ‘technical’

Between 2017 and last year, the Fed allowed more than $700 billion of assets that it accumulated during quantitative easing to roll off of its balance sheet.

But a flare-up in money markets in August last year sent interest rates spiking beyond the Fed’s target range. The Fed acknowledged that the balance sheet “normalization” process may not have left enough liquidity flowing in the repo market, the plumbing of the financial system where banks and broker-dealers borrow cash.

The Fed committed to T-bill purchases at a $60-billion-a-month pace and the New York Fed opened up short-term repo operations to provide overnight liquidity directly to primary dealers.

As of Jan. 22, the New York Fed was offering about $186 billion in overnight repo operations.

Powell has reiterated that the operations are “technical” and designed to increase bank reserves to keep repo rates — and therefore interest rates at large — in control. And the Fed has said it will continue those purchases “at least” through the second quarter of this year.

“They do not represent a change in the stance of monetary policy,” Powell said Oct. 30. “In particular, our Treasury bill purchases should not be confused with the large-scale asset purchase programs that we deployed after the financial crisis.”

‘Tough to explain’

JPMorgan’s Michael Feroli wrote Jan. 24 that some market participants have the “magical thinking” that supplying more bank reserves corresponds with higher asset prices. Feroli argues that there is no channel by which overnight funding leads to credit creation, meaning that the Fed’s T-bill purchases and repo operations have no accommodative impact.

“[T]he slowing in reserve creation set to occur later this year has no effect on the economic outlook,” Feroli wrote.

But that “magical” thinking may even exist inside the Fed, where FOMC voter and Dallas Fed President Robert Kaplan has said T-bill purchases, repo operations, and low interest rates create a “derivative” of quantitative easing.

“All three of those actions are contributing to elevated risk-asset valuations,” Kaplan told Bloomberg on Jan. 15.

UBS warned that the issue of liquidity is “tough to explain,” adding that markets at risk of reading any stoppage in balance sheet growth as taking the punch bowl away.

“This topic is the key area where a misstatement could easily lead to an adverse market reaction,” UBS wrote Jan. 23.

The Fed will release its policy announcement at 2 p.m. ET on Wednesday, followed by a press conference at 2:30 p.m. ET.

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.

Trump has tweeted about the Fed 100 times since nominating Jerome Powell

Dambisa Moyo: Defunding oil companies is a 'naive' way to address climate change

Central banks see ‘impending arrival’ of their own digital currencies

Guggenheim's Scott Minerd: Fed liquidity could create new bubble

'This is the new normal': California businesses pessimistic on phase 2 deal

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.