Yahoo Finance

Yahoo Finance June Undervalued Stock Picks

Pilgrim’s Pride and Hi-Crush Partners are stocks on my list that are potentially undervalued. This means their current share prices are trading well-below what the companies are actually worth. There’s a few ways you can measure the value of a company – you can forecast how much money it will make in the future and base your valuation off of this, or you can look around at its peers of similar size and industry to roughly estimate what it should be worth. Below, I’ve created a list of companies that compare favourably in all criteria based on their most recent financial data, making them potentially good investments.

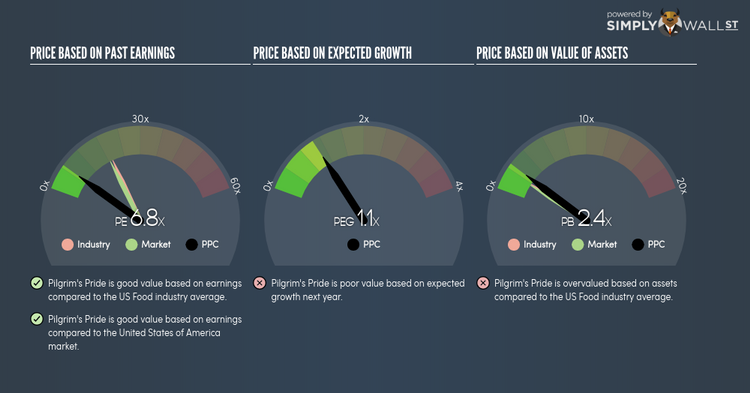

Pilgrim’s Pride Corporation (NASDAQ:PPC)

Pilgrim’s Pride Corporation engages in the production, processing, marketing, and distribution of fresh, frozen, and value-added chicken products in the United States, the United Kingdom, Europe, and Mexico. Started in 1946, and currently headed by CEO William Lovette, the company now has 51,400 employees and with the market cap of USD $4.89B, it falls under the mid-cap stocks category.

PPC’s shares are currently hovering at around -59% under its intrinsic level of $48.07, at a price of US$19.65, according to my discounted cash flow model. This discrepancy gives us a chance to invest in PPC at a discount. Also, PPC’s PE ratio stands at 6.79x relative to its Food peer level of, 19.46x implying that relative to its comparable set of companies, we can buy PPC’s stock at a cheaper price today. PPC is also a financially healthy company, as short-term assets amply cover upcoming and long-term liabilities.

More on Pilgrim’s Pride here.

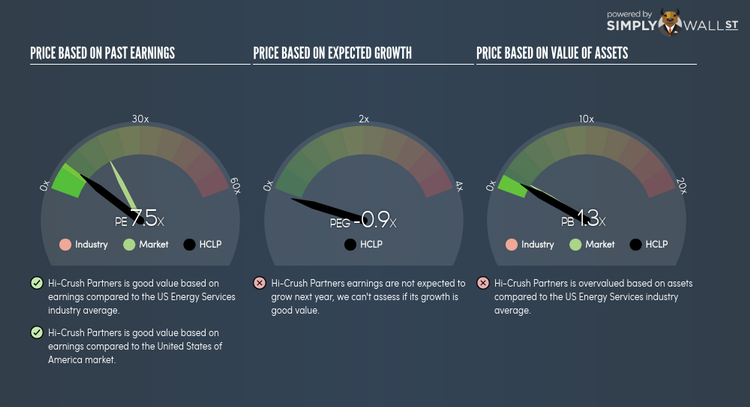

Hi-Crush Partners LP (NYSE:HCLP)

Hi-Crush Partners LP, together with its subsidiaries, provides proppant and logistics solutions to the energy industry in North America. Founded in 2012, and currently lead by Robert Rasmus, the company provides employment to 95 people and with the market cap of USD $1.05B, it falls under the small-cap category.

HCLP’s shares are currently hovering at around -56% less than its true level of $27.02, at a price of US$11.90, based on my discounted cash flow model. This discrepancy signals a potential opportunity to buy HCLP shares at a low price. Moreover, HCLP’s PE ratio stands at 7.55x while its Energy Services peer level trades at, 18.47x implying that relative to its comparable set of companies, you can purchase HCLP’s stock for a lower price right now. HCLP is also a financially healthy company, with near-term assets able to cover upcoming and long-term liabilities. It’s debt-to-equity ratio of 24.18% has been falling over time, signalling HCLP’s capacity to reduce its debt obligations year on year. Interested in Hi-Crush Partners? Find out more here.

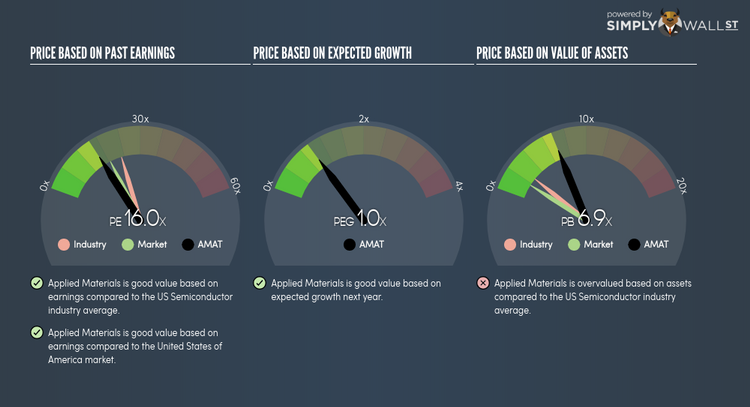

Applied Materials, Inc. (NASDAQ:AMAT)

Applied Materials, Inc. provides manufacturing equipment, services, and software to the semiconductor, display, and related industries worldwide. Started in 1967, and currently headed by CEO Gary Dickerson, the company currently employs 18,400 people and has a market cap of USD $48.35B, putting it in the large-cap group.

AMAT’s stock is now hovering at around -34% below its actual value of $72.3, at a price tag of US$47.96, according to my discounted cash flow model. This discrepancy gives us a chance to invest in AMAT at a discount. Moreover, AMAT’s PE ratio is trading at 15.96x against its its Semiconductor peer level of, 22.71x indicating that relative to other stocks in the industry, we can buy AMAT’s stock at a cheaper price today. AMAT is also in good financial health, as short-term assets amply cover upcoming and long-term liabilities.

Continue research on Applied Materials here.

For more financially sound, undervalued companies to add to your portfolio, explore this interactive list of undervalued stocks.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.