Yahoo Finance

Yahoo Finance What You Should Know About Heartland Bank Limited’s (NZSE:HBL) Liquidity

Heartland Bank Limited’s (NZSE:HBL) profitability and risk are largely affected by the underlying economic growth for the region it operates in NZ given it is a small-cap stock with a market capitalisation of NZ$982.81m. Since banks make money by reinvesting its customers’ deposits in the form of loans, strong economic growth will drive the level of savings deposits and demand for loans, directly impacting the cash flows of those banks. After the Financial Crisis in 2008, a set of reforms called Basel III was created with the purpose of strengthening regulation, risk management and supervision in the banking sector. The Basel III reforms are aimed at banking regulations to improve financial institutions’ ability to absorb shocks caused by economic stress which could expose banks like Heartland Bank to vulnerabilities. Since its financial standing can unexpectedly decline in the case of an adverse macro event such as political instability, it is important to understand how prudent the bank is at managing its risk levels. Sufficient liquidity and low levels of leverage could place the bank in a safe place in case of unexpected macro headwinds. Today we will be measuring Heartland Bank’s financial risk position by looking at three leverage and liquidity metrics.

See our latest analysis for Heartland Bank

Is HBL’s Leverage Level Appropriate?

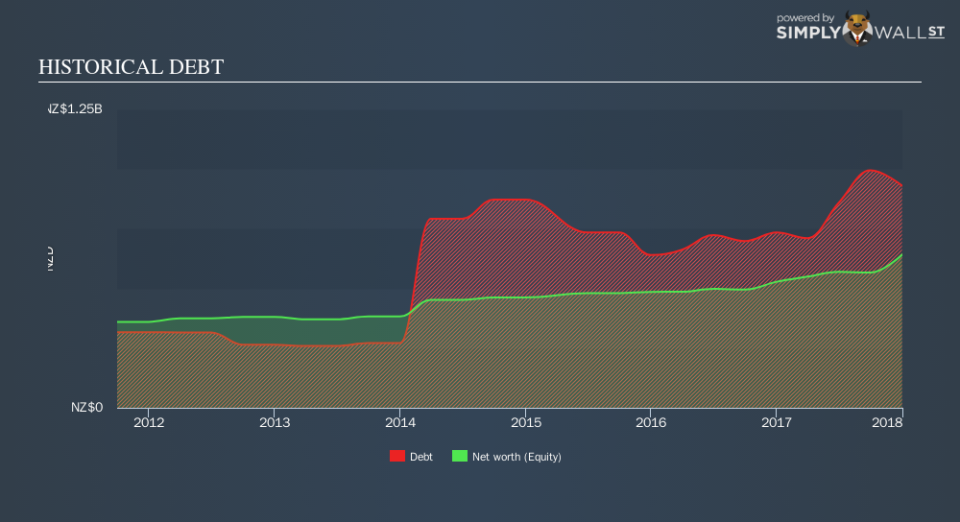

Banks with low leverage are exposed to lower risks around their ability to repay debt. A bank’s leverage can be thought of as the amount of assets it holds compared to its own shareholders’ funds. While financial companies will always have some leverage for a sufficient capital buffer, Heartland Bank’s leverage ratio of less than the suitable maximum level of 20x, at 6.72x, is considered to be very cautious and prudent. This means the bank has a sensibly high level of equity compared to the level of debt it has taken on to maintain operations which places it in a strong position to pay back its debt in unforeseen circumstances. Should the bank need to increase its debt levels to meet capital requirements, it will have abundant headroom to do so.

What Is HBL’s Level of Liquidity?

Due to its illiquid nature, loans are an important asset class we should learn more about. Normally, they should not exceed 70% of total assets, however its current level of 87.83% means the bank has clearly lent out 17.83% above the sensible threshold. This means its revenue is reliant on these specific assets which means the bank is also more exposed to default compared to banks with less loans.

Does HBL Have Liquidity Mismatch?

Banks profit by lending out its customers’ deposits as loans and charge an interest on the principle. These loans may be fixed term and often cannot be readily realized, yet customer deposits on the liability side must be paid on-demand and in short notice. This mismatch between illiquid loans and liquid deposits poses a risk for the bank if unusual events occur and requires it to immediately repay its depositors. Compared to the appropriate industry loan to deposit level of 90%, Heartland Bank’s ratio of over 139.95% is unsustainably higher, which places the bank in a very dangerous position given the high liquidity discrepancy. Basically, for NZ$1 of deposits with the bank, it lends out over NZ$1.20 which is unjustifiable.

Next Steps:

We’ve only touched on operational risks for HBL in this article. But as a stock investment, there are other fundamentals you need to understand. Below, I’ve compiled three essential factors you should further examine:

Future Outlook: What are well-informed industry analysts predicting for HBL’s future growth? Take a look at our free research report of analyst consensus for HBL’s outlook.

Valuation: What is HBL worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether HBL is currently mispriced by the market.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.