Yahoo Finance

Yahoo Finance Lowe's (LOW) Digital Division and Pro Business Augur Well

Lowe's Companies, Inc. LOW is well-positioned to capitalize on the demand for the home improvement market, backed by investments in technology, merchandise category and strength in the Pro business. A strong digital base has been aiding the company’s performance for a while now. LOW’s Total Home strategy, including complete solutions for various home improvement needs, also bodes well.

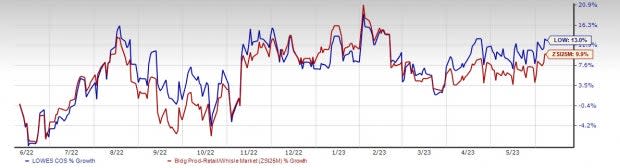

Despite a tough operating backdrop, this renowned home-improvement retailer has gained 13% in the past six months, outperforming the industry’s 9.9% growth. The long-term expected earnings growth rate of 12.6%, coupled with a VGM Score of A, speaks volumes for this current Zacks Rank #3 (Hold) stock.

The Zacks Consensus Estimate for Lowe’s fiscal 2024 sales and earnings per share (EPS) is currently pegged at $89.6 billion and $14.65, respectively. These estimates suggest growth of 1.9% and 9.1%, respectively, from the year-ago fiscal quarter’s corresponding figures, raising analysts’ optimism about the stock.

Detailing Strategies

Management continues making investments in omnichannel capabilities to drive growth. The areas include expanding the online assortment, boosting the user experience and improving fulfillment. The company has also been enhancing the pick up in store experience to streamline processes and advance technology. These enhancements led to faster fulfillment and a 400-basis point rise in pickup in-store customer satisfaction scores in the first quarter of fiscal 2023.

Apparently, online sales accelerated with 6% comparable sales growth, accounting for more than 10% sales penetration. The growth was backed by higher Pro sales stemming from advanced Pro digital experience with the latest tools and personalization. Management is on track with advancing the same-day and next-day fulfillment capabilities. Meanwhile, its focus on perpetual productivity improvement, or the PPI initiative, has also been yielding results.

Image Source: Zacks Investment Research

Pro customers have been a significant driver in Lowe's business. The company has been augmenting pro-focused brands and had earlier refurbished its pro-service business website which is called LowesForPros.com. Management remains pleased with the continued enhancements to its assortment of Pro products from trusted brands. The company is also experiencing higher demand for paint, especially from the Pros business.

Lowe’s has launched Pro online business tools, the latest upgrade to its MVP’s Pro Rewards program. Management is quite focused on enhancing the Pro offering across the company’s stores and online with improved service levels, deeper inventory quantities, intuitive store layout and more Pro national brands. The Pro segment is expected to continue its momentum with improved in-stock inventory levels, enhanced service offerings and the Pro loyalty program.

Lowe’s has also been scaling the its rural framework to as many as 300 additional stores by the year’s end, with a broader offering of farm, ranch and outdoor products. This will position Lowe’s as a one-stop shop for the rural side of the country. The company has enhanced its new store-inventory management system, or SIMS, which focuses on improving inventory visibility and operational efficiency. Lowe’s expects a $250 million benefit to sales from the delayed onset of spring in fiscal 2023.

In a nutshell, Lowe’s is well-poised for growth, given the above-discussed tailwinds.

Three Better-Ranked Retail Stocks

We have highlighted three better-ranked stocks, namely Abercrombie & Fitch ANF, American Eagle Outfitters AEO and Hibbett Sports HIBB.

Abercrombie & Fitch, a leading casual apparel retailer, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Abercrombie & Fitch’s current financial-year sales and EPS suggests growth of 2.1% and 472%, respectively, from the year-ago reported figures. ANF delivered a negative trailing four-quarter earnings surprise of 141.2%, on average.

American Eagle Outfitters, a retailer of casual apparel, accessories and footwear, currently carries a Zacks Rank #2 (Buy). AEO delivered an earnings surprise of 23.3% in the last reported quarter.

The Zacks Consensus Estimate for American Eagle Outfitters’ current financial-year sales and EPS suggests growth of 1.4% and 15.5%, respectively, from the year-ago reported figures.

Hibbett, a sporting goods retailer, currently carries a Zacks Rank of 2. The company has a negative trailing four-quarter earnings surprise of 13.9%, on average.

The consensus estimate for Hibbett’s current financial-year sales suggests growth of 5.7% from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

Lowe's Companies, Inc. (LOW) : Free Stock Analysis Report

Hibbett, Inc. (HIBB) : Free Stock Analysis Report