Yahoo Finance

Yahoo Finance Matthews International (NASDAQ:MATW) Is Increasing Its Dividend To $0.23

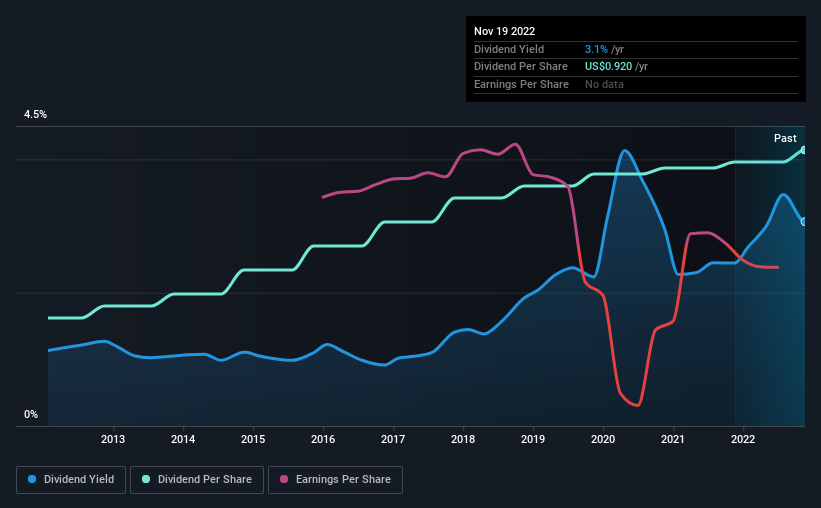

Matthews International Corporation (NASDAQ:MATW) will increase its dividend from last year's comparable payment on the 12th of December to $0.23. This takes the dividend yield to 3.1%, which shareholders will be pleased with.

See our latest analysis for Matthews International

Matthews International Is Paying Out More Than It Is Earning

A big dividend yield for a few years doesn't mean much if it can't be sustained. Matthews International is not generating a profit, but its free cash flows easily cover the dividend, leaving plenty for reinvestment in the business. In general, cash flows are more important than the more traditional measures of profit so we feel pretty comfortable with the dividend at this level.

Over the next year, EPS is forecast to expand by 111.5%. If the dividend continues on its recent course, the company could be paying out several times what it earns in the next 12 months, which could start applying pressure to the balance sheet.

Matthews International Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2012, the dividend has gone from $0.36 total annually to $0.92. This implies that the company grew its distributions at a yearly rate of about 9.8% over that duration. Companies like this can be very valuable over the long term, if the decent rate of growth can be maintained.

The Dividend Has Limited Growth Potential

The company's investors will be pleased to have been receiving dividend income for some time. However, initial appearances might be deceiving. Earnings per share has been sinking by 47% over the last five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The company is generating plenty of cash, but we still think the dividend is a bit high for comfort. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 2 warning signs for Matthews International (of which 1 is a bit concerning!) you should know about. Is Matthews International not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here