Yahoo Finance

Yahoo Finance Omnicell's (OMCL) New Acquisitions Aid Growth, Cost Woes Stay

Omnicell's OMCL strategic acquisitions and partnerships support each of the three pillars of the company’s strategy. Yet, the increasing cost of production continues to hamper the company’s margin performance. Weak hospital spending trends and tough competition also pose threats. The stock carries a Zacks Rank #3 (Hold).

Omnicell ended the first quarter of 2023 with better-than-expected earnings and revenues, driven by strong execution, disciplined cost management and revenue timing. Reported revenues exceeded the high end of Omnicell’s previous revenue outlook in the band of $273-$283 million, which is highly appreciated. The year-over-year increase in Omnicell’s service revenues emphasizes its digital transformation strategy.

The company’s adjusted EPS in the quarter surpassed the top end of the previous guidance in the band of 4-14 cents for the first quarter, led by a capable product and service mix, expense timing and solid execution.

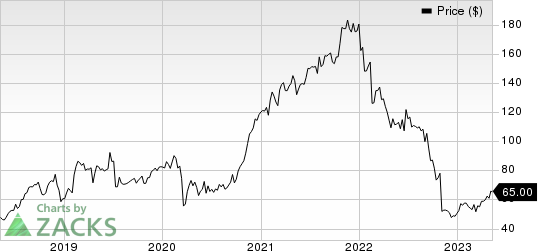

Omnicell, Inc. Price

Omnicell, Inc. price | Omnicell, Inc. Quote

Omnicell remains well-positioned to meet pharmacy and hospital needs, backed by recent acquisitions and expansion of its advanced services solutions. Strong revenue contributions from the recent acquisitions of FDS Amplicare, ReCept and MarkeTouch Media are major tailwinds. The company’s Central Pharmacy Dispensing Service continues to witness increasing demand from health systems, which buoys optimism. The company’s long-term sole source agreements with more than 50% of the top 300 U.S. health systems will allow it to help customers mitigate ongoing labor challenges.

In terms of its 2025 financial roadmap, Omnicell targets reaching 1.9 billion to 2 billion of revenues by 2025 at a 14% to 15% compounded total annual revenue growth rate from 2021 to 2025. Over the same period of time, it is also targeting an expansion of non-GAAP EBITDA margin from 21% in 2021 to 25% by 2025, representing margin expansion of approximately 400 basis points. The company is well-positioned to deliver on the 2025 total revenue growth targets, driven by factors like growing its tech services revenues, benefits from long-term sole source customer partnerships, multi-year co-development plans and increased average deal sizes.

On the flip side, revenues in the first quarter were down 8.8% year over year. The decline was mainly due to lower point-of-care revenues as a result of ongoing health systems and capital budget constraints. We note that the economic environment, including its effect on Omnicell health system customers, has caused many health systems to implement capital budget freezes and additional budget approval processes, resulting in elongated sales cycles. At the same time, ongoing health system labor constraints continue to increase, resulting in a higher-than-typical number of customers requesting to temporarily defer point-of-care implementations.

On a segmental basis, product revenues declined 17.8% year over year in the reported quarter. Meanwhile, rise in operating costs led to an operating loss in the quarter, placing significant pressure on the bottom line. The company has taken several measures to refine its cost structure, including a reduction in workforce and other expense containment efforts.

Over the past year, Omnicell’s shares have underperformed the industry it belongs to. The stock has declined 42.6% compared with the industry’s 33.3% plunge.

Key Picks

Some better-ranked stocks in the broader medical space are Edwards Lifesciences Corporation EW, Intuitive Surgical, Inc. ISRG and Johnson & Johnson JNJ.

Edwards Lifesciences, carrying a Zacks Rank #2 (Buy), reported first-quarter 2023 adjusted earnings per share (EPS) of 62 cents, beating the Zacks Consensus Estimate by 1.6%. Revenues of $1.46 billion outpaced the consensus mark by 4.7%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Edwards Lifesciences has a long-term estimated growth rate of 6.8%. EW’s earnings surpassed estimates in two of the trailing four quarters, missed the same in one and broke even in the other, the average being 1.2%.

Intuitive Surgical, having a Zacks Rank #2, reported first-quarter 2023 adjusted EPS of $1.23, which beat the Zacks Consensus Estimate by 3.4%. Revenues of $1.70 billion outpaced the consensus mark by 6.9%.

Intuitive Surgical has a long-term estimated growth rate of 13%. ISRG’s earnings surpassed estimates in two of the trailing four quarters and missed the same in the other two, the average being 1.9%.

Johnson & Johnson reported first-quarter 2023 adjusted earnings of $2.68 per share, beating the Zacks Consensus Estimate by 6.8%. Revenues of $24.75 billion surpassed the Zacks Consensus Estimate by 5%. It currently carries a Zacks Rank #2.

Johnson & Johnson has a long-term estimated growth rate of 5.5%. JNJ’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 3.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Johnson & Johnson (JNJ) : Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG) : Free Stock Analysis Report

Edwards Lifesciences Corporation (EW) : Free Stock Analysis Report

Omnicell, Inc. (OMCL) : Free Stock Analysis Report