Yahoo Finance

Yahoo Finance Providing Regulatory Clarity (Binance and Coinbase Edition)

Well I was going to write about last week’s market structure bill but then the SEC sued Binance and y i k e s. So let’s talk about Binance. And then the SEC sued Coinbase! Double y i k e s. So let’s talk about both of them.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

The SEC crusade

The narrative

The U.S. Securities and Exchange Commission (SEC) filed two major lawsuits and an application for a temporary restraining order over two days against Binance and Coinbase, respectively the world’s and the U.S.’s largest crypto exchanges. While the suits share commonalities, there are some pretty major differences as well.

Why it matters

These may well be the cases that define how cryptocurrencies are regulated in the U.S., at least until Congress passes some legislation (if that happens). We’ve seen the complaints; the question is how Coinbase and Binance will defend themselves.

Breaking it down

I’ve already written well over 2,000 words on the various lawsuits, so I’m not going to recap them here. Click the links to read my coverage of the Binance lawsuit and the Coinbase lawsuit.

I’m more interested in the responses from the companies right now. Both Binance and Coinbase have issued a number of statements and had their respective executives weigh in on both TV and Twitter about the allegations.

There are some clear differences so far: Coinbase CEO Brian Armstrong is making the TV and conference circuit, saying Coinbase does not plan to shut down its staking service (which is also facing heat from 10 state regulators) while Binance.US announced Wednesday it would halt trading on over 50 different token pairs, most of which were traded against the tether (USDT) stablecoin. Binance itself has said multiple times that customer funds have never been at risk, and that it disagrees with the SEC’s assessment.

One argument Coinbase has made since receiving its Wells Notice earlier this year is that the fact it’s gone public under the SEC’s auspices.

“The SEC reviewed our business and allowed us to become a public company in 2021,” Armstrong said in a tweet this week.

That’s a misleading claim, said Alexandra Damsker, a one-time SEC attorney who’s now an adviser to INX. A reviewer with the Division of Corporation Finance is not tasked with determining whether something is legal or illegal, she said, though they can alert the Division of Enforcement or another enforcement officer if they find something questionable.

“I can't tell them that what they're doing is illegal, because I don't know,” Damsker said. “And I can't tell them it's not because I don't know. And I can't warn them because I don't know and I can't put a comment on it because comments are public, and that would tell the industry or tell the marketplace that there might be something illegal and that's not something we can do, right? So what do I do? I continued the process.”

The Division of Corporation Finance would just continue its own review, which consists of looking for material misstatements or omissions and ensuring that the SEC’s rules are met, she said.

Armstrong also said Coinbase tried to “come in and register,” as SEC Chair Gary Gensler has often said, but “there is no path” to do so, a complaint echoed this week by Robinhood’s compliance chief Dan Gallagher in front of Congress (and it’s worth noting Robinhood received a subpoena tied to its crypto activities). Both Coinbase and Binance also reiterated their complaints about regulation by enforcement rather than guidance, though, arguably the SEC did provide some notice that it believed some (specific) cryptocurrencies are unregistered securities.

To some extent, this comes down to the fundamental question at the heart of this complaint: are cryptocurrencies – at least the ones listed in the Coinbase and Binance complaints – securities? The SEC obviously thinks the answer is yes, and so Coinbase’s efforts to get the agency to say something else may just well be moot.

Binance, for its part, is taking a similarly combative position, arguing in public statements that it had been cooperating with the SEC’s investigation and tried to work toward a “negotiated settlement.”

“While we take the SEC’s allegations seriously, they should not be the subject of an SEC enforcement action, let alone on an emergency basis. We intend to defend our platform vigorously,” Binance said. “Unfortunately, the SEC’s refusal to productively engage with us is just another example of the Commission’s misguided and conscious refusal to provide much-needed clarity and guidance to the digital asset industry.”

Of course, the Binance and Coinbase cases do share some major differences. While Coinbase is facing a largely vanilla case where the main allegation is “you listed securities and didn’t register as a broker, exchange or clearinghouse,” the Binance case includes a number of allegations that Binance and CEO Changpeng Zhao secretly had access to Binance.US’s customer funds and diverted these funds to Zhao’s own entities.

In various tweets, Binance.US has said that the SEC hadn’t previously expressed concern about customer funds and that its attorneys have already spoken with the agency about these issues.

Binance now has a June 12 deadline to respond to the SEC’s motion for a temporary restraining order, with a hearing scheduled for June 13. The company’s defense will (I’m guessing) illustrate some of its broader arguments against the SEC’s overarching complaint.

Stories you may have missed

Binance Lawsuit Could Be ‘Huge Mistake’ or Bring Needed Clarity to U.S. Crypto Industry: CoinDesk’s Helene Braun spoke to a number of crypto industry participants about the suit against Binance.

Binance Hands Rising Star Teng Key Role to Replace CEO Zhao at Largest Crypto Exchange: Shortly before the SEC filed its suit, Ian Allison reported that Binance’s Richard Teng is now well-positioned to become the head of Binance’s global empire should founder and current CEO Changpeng Zhao step down.

Cryptocurrencies Crash After the SEC Charges Binance With Sale of Unregistered Securities: This headline seems pretty self-explanatory.

Crypto Traders Suffer $320M Losses in Liquidations as SEC Lawsuit Against Binance Spurs Market Plunge: So does this one.

Coinbase Traders Withdraw $600M in a Day Amid SEC Lawsuits: And this one, really.

One-Two Punch Finally Registers SEC View on Binance, Coinbase, Rest of Crypto: “The mystery is over for how the U.S. Securities and Exchange Commission will come after the digital assets sector’s big platforms, though alleged skeletons in Binance’s closet drew more ire,” Jesse Hamilton writes.

This week

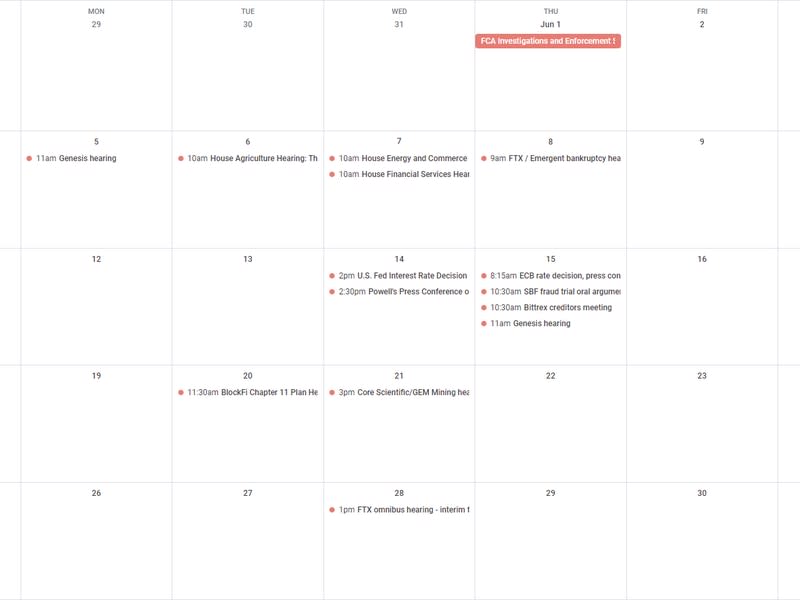

Monday

15:00 UTC (11:00 a.m. ET) There was a bankruptcy hearing for Genesis (a sister company to CoinDesk), in which a judge extended an ongoing mediation period between the company and its creditors.

Tuesday

14:00 UTC (10:00 a.m. ET) The House Agriculture Committee held a hearing on crypto legislation and regulation, featuring CFTC Chair Rostin Behnam, former CFTC Chair Chris Giancarlo, former Acting CFTC Chair Walt Lukken (who’s now CEO of the Futures Industry Association), former CFTC Commissioner Dan Berkovitz, former SEC Commissioner Dan Gallagher (who’s now chief legal compliance and corporate affairs officer at Robinhood) and former Magistrate Judge Paul Grewal (who’s now Coinbase’s chief legal officer).

Wednesday

14:00 UTC (10:00 a.m. ET) The House Energy and Commerce Committee’s subcommittee on innovation, data and commerce held a hearing on blockchains, featuring Southern Methodist University Law Professor Carla Reyes, Villanova University Professor Hasshi Sudler, Polygon Labs President Ryan Wyatt and Electronic Frontier Foundation Senior Fellow Ross Schulman.

14:00 UTC (10:00 a.m. ET) The House Financial Services Committee held a hearing on preserving the dollar’s role in the world.

Thursday

13:00 UTC (9:00 a.m. ET) Emergent Fidelity will have a bankruptcy hearing.

Elsewhere:

(The New York Times) Twitter’s advertising revenue continues to be down year over year, the Times reported, citing an internal presentation, and is “unlikely to improve anytime soon.”

(Rolling Stone) Rolling Stone’s Will Gottsegan (a former CoinDesker) profiled Binance CEO Changpeng Zhao, with the article publishing just days before the SEC lawsuit.

(The Atlantic) This is a long, in-depth and fascinating read about CNN chief Chris Licht. (Licht appears to have since been fired.)

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at nik@coindesk.com or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!