Yahoo Finance

Yahoo Finance Reasons to Retain Catalent (CTLT) Stock in Your Portfolio

Catalent, Inc. CTLT is well-poised for growth in the coming quarters, backed by its robust facility-expansion activities over the past few months. A robust third-quarter fiscal 2022 performance, along with a slew of strategic deals over the past few months, is expected to contribute further. Catalent’s operation in a competitive landscape and regulatory requirements pose threats.

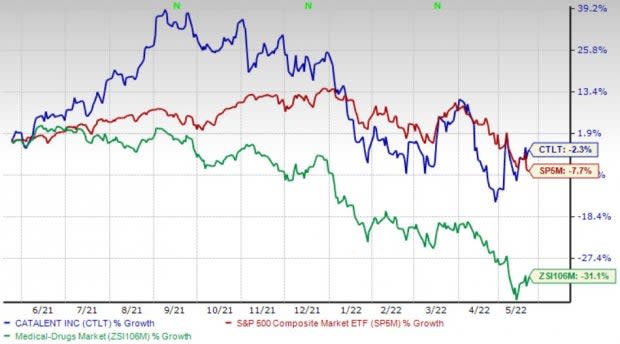

Over the past year, this Zacks Rank #3 (Hold) stock has lost 2.3% compared with a 31.1% fall of the industry and a 7.7% decline of the S&P 500.

The renowned global provider of advanced delivery technologies has a market capitalization of $17.96 billion. Catalent projects 17.3% growth for the next five years and expects to maintain its strong performance. It has delivered an earnings surprise of 9.2% for the past four quarters, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strong Q3 Results: Catalent’s solid third-quarter fiscal 2022 results, along with the year-over-year uptick in the top and bottom lines, buoy optimism. Continued strength in its Biologics arm in the quarter under review looks encouraging. Robust performances by the Clinical Supply Services, and the Softgel and Oral Technologies segments also raise optimism. A raised financial outlook for the year heightens our positivity regarding the stock.

Expansionary Activities: We are upbeat about Catalent’s robust expansionary activities like the opening of a slew of facilities over the past few months. This month, the company announced that it commenced a $175-million project to expand its flagship U.S. manufacturing facility for large-scale oral dose forms in Winchester, KY.

In April, Catalent announced that it completed a significant expansion of its nasal capabilities at its Morrisville, Research Triangle Park (RTP), NC-based facility to provide improved services for the development and manufacturing of unit and bi-dose nasal spray products.

Strategic Deals: We are optimistic about Catalent’s robust growth opportunities via its recent tie-ups and buyouts. The company, in March, announced its collaboration with TFF Pharmaceuticals, Inc. with respect to the latter’s patented Thin Film Freezing technology.

Catalent, in April, acquired Erytech Pharma’s commercial-scale cell therapy manufacturing facility in Princeton, NJ.

Downsides

Regulatory Requirements: The healthcare industry is highly regulated, wherein Catalent and its customers are subject to various local, state, federal, national and transnational laws and regulations, including the operating, quality, and security standards of the FDA and the DEA.

Any future change to such laws and regulations could affect the company. Failure by Catalent or its customers to comply with the requirements of these regulatory authorities could result in warning letters, among others.

Stiff Competition: Catalent operates in a highly competitive market, wherein it competes with multiple companies, including those offering advanced delivery technologies and outsourced dose form or biologics manufacturing. The company also competes in some cases with the internal operations of those pharmaceutical, biotechnology and consumer health customers that also have manufacturing capabilities and choose to source these services internally.

Estimate Trend

Catalent is witnessing a positive estimate revision trend for 2022. In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 1.1% north to $3.79.

The Zacks Consensus Estimate for the company’s fourth-quarter fiscal 2022 revenues is pegged at $1.33 billion, suggesting a 12.1% improvement from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Omnicell, Inc. OMCL, Patterson Companies, Inc. PDCO and AMN Healthcare Services, Inc. AMN.

Omnicell, flaunting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 16%. OMCL’s earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missed the same in the other, the average beat being 13.4%.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Omnicell has lost 18.5% compared with the industry’s 43.9% fall over the past year.

Patterson Companies has an estimated long-term growth rate of 9.9%. PDCO’s earnings surpassed estimates in three of the trailing four quarters and missed the same in the other, the average beat being 2.7%. It currently carries a Zacks Rank #2 (Buy).

Patterson Companies has lost 7.9% compared with the industry’s 6.9% fall over the past year.

AMN Healthcare has an estimated long-term growth rate of 1.1%. AMN’s earnings surpassed estimates in the trailing four quarters, the average beat being 15.6%. It currently sports a Zacks Rank #1.

AMN Healthcare has lost 1.8% compared with the industry’s 63% fall over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicell, Inc. (OMCL) : Free Stock Analysis Report

Patterson Companies, Inc. (PDCO) : Free Stock Analysis Report

AMN Healthcare Services Inc (AMN) : Free Stock Analysis Report

Catalent, Inc. (CTLT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research