Yahoo Finance

Yahoo Finance Scales Corporation Limited (NZSE:SCL): What’s In It For The Shareholders?

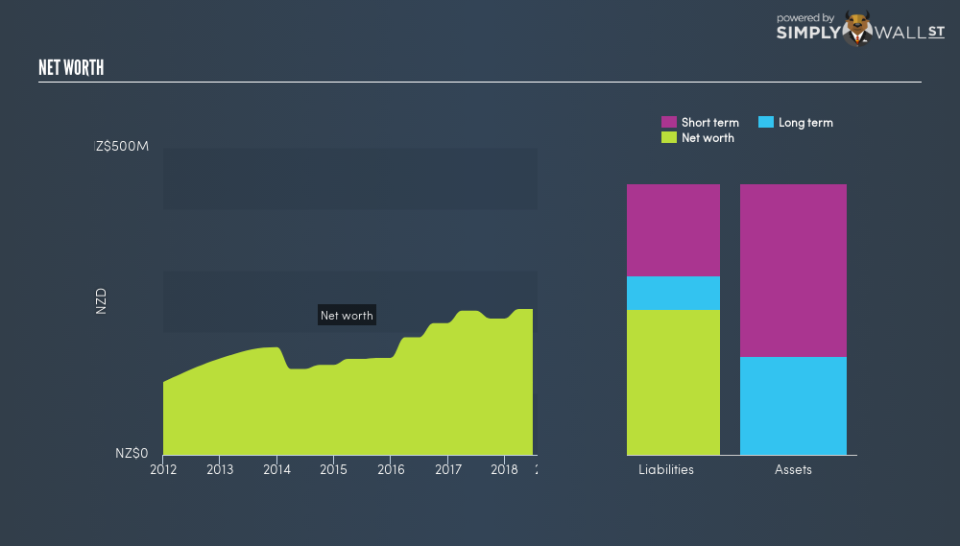

Two important questions to ask before you buy Scales Corporation Limited (NZSE:SCL) is, how it makes money and how it spends its cash. This difference directly flows down to how much the stock is worth. Operating in the packaged foods and meats industry, SCL is currently valued at NZ$682.9m. I’ve analysed below, the health and outlook of SCL’s cash flow, which will help you understand the stock from a cash standpoint. Cash is an important concept to grasp as an investor, as it directly impacts the value of your shares and the future growth potential of your portfolio.

Check out our latest analysis for Scales

Is Scales generating enough cash?

Free cash flow (FCF) is the amount of cash Scales has left after it pays off its expenses, including its net capital expenditures, which is what the company needs to spend each year to maintain or grow its business operations.

I will be analysing Scales’s FCF by looking at its FCF yield and its operating cash flow growth. The yield will tell us whether the stock is generating enough cash to compensate for the risk investors take on by holding a single stock, which I will compare to the market index. The growth will proxy for sustainability levels of this cash generation.

Free Cash Flow = Operating Cash Flows – Net Capital Expenditure

Free Cash Flow Yield = Free Cash Flow / Enterprise Value

where Enterprise Value = Market Capitalisation + Net Debt

After accounting for capital expenses required to run the business, Scales is not able to generate positive FCF, leading to a negative FCF yield – not very useful for interpretation!

Is Scales’s yield sustainable?

Does Scales’s future look brighter in terms of its ability to generate higher operating cash flows? This can be estimated by examining the trend of the company’s operating cash flow going forward. In the next few years, the company is expected to grow its cash from operations at a double-digit rate of 48.5%, ramping up from its current levels of NZ$34.3m to NZ$51.0m in two years’ time. Although this seems impressive, breaking down into year-on-year growth rates, SCL’s operating cash flow growth is expected to decline from a rate of 45.6% next year, to 2.0% in the following year. However the overall picture seems encouraging, should capital expenditure levels maintain at an appropriate level.

Next Steps:

Now you know to keep cash flows in mind, You should continue to research Scales to get a more holistic view of the company by looking at:

Valuation: What is SCL worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether SCL is currently mispriced by the market.

Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Scales’s board and the CEO’s back ground.

Other High-Performing Stocks: If you believe you should cushion your portfolio with something less risky, scroll through our free list of these great stocks here.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.