Yahoo Finance

Yahoo Finance Shareholders Would Not Be Objecting To Liquidity Services, Inc.'s (NASDAQ:LQDT) CEO Compensation And Here's Why

The performance at Liquidity Services, Inc. (NASDAQ:LQDT) has been quite strong recently and CEO Bill Angrick has played a role in it. Coming up to the next AGM on 23 February 2023, shareholders would be keeping this in mind. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. Here is our take on why we think CEO compensation is not extravagant.

Check out our latest analysis for Liquidity Services

Comparing Liquidity Services, Inc.'s CEO Compensation With The Industry

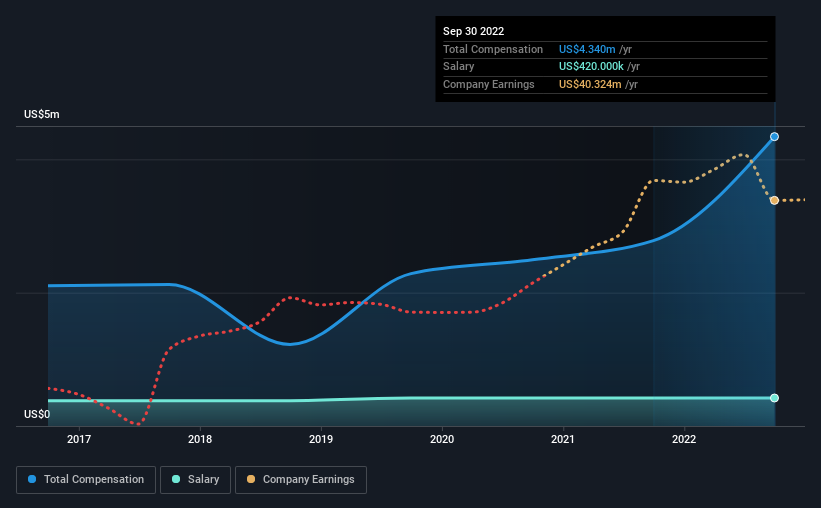

At the time of writing, our data shows that Liquidity Services, Inc. has a market capitalization of US$413m, and reported total annual CEO compensation of US$4.3m for the year to September 2022. We note that's an increase of 56% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$420k.

On examining similar-sized companies in the American Commercial Services industry with market capitalizations between US$200m and US$800m, we discovered that the median CEO total compensation of that group was US$4.9m. So it looks like Liquidity Services compensates Bill Angrick in line with the median for the industry. Furthermore, Bill Angrick directly owns US$92m worth of shares in the company, implying that they are deeply invested in the company's success.

Component | 2022 | 2021 | Proportion (2022) |

Salary | US$420k | US$420k | 10% |

Other | US$3.9m | US$2.4m | 90% |

Total Compensation | US$4.3m | US$2.8m | 100% |

Talking in terms of the industry, salary represented approximately 18% of total compensation out of all the companies we analyzed, while other remuneration made up 82% of the pie. It's interesting to note that Liquidity Services allocates a smaller portion of compensation to salary in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Liquidity Services, Inc.'s Growth

Liquidity Services, Inc.'s earnings per share (EPS) grew 91% per year over the last three years. Its revenue is up 6.4% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Liquidity Services, Inc. Been A Good Investment?

We think that the total shareholder return of 173%, over three years, would leave most Liquidity Services, Inc. shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We did our research and identified 3 warning signs (and 2 which are a bit concerning) in Liquidity Services we think you should know about.

Important note: Liquidity Services is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here