Yahoo Finance

Yahoo Finance Square (SQ) Q4 Earnings Beat, Robust Portfolio Key Catalyst

Square Inc. SQ delivered fourth-quarter 2017 adjusted earnings of 8 cents per share, which beat the Zacks Consensus Estimate by a penny. The figure jumped 60% on a year-over-year basis and also came ahead of the guided range of 5-6 cents per share.

Revenues of $616 million surpassed the consensus mark of $601 million and increased 36.3% year over year. Revenues also came well ahead of the guided range of $585-$95 million.

Adjusted revenues jumped 47% to $283 million. Management stated that retention rate across its entire-seller base remained positive, which reflected that existing sellers continue to benefit from the Square ecosystem.

Revenues from products launched since 2014 was 22% of total net revenues and 36% of adjusted revenues, up from 14% and 25%, respectively, in the year-ago quarter. These new products include Square Capital, Caviar, Invoices, Instant Deposit, and Build with Square APIs.

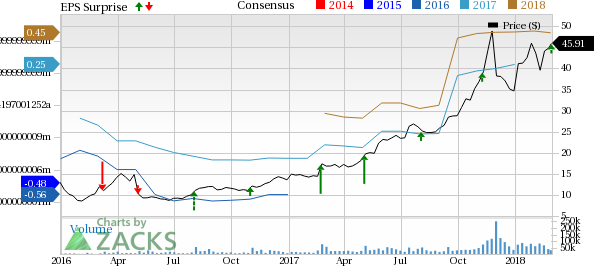

Square, Inc. Price, Consensus and EPS Surprise

Square, Inc. Price, Consensus and EPS Surprise | Square, Inc. Quote

Square’s focus on strengthening omni-channel commerce and expanding financial services offerings are driving top-line growth. Further, penetration into existing international markets of Australia, Japan, Canada and the U.K. is expected to be a key catalyst going forward.

GPV Details

Gross Payment Volume (“GPV”) increased 31% year over year to $17.9 billion, driven by growth in larger sellers.

Square defines larger sellers as those who make more than $125,000 of annualized GPV and midmarket sellers as those who make more than $500,000 of annualized revenues.

GPV from larger sellers contributed 47% to total GPV and was up 44% year over year.

Top-line Details

Transaction-based revenues of $524.6 million increased 30.3% year over year. The rise can be attributed to robust growth in Invoices, Virtual Terminal, and E-Commerce API payments. Transaction-based revenues as a percentage of GPV were 2.93%, down slightly from 2.94% in the year-ago quarter.

Subscription and services based revenues soared 96% from the year-ago quarter to $79.4 million. Rapid product innovation along with Square’s ability to cross-sell drove growth.

Instant Deposit, Caviar, and Square Capital contributed the majority of subscription and services-based revenues. Square Capital facilitated 47K business loans totaling $305 million, up 23% year over year.

Hardware revenues were $12 million, up 35.5% year over year, driven by an increase in sales of Square Stand along with strong demand for contactless and chip reader in Canada.

Pre-orders of Square Register were strong and shipping started late fourth quarter. This is expected to positively impact hardware revenues in the current quarter.

Operating Results

Adjusted EBITDA margin was 14.6%, down 100 basis points (bps) year over year, primarily due to higher investments.

Non-GAAP operating expenses as percentage of adjusted revenues declined 160 bps on a year-over-year basis to 70.8%.

Adjusted product development expenses remained flat year over year. General and administrative expenses and transaction, loan & advance losses as percentage of revenues declined 260 bps and 80 bps, respectively. These were partially offset by higher sales and marketing expenses, which increased 170 bps.

The year-over-year increase in sales and marketing expenses were primarily driven by an increase in Cash App peer-to- peer, paid marketing, and personnel costs.

Moreover, transaction losses as a percentage of GPV trended below Square’s 0.1% historical average, which reflects improvement from ongoing investments in risk management initiatives.

Transaction-based profit as a percentage of GPV was 1.07% better than 1.04% reported in the year-ago quarter.

GAAP operating loss was $13 million slightly narrower than an operating loss of almost $14 million reported in the year-ago quarter.

Balance Sheet

As of Dec 31, 2017, cash and cash equivalents balance was $1.1 billion compared with $658.4 million as of Sep 30, 2017. Long-term debt was $358.6 million, up $4.4 million sequentially.

Guidance

For first-quarter 2018, Square expects total revenues between $605 million and $620 million. The Zacks Consensus Estimate for revenues is currently pegged at $600.7 million.

Adjusted revenues are expected between $290 million and $295 million. The mid-point reflects year-over-year growth of 44%.

Adjusted EBITDA is expected in the range of $30-$33 million. The mid-point reflects year-over-year growth of 11%.

Adjusted earnings are expected in the range of 3-5 cents per share. The Zacks Consensus Estimate for earnings is currently pegged at 8 cents per share.

For 2018, Square expects total revenues between $2.82 billion and $2.88 billion. The Zacks Consensus Estimate for revenues currently stands at $2.84 billion.

Adjusted revenues are expected between $1.30 billion and $1.33 billion. The mid-point reflects year-over-year growth of 34%.

Adjusted EBITDA is anticipated in the range of $240-$250 million. The mid-point reflects year-over-year growth of 19%.

Adjusted earnings are projected in the range of 43-47 cents per share. The Zacks Consensus Estimate for earnings is currently pegged at 45 cents per share.

Zacks Rank and Stocks to Consider

Castlight carries a Zacks Rank #3 (Hold).

Paycom Software PAYC, Facebook FB and The Trade Desk TTD are some better-ranked stocks worth considering in the broader technology sector. While Paycom sports a Zacks Rank #1 (Strong Buy), both Facebook and The Trade Desk carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Long-term earnings growth rate for Paycom, Facebook and The Trade Desk are currently pegged at 25.75%, 26.51% and 25%, respectively.

Wall Street’s Next Amazon

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Facebook, Inc. (FB) : Free Stock Analysis Report

The Trade Desk Inc. (TTD) : Free Stock Analysis Report

Paycom Software, Inc. (PAYC) : Free Stock Analysis Report

Square, Inc. (SQ) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research