Yahoo Finance

Yahoo Finance Stable Fundamentals and U.S. Backing may Offset Micron's (NASDAQ:MU) Growth Revision

First appeared on Simply Wall St News

Summary:

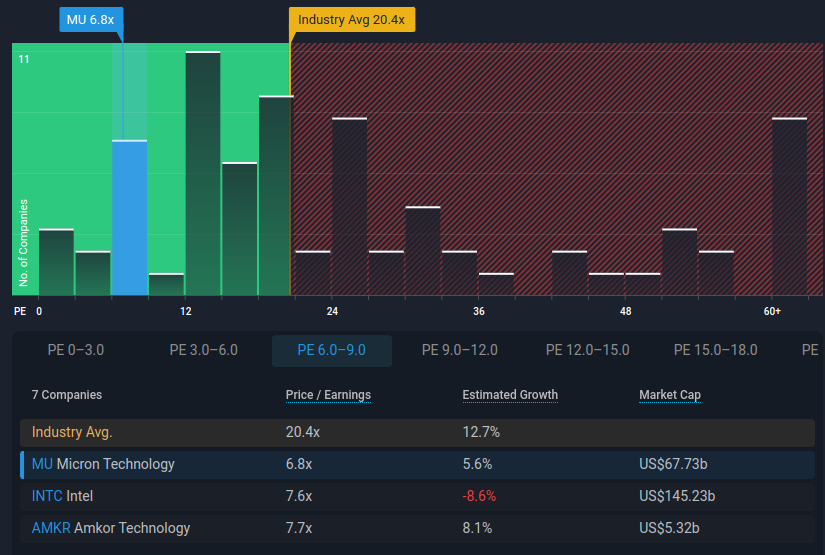

MU is trading at a low valuation of 6.8x PE relative to industry peers.

Despite the announced demand reduction, there are multiple fundamental factors that may play in favor of the company.

MU is pushing multiple capex growth projects, one of which is backed by the U.S. government.

Micron Technology, Inc. (NASDAQ:MU) has returned to the media spotlight after the recent outlook revisions. It seems analysts are keen to call a negative financial performance trend and imply that the stock could suffer. However, in order to have the full picture, we need to compare that to the fundamentals, possible offsetting factors and the current valuation of the company.

Looking at the relative value of price to earnings vs the overall industry, we see that the stock is trading at a lower valuation (P/E at 6.8) compared to peers (average P/E of 20.4), which may bolster contrarian arguments that the stock is cheap to begin with:

That is why we will take a deeper dive into the fundamentals of the stock, but investors can use the same approach when scanning other peers in the industry, such as:

Intel (NASDAQ:INTC)

NVIDIA (NASDAQ:NVDA)

AMD (NASDAQ:AMD)

Fundamental Analysis

When we analyze the fundamentals for Micron, we see a strong company with implied long-term growth, backed by government grants and capital investments. We will review some key fundamentals for the company:

Financial Health

Micron has been steadily building up a cash balance, which gives the company a safety position and is precisely what investors would like to see in the event of a demand decline. The company has a cash balance of $10.227b and total debt at $6.034b. Having more cash than debt decreases the risk in downturns. Additionally, the debt to market value of equity for Micron is about 9%, which is on the low-side for a company that is profitable and expected to take on growth CapEx projects.

Dividends and Growth

The company has a low 0.75% dividend yield, but there are reasons why that may be great for investors:

First, Micron is utilizing a mixed dividend and buyback approach to return capital to investors. In the last 12 months, the company has paid out $2.8b in buybacks and $506m in dividends. This makes the cash adjusted (for buybacks) payout ratio 68%. While the dividend appears small, it seems that most of the return for investors is provided via buybacks.

Second, this leaves some 30% of the cash retained in order to finance growth projects. The company is planning a $40 billion U.S. memory-chip manufacturing facility investment over the next decade. This is within the projected $150 billion of global planned CapEx investments for this timeframe. This facility will be considered a strategic investment and will be partly backed by the grants from the U.S. CHIPS and Science Act. It seems that Micron is expecting a decade long, investment driven growth journey - which is aligned with the U.S. interests to bring chip manufacturing back to the country.

Shareholders with a longer investment horizon may keep being bullish on the company despite short-term headwinds. Considering the growth projections, here is how analysts see the company performing in the next few years:

We can see that analysts have updated their forecasts on the 9th of August, and while they expect a decline in top and bottom line income for 2023, they are still bullish on the long-term product demand and expect to see growth back from 2024.

Micron's Future Outlook Revisions

On the 9th of August 2022, Micron issued a future outlook revision, citing a demand decline for DRAM and NAND for FQ4 2022 and FQ1 2023. Implying that they expect their memory chips to be less in-demand as people cycle away from buying PC components. For context, the industry saw a surge in the need for PC components during the pandemic as consumers were spending more of their time at home. Additionally, the tech boom drove demand for Bitcoin mining, from which semiconductor companies also benefited by selling processing units used in mining. Now, as the market normalizes, consumers are shifting their focus away from PC components and this is reflected in the reduction of demand. However, this decline seems to be temporary, as developing technologies still make these products attractive and cheaper parts open up lower-income demographics.

In the release, the company changed Q4 revenue guidance from the previous $7.2b +/- $400m, to about $6.8 or less.

They also indicated a meaningful reduction in planned CapEx for FY 2023, negative free cash flow in FQ1 2023, and sequential declines in margins. On the other hand, there is a possible risk reduction tailwind that may sustain the level of the stock price - Some analysts indicate that the FED will issue a September 0.75% rate hike and pause thereafter, upon which the market may react with higher valuations for equities across the board. This comes after the latest CPI results, which saw a decrease to CPI from 9.1% for June to 8.5% for July.

Conclusion

Overall, it seems that Micron will experience a temporary drop in fundamentals, but government backing, growth CapEx, long-term semiconductor demand, and a settling down of inflation may offset these negative factors, and investors that already view the company as undervalued may initiate contrarian strategies.

If these risks are making you reconsider your opinion on Micron Technology, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here