Yahoo Finance

Yahoo Finance Is Teck Resources Ltd. a Buy?

Mining companies rarely specialize in one commodity. That's mostly due to the nature of raw ores and mineral deposits, which often contain multiple resources. For instance, gold, silver, and lead are often mined from a single asset. Lithium production comes with a steady stream of potash. And so on. But only the largest companies can dip their hands into multiple cookie jars and own multiple production assets spanning unrelated mineral groupings.

The $11 billion mining stock Teck Resources (NYSE: TECK) is a great example. The Canadian miner is a major producer of steelmaking or metallurgical coal, zinc concentrate, and copper, in addition to being a small to moderate producer of gold, silver, lead, and molybdenum. It struggled during the commodity pricing slump that began in 2014, although things may be turning around.

Image source: Getty Images.

Management has cleaned up the balance sheet, operations are recovering with higher selling prices and lower costs, and it's about to add a sizable new revenue stream from production at a massive Canadian oil sands mining project with Suncor and Total SA.

Does the potential for near- and medium-term growth outweigh the long-term risks inherent to commodity-based industries?

By the numbers

The bull case is relatively simple to understand. Teck Resources has been cruising in 2017 thanks to incredible selling price increases in steelmaking coal compared to those realized in 2016. Production was essentially flat in the first nine months of this year compared to the year-ago period, but selling prices more than doubled.

That alone accounted for a roughly CA$2.5 billion increase in revenue between the periods. Throw in healthy increases in the selling prices of zinc and copper, and, well, there's not a whole lot for shareholders to complain about.

Metric | First Nine Months 2017 | First Nine Months 2016 | % Change |

|---|---|---|---|

Revenue | $8.84 billion | $5.74 billion | 54% |

Gross profit | $3.34 billion | $819 million | 308% |

EBITDA | $4.04 billion | $1.79 billion | 125% |

Cash flow from operations | $3.60 billion | $1.57 billion | 129% |

Debt | $6.12 billion | $8.70 billion | (30%) |

Dividends paid to date | $0.15 per share | $0.05 per share | 200% |

Data source: Teck Resources. Numbers reported in Canadian dollars.

The top and bottom lines are up. Debt balances are down. Operating cash flow and dividends paid have increased. Teck Resources is rolling -- and the best is yet to come for the diversified miner. Why?

The massive Fort Hills oil sands project is slated to come online before the end of 2017. It's expected to remain in service for at least 50 years and will reach production of 194,000 barrels per day within the first year of operations. The asset is 20% owned by the company, 51% owned by Suncor, and 29% owned by Total SA.

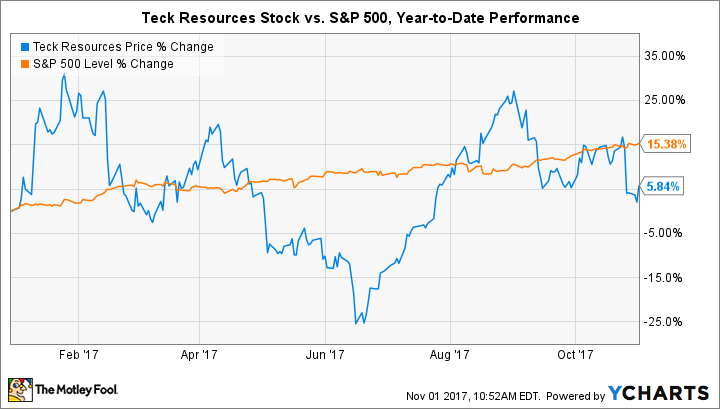

There is one problem, though: Wall Street can't seem to shake the connection between the phrases "oil sands" and "really expensive." Rather than serving as a near-term catalyst, the impending mine start-up seems to be weighing on Teck Resources stock, which is up just 5% in 2017.

The idea that oil sands products are expensive is a misconception. Er, kind of. Although oil sands projects are expensive upfront to build, they offer among the lowest production cost profiles in the industry once up and running. Since Fort Hills was 96% complete at the end of October, the most financially risky part of Teck Resources' commitment is essentially behind investors at this point. It's estimated to enable profitable production at $40 per barrel -- or lower -- crude oil prices.

Making matters more complicated, the stock sold off en masse after third-quarter 2017 earnings were released at the end of October. Despite the tremendous year-over-year operational improvement, investors didn't like the news that an inventory mix change will result in a one-time reduction of realized prices for steelmaking coal in the fourth quarter of this year. Yet, even with the short-term hiccup, selling prices will be close to double those from the year-ago period.

Is Teck Resources a buy?

Given Wall Street's inability to properly value the looming Fort Hills mine and the knee-jerk reaction to expected steelmaking coal prices for the final quarter of 2017, it's fairly easy to argue that Teck Resources stock is a buy at current levels. Even if coal and oil don't survive the 21st century as essential natural resources for modern society, they're far from being replaced anytime soon. That leaves plenty of growth potential for Canada's largest diversified miner in the near and medium term.

That said, it's important to remember that commodities markets can be volatile and accompanied by low margins for producers. Most mining stocks have failed to outpace the returns of the S&P 500 over even moderate time periods, instead of erupting for short bursts here and there, even when they're diversified into multiple resources. In other words, if you pull the trigger on Teck Resources at current levels, then know it may require more frequent re-evaluation than most other holdings.

More From The Motley Fool

6 Years Later, 6 Charts That Show How Far Apple, Inc. Has Come Since Steve Jobs' Passing

Why You're Smart to Buy Shopify Inc. (US) -- Despite Citron's Report

Maxx Chatsko has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.