Yahoo Finance

Yahoo Finance Total's Management Lays Out Why Its Stock Is a Buy

Despite the company's substantial operating improvements and improving income results over the past couple of years, shares of Total (NYSE: TOT) haven't exactly been a great performer. Total's stock is up 25% over the past five years, compared to a 64% gain for the S&P 500. Numbers like that don't incite much confidence for investors.

Listening in to the company's most recent conference call paints a very different picture, though. Here are some of the highlights from the company's meeting with investors that should give them reason to believe that the next half decade will be a substantial improvement over the last one.

Image source: Getty Images.

Is an oil supply crunch coming?

Oil production has been, and always will be, a constant struggle against the natural depletion of reservoirs and the natural decline of production that accompanies it. The only ways to combat it are to constantly invest in either improving reservoir recovery rates or to find new sources. As oil prices have declined, companies haven't had enough capital to deploy toward new sources. According to Total CEO Patrick Pouyanne, that underinvestment is going to catch up to the industry sooner rather than later:

It is a fact that we -- our industry, globally speaking -- did not invest much in the last three years, $400 billion instead of $750 billion previously. So this type of slowing investments will have an impact for years after the decisions. And so this is a fundamental surprise with support to the oil price. On the gas price, again the same story, a little more surprisingly, I think.

As much as U.S. shale production has changed the game, it still remains a modest part of global oil supplies. Those supplies will need to be replaced, but the backlog of projects under development looks quite small. This could be a boom for the industry in the coming years for companies that play their cards right.

Production profits come from more than just prices

I think it's fair to say that a majority of the published content on the oil and gas industry is about oil prices. Whether it's something OPEC did, some inventory-level data, or some geopolitical event that has traders spooked, there is always something driving oil prices at any given moment during the day.

Unfortunately, that ubiquity of content tends to heavily influence investment decisions by individuals. So with oil prices around $60 a barrel -- much better than a couple of years ago, but still way off $100 a barrel -- valuations in the oil and gas industry are quite modest today.

This kind of thinking overlooks an important point. Many companies have lowered their cost structure so that returns on $60 a barrel are much better today than a few years ago. This quote from CFO Patrick de la Chevardiere highlights this perfectly (text in bold my own for emphasis):

Our adjusted net income for 2017 was $10.6 billion, basically 28% higher than in 2016. The main driver was a 86% increase in upstream from a 23% increase in Brent.

This goes to show how the combined effects of higher prices and lower break-even costs have impacted the bottom line at Total and other oil producers. In fact, Total's free-cash-flow generation is now at the same levels it was before the oil crash despite the significantly lower oil prices today. Investors looking at this industry need to look beyond just oil prices, because $60 a barrel doesn't mean what it used to.

De-leveraged

Part of an investment thesis for integrated oil and gas companies like Total is their size and balance-sheet strength. It's a cyclical business, after all, and having the financial firepower to work through downturns in the industry can be incredibly valuable.

Of the integrated majors, Total's debt levels have tended to the high side of the industry, and its leverage was actually quite high when oil prices started to collapse. Thanks to finishing several major capital projects that increased production and decreased capital commitments, though, the company was actually able to reduce its debt loads. Here's de la Chevardiere explaining the progress the company has made and guidance for the upcoming years:

One of the most challenging aspect of the oil price collapse, for Total, was that we entered this period with gearing at 31%. One of the most significant achievement in term of financial, for me, over the past few years has been reducing the gearing. We ended 2017 with a 14% net debt-to-equity gearing. With [the Petrobras deal], which is complete today, it would have been 16%.

Starting 2018, we will change our gearing definition to be in line with what is used by our competitors, and we will use a debt-to-capital ratio. And using this debt-to-capital ratio, we reduce the gearing by two point[s]. This is not the objective, the objective being to be in line with what is used by our competitors. So the net debt-to-capital will be 12% by end of 2017.

This is a rather remarkable achievement for the company. A net debt-to-capital ratio of 12% would transform it from one of the most indebted integrated majors to the least. That should give the company plenty of firepower in the future to make deals, return capital to shareholders, or be ready for the next market swoon.

Growth in a low growth industry

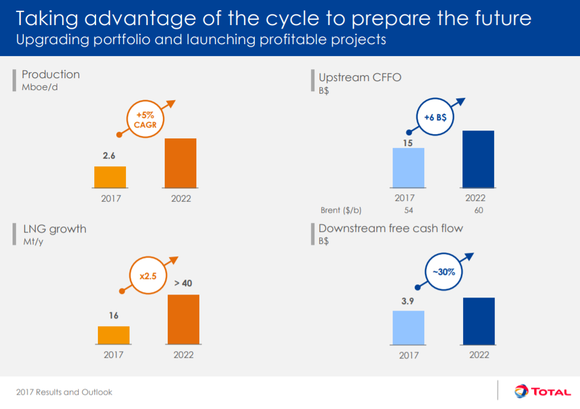

As part of the company's presentation, Pouyanne updated some of the company's objectives and how it intends to grow from its September presentation. The slide below is the one Pouyanne is referring to in this statement:

[W]e have there some few indicators which I think are summarizing the September presentation and the objective that we have and the assets that we have managed to put in our portfolio in order to achieve these objectives: a production growth with an average of 5% for the next five years; a double of or more than doubling [liquid natural gas] growth from 16 million tons management per year to more than 40 million tons, of course, thanks to the Engie deal. We have also, as I will say, an increase, and this is a target of $6 billion, of upstream cash flow from operations. And the downstream as well is targeting to increase its free cash flow by 50%. So this is, in figures, what we intend to do.

Image source: Total.

The most notable change in this slide from what we had seen before is the monumental change in liquid natural gas (LNG) growth. Total has said in previous statements that it wanted to focus on LNG, but it was working off a much smaller base than its peers. That changed recently with the acquisition of Engie's LNG assets, which are made up of an equity stake in the Cameron LNG export facility in Texas, several LNG tankers, sales and purchase agreements, and several regasification units.

The addition of these assets as well as some other investments has the potential to put Total on track to become the second largest LNG business among the integrated majors (Royal Dutch Shell is the largest). By 2020, Total estimates it will generate more than $3 billion in cash flow annually from LNG. Considering that analysts expect the global LNG market to grow at almost double the pace of oil, LNG represents one of the few outlets where oil and gas companies can grow significantly without the constant fear of oversupplying the market.

Creating additional shareholder value

Total has a problem it hasn't had in years: It has more cash than it knows what to do with. The company has already paid off a significant amount of its debt, and its capital spending plans are more or less set for the next few years. Without a plethora of options for acquisitions, the company has some extra cash on hand. According to Pouyanne, management intends to return that extra cash to shareholders:

[The] second proposal by the board has assigned to do is how do we share with our shareholders the benefit from oil price upside. We cannot, first, do it by increasing dividend, so let's introduce the share buyback and in order to share these oil price recovery. So it's, we said, up to $5 billion share buyback over 2018, 2020. It will come on the top of, obviously, of the scrip shares buyback. And of course, it's linked to the oil price recovery, because it's part of sharing the oil price upside.

It should be noted that management does intend to increase its dividend, but doesn't want to dedicate all that additional cash to dividend payments. After all, dividend payments were part of the reason that big oil companies looked a little questionable at the depths of the most recent crash.

Also, buying back stock looks pretty attractive right now because the company's stock is trading at modest valuations.

What a Fool believes

Total has been one of the best of the big-oil bunch over the past few years thanks to some of management's moves. The best of the bunch still wasn't exactly great, as the industry was reeling from low prices. However, as oil prices have started to turn and production costs have continued to decline, the company is generating impressive rates of earnings and cash flow that are giving management lots of options right now. With plans for robust LNG growth, a stock buyback program, and one of the highest rates of return in the business, Total looks very attractive today.

More From The Motley Fool

Tyler Crowe owns shares of Total. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.